By now you should understand Potomac is about managing risk focusing on the catastrophic risk of bear market declines.

However, I try to surround myself with different types of investors because it’s important to understand other opinions and experiences beside your own.

One group of investors I call the “Buy the Dip” crowd. They openly welcome market declines, not because they are permabears, but rather because, as they claim, it is a great opportunity to buy stocks at a discount.

There hasn’t been a nasty bear market for over a decade, so their sanguine disposition is understandable. These investors have zero fear when it comes to market declines and are unapologetically aggressive.

Since there hasn’t been a vicious bear market for years, their experience with declines is that they are short lived and recover quickly. In addition, during this period most risk management techniques have been punished.

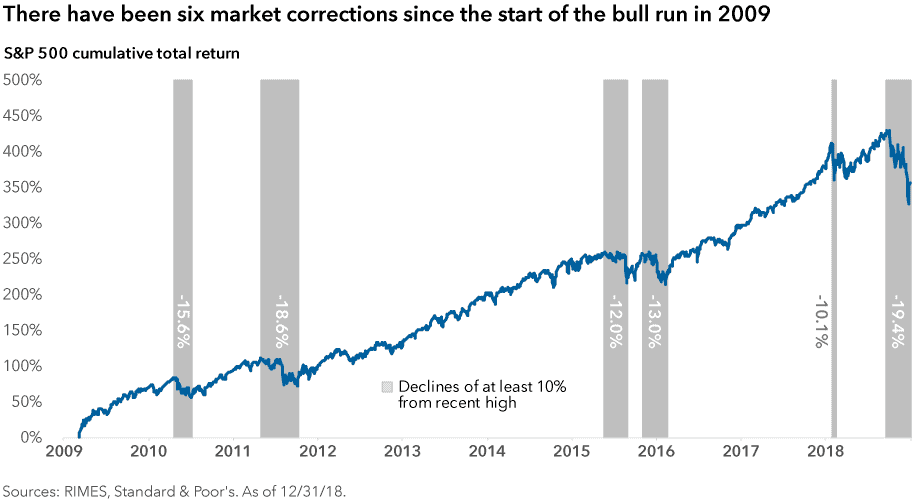

The bottom line is that the concept of buying the dip has worked extremely well in the last decade. Look at the corrections since the market bottom in 2009 and how quickly they recovered.

Our monthly market commentary updates has a statement on repeat when discussing our beliefs on money management; “it’s impossible to protect from every market correction but our job is to make sure the correction doesn’t turn into a catastrophic loss”.

There is a saying that bull markets take the escalator up while bear markets take the elevator down. If you zoom out many years this is true; however, while you are in the belly of the beast the experience feels vastly different.

Bear markets DO NOT go straight down and are littered with head fakes. In this type of environment buying the dip can be severely punished.

I admit the following examples are extreme bear markets when measured from peak to trough. However, the reason these are my examples is not the peak to trough loss but the violent rallies and declines that happened within the overall bear market.

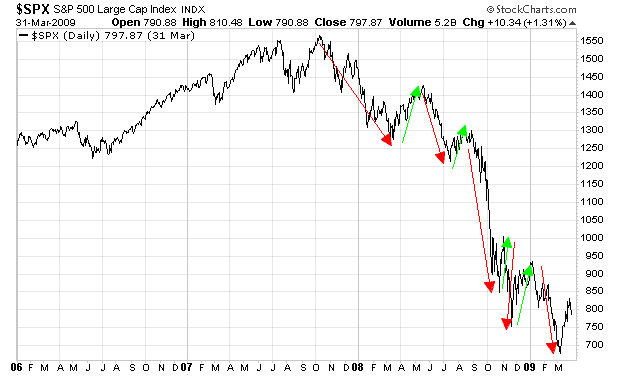

2007-2009 Bear Market (S&P 500)

- The market peaked in October of 2007 and proceed to decline approximately 18.5% through March of 2008.

- It then had a two month 12% rally through May of 2008.

- Which was then proceeded by a -15% decline that took us through the middle of summer.

- A quick 7% pop in three weeks preceded what was the nastiest part of the bear market; the 32% decline through the end of October.

- Just to mess with your head, the market then staged an impressive 10.5% rally in a week!

- But then it proceeded to drop another -16.7% until just before Thanksgiving.

- Next, the Christmas rally ensued sending the market soaring 15.8% through the week of 2009. Whew, we must be done with this by now!

- Sadly, we were not done as the market then barfed all over itself with another -27% decline through what was the ultimate bottom in the beginning of March 2009.

A picture is worth a thousand words…

You’re probably thinking “Well Manish, just shut up already about risk. The market rallied off the March 2009 lows and recovered all the losses in less than 5 years. Now we are amid the greatest bull market of all time. Go back in your hole…”

This is all true assuming you didn’t get wiped out from buying the dip. But what if it didn’t pan out this way OR you are on the doorstep of retirement. How long can you hang on waiting for a recovery?

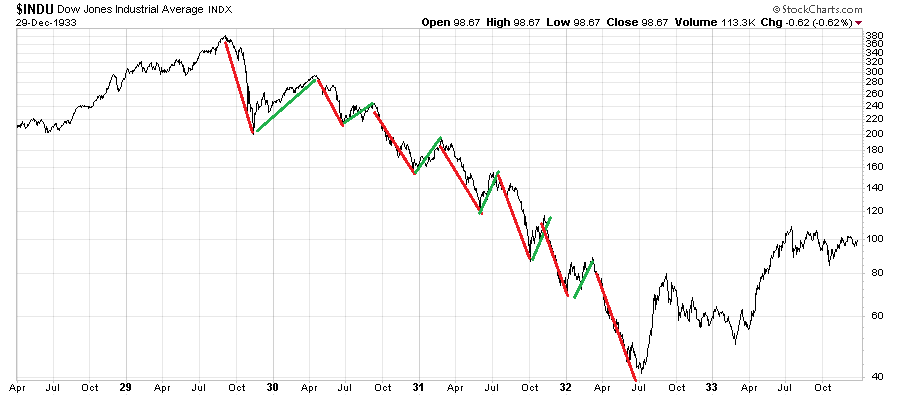

1929-1953 Bear Market (Dow Jones Industrial Average)

Buckle your seatbelt because this is gut wrenching and, without a doubt, can happen again.

- From the market top in September of 1929 the market fell -45% through the middle of November.

- It then staged an impressive rally of 40% through the spring of 1930 followed by a -25% decline through the beginning of the summer of 1930.

- The summertime saw a 11% rally only to be followed by another gut wrenching -36% decline to end the year.

- As Christmas of 1930 rolled around the market picked up steam and rallied 23% through the end of February 1931.

- This was followed by another gut wrenching -37% decline through the beginning of the summer of 1931.

- There was a monster one month rally of 23% to kick off the summer of 1931, only to be followed by another kick in the ass with a -43% decline through the fall.

- The fall of 1931 saw another monster one month rally of 35%.

- The “Christmas rally” failed to show up as the market then declined -38% through the start of 1932 which was then followed by a quick 24% rally through the beginning of spring.

- The final gut punch was from the spring of 1932 through Independence Day with a whopping -50% decline.

This total experience ended up being a greater than -85% peak to trough decline. This next fact every investor needs to make sure they understand (especially the young pups who have no fear):

The market DID NOT recover its losses until 1954 which was 25 years later!

Conclusion

An investment philosophy is born and cultivated based on the personal experiences of each investor. I don’t blame younger investors for being proponents of buy and hold because, in their experience, this mindset has been rewarded. In fact, I envy their youthful exuberance and irreverent approach to risk.

I was once a gun slinger, tech stock investor who was humbled by the tech burst 20 years ago. Investing through two soul crushing bear markets has a way of tempering greedy impulses.

You can’t just read about bear markets or point to fancy charts. The only way to truly figure out if you have what it takes is to manage other people’s money during a vicious bear market.

Will you stick to your beliefs with investors questioning your every move?

Will you follow your process and remain unemotional?

Will you trust your process, systems and indicators?

It’s a lot harder than it seems when there is no one that is holding your hand.

If drawdowns have you afraid to talk to your clients about risk we created a free white label resource to help, click to download after the break.

Disclosure: This information is prepared for general information only and should not be considered as individual investment advice nor as a solicitation to buy or offer to sell any securities. This material does not constitute any representation as to the suitability or appropriateness of any investment advisory program or security. Please visit our FULL DISCLOSURE page.