It’s quite common for investors to struggle understanding that investing is not a sprint but rather a marathon. When deciding on investments it’s important to understand the long-term risk to reward value add of the product, which can be further defined and evaluated by the strategies drawdown. However, there will always be a handful of investors who select an investment based on the long term but start to judge and evaluate it on the short term. Some of this misalignment can be attributed to misaligned expectations but it’s mostly the lack of understanding about timing and market cycles.

Anyone who understands sequence risk knows how critical timing is to overall investment success. For example, if an investor decides to retire just before or in the early stages of a bear market, they may see a big decline in the value of their accumulated wealth that could complicate their entire retirement plan.

On the other hand, an investor who retires at the start of a bull market would see the value of their portfolio appreciate and likely be able to enjoy a comfortable and secure retirement with less financial pressures to worry about.

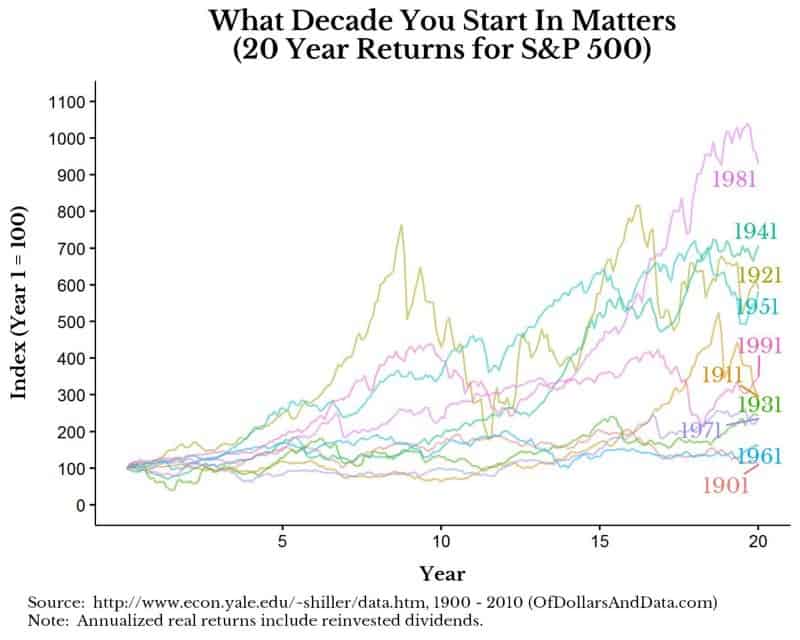

Different investors will have different experiences in the markets, depending on when they start investing. This idea was illustrated well in a recent article from “On Dollars and Data”, which examined total returns for stocks and a blended stock/bond portfolio over different 20- and 40-year periods. As one example, the chart below shows how 20-year returns for the S&P 500 diverged significantly over different decades, starting in 1901.

Born at The Right (or Wrong) Time?

An analysis like this gives the impression that successful investing is just a matter of luck or even birth year—just being born and starting to invest at the right time could make you twice as wealthy as someone else (or half as wealthy, if you were born at the wrong time.) But it’s not luck or birth year that leads to different experiences for different investors—it’s all about the timing of market cycles.

If markets went up all the time—in other words, if there was no cyclicality in the markets—then investors wouldn’t need the services of risk managers like Potomac. They could instead just put their savings in whatever investment offered the best returns until their money grew to meet their goals.

Of course, markets work nothing like this. Cyclicality comes with the territory. Bear markets always follow bull markets, and vice versa. We can’t predict when these different market cycles will appear or how long they will last, but we know one will always follow the other and we are ready to react accordingly. At Potomac, we manage the risks and seek the rewards that come over a full market cycle and therefore we are not a good fit for investors with a shorter time frame.

Why Full Market Cycles Matter

It’s common for investment managers to benchmark their performance over different time frames, from as short as one quarter or one year to up to 10 or 20 years. Whatever the chosen time frame, you can’t escape the fact that market performance over different periods is likely to be random. That’s because market cycles don’t start or end on quarters or calendar years. Nor do market cycles last for any specific length of time.

At Potomac, we prefer to measure the success of our strategies over the course of a full market cycle—from a market advance of 20% to a decline of 20%. Generally, this type of market performance won’t happen in a 3-5-year time frame. By nature, we are long-term investors, and clients who invest with us should also have a long-term time horizon as well.

The Value of Protection

As an unconstrained tactical investment manager, we position our strategies to offer investors some degree of protection from catastrophic investment losses. It’s like the way any type of property insurance works. Full Disclosure: Our strategies are NOT insurance and do not offer any sort of guarantee against losses.

For instance, as a homeowner, you buy insurance coverage for your property in the event of a devastating loss. In a place like the Florida coast, which is often threatened by hurricanes, it’s common to get hurricane coverage as part of a homeowner’s insurance policy.

Of course, hurricanes don’t follow any pattern—they appear randomly and follow unpredictable paths. Seven or eight years could go by without any sign of a single tropical storm. That could lead a homeowner to see no value in their hurricane insurance coverage.

But if a hurricane came in Year 9, you’d quickly appreciate the value of your hurricane policy. Without the protection offered by the insurance, you would have to pay for the loss of your home out of your own pocket. That’s generally not feasible for most people—unless you’re extremely wealthy, you probably couldn’t replace the value of your home from your savings alone. Instead, you would have to borrow from someplace else—your retirement savings, most likely—or just write-off the damage to your home as a total loss and move on.

Insurance works by protecting the value of your assets in the event of a devastating loss. Risk management works in a similar way, by acting like an insurance policy for your investment portfolio.

Risk management strategies generally don’t protect investors from all losses, but ideally, they will shield investors from most losses, specifically during catastrophic downturns. Without some degree of protection and the ability to react quickly to changing market conditions, the value of an investor’s assets would likely decline to a point where their financial future, their security and comfort, would be in jeopardy. To us, that’s a risk we believe investors should not have to take.

Disclosure: This information is prepared for general information only and should not be considered as individual investment advice nor as a solicitation to buy or offer to sell any securities. This material does not constitute any representation as to the suitability or appropriateness of any investment advisory program or security. Please visit our FULL DISCLOSURE page.