Investors are always seeking ways to make retirement planning and investing easier.

Due to that desire, product providers are always more than happy to create new products that will provide simple investment choices that are thought to be safer, or that have the capability to post better returns than the last set of products.

It’s not just mutual fund companies creating a fund based on the newest data-driven methodology. Financial services and financial technology companies are also always in the mix to convince investors that what they’re offering is truly special.

Remember the E-Trade baby? Though lighthearted and fanciful, the insinuation behind using a (talking) baby in their commercials is that E-Trade makes trading so simple, a child could succeed at using their software to build their investment portfolio.

More recently, Betterment’s new marketing campaign appeals to the idea that investors should always be working to, in their words, “outsmart average” and use new technology to put themselves at the forefront of investing strategies.

When it comes to corporate retirement plans, most participants will see Target Date Funds as the product referenced as making investing for retirement easier.

Target date funds now dominate most employer plans. In fact, the majority of those plans offer them as their default investment option and most employees don’t change from that pre-determined choice.

While target date funds may have a certain charm because of how easy to understand they appear to be on the surface, they aren’t the right fit for everyone’s retirement portfolio.

But before I explain why you might not want your entire retirement wrapped up in a target date fund, it’s important to take a step back and understand where they came from and where they’re going.

In this post we’ll cover the history of target date funds leading up to today, and why you should think twice about investing all your retirement savings in one.

Target Date Funds: Created for the DIY Investor

Way back in 1994, the first target date funds made their appearance.

Wells Fargo and Barclays Global Investors worked together to release the first funds of this kind in March of that year.

Originally, the reason behind the creation of target date funds made sense. Most plan participants struggled to select their own investments and build a balanced, risk-managed portfolio. Most investors still struggle with that task as much today as they did in 1994 too, so it’s not surprising.

And the truth is, target date funds do give investors a simpler choice over choosing a range of assets because you’re usually making one choice instead of many. But simple doesn’t always equal best, and I’ll explain more about why later.

At its most basic explanation, target date funds are a mutual fund that holds a mix of stocks and bonds. The assets held in the fund are professionally managed, and the fund’s asset allocation is adjusted to lower risk assets as they get closer to their target date—or at least that’s the idea, even though it doesn’t always happen.

As you might have guessed based on their name, the target date assigned to each fund plays an important role in the fund you might choose for yourself. It also plays a role in the “simplicity” of these funds.

Rather than choosing a balanced mix of equities and bonds on your own, you can instead choose a target date fund with a date near your own planned retirement year.

For example, if you were working in 1994 and wanted to retire in 2020, you would have chosen a target date fund close to that year. If you prefer your investments a little riskier, you might choose a fund with a date of 2025, or if you’re a little more conservative you might go the other way and choose a fund with a 2015 date.

Target date funds by their nature are designed to be long-term investments. You are typically choosing a fund that will carry you twenty to thirty years into the future.

Again, the idea is simple. It makes investing for retirement a “one and done” type of situation. But as we’ll see, that type of hands-off approach to your nest egg can lead to more problems than solutions.

First, though, let’s move up our history lesson to the present so you can see how the popularity of target date funds has affected how deeply involved clients get in their investment portfolios.

-07")

The Popularity of Target Date Funds in Retirement Plans Today

The simple value proposition of target date funds— choose your retirement year and then sit back and wait until that day comes — means that their popularity among investors has skyrocketed over the years.

In fact, target date funds have grown so popular that the majority of employer retirements plans now offer them as their default investment.

A Vanguard study about the current state of defined contribution plans, released in June 2018, estimates that 70% of its retirement plan participants will be invested in a single target date fund by 2022.

")

Source: Vanguard

Notes: Numbers for 2022 are Vanguard estimates.

In the same report, Vanguard also notes that at the end of 2017, 9 out of every 10 plan sponsors offered target date funds. Compared to a decade earlier, that represents a more than 50% increase in plan sponsors offering these types of funds.

In every which way you look at the numbers, the growth and popularity of Target Date Funds is astounding.

If we expand out our view to include 401k accounts, the expansion and demand is even higher, if you can believe it.

JPMorgan estimates that 88% of new retirement plan contributions are expected to flow into target date funds by 2019.

Take a second to review those numbers to get a good sense of how dominant these funds have become throughout the employer retirement plan market. There is not much more market saturation that these funds can see before becoming the only option for plan participants.

One of the reasons why target date funds dominate is because so many plans now choose them as their default investment option for employees.

If the promise of a target date fund was to simplify investing so an investor could not only skip the hassle of choosing their own investment mix, but also need only to choose a fund with a date in its name near their own retirement date, then it makes sense that most investors (who are not well-educated by employers about the markets and their investment options, to a great extent) would stick with the default options presented to them.

Of the 46% of plans that adopted automatic participant enrollment in 2017, almost 100% of employers also chose a target date fund as the default investment option for participants.

The ease of selecting a target date fund is the main draw that they have going for them. In my opinion, so many investors find target date funds attractive because they perceive them to be an investment they can choose once and then let go.

When most plan participants choose a fund with a target date close to their own hoped-for retirement date, they decide to let it sit without revisiting their plan.

They set up automatic deductions from their paychecks and consider their role in the investment and retirement planning process to be complete.

But wait. While the history and overwhelming success of target date funds make them sound simple, convenient, and a surefire way to create a winning retirement portfolio, that’s not necessarily true. The convenience and simplicity that create that “one and done” mentality for investors may be hurting many more than it’s helping.

In the next section, we’ll look at how that mentality contributes to the dangers of entrusting your retirement portfolio to a single fund—even one that’s managed for you.

Dangers of Target Date Funds for Retirement Plan Participants

There are three red flags I want to point out that illustrate why target date funds can be the wrong choice for many plan participants.

Target Date are One-Size Fits All

Investing solely in a target date fund, like most plan participants now do, means a loss of control.

The fund takes all the initiative out of the investor’s hands and creates a situation where they may be overexposed to an asset class that doesn’t truly fit their goals and what they want to do with their money, or the fund may not be as well-diversified as necessary to protect it against inevitable market downturns.

Furthermore, target date funds are not customized, and they can’t be tweaked to an individual’s life or changing situations. When you invest, you want to create a portfolio that works for you and is planned with your personal preferences and goals in mind.

You should be careful about entrusting your future, and the future of your family, to a product that doesn’t give thought to who you are as a person.

Target Date Funds are Not Risk-Managed.

Although they are marketed as such, I don’t see target date funds as qualifying for the label of a true “risk-managed” fund. Primarily, because the only way to truly manage risk is to use investments that have the ability to exit the market when risk levels are elevated.

For example, let’s look at investors who used Fidelity in their 403(b) plan and aimed to retire from any period between 2005 and 2015.

Assuming you only used one target date fund, (which the stats laid out above indicate is a safe assumption) you would have likely selected a Fidelity Freedom® fund with a target date closest to your expected retirement date.

During your retirement years, you are likely withdrawing money to meet expenses and you’re also not generating any income. The absolute last thing you need to start your retirement is a combination of large max. drawdowns and catastrophic losses.

If you’re not familiar with the idea of max drawdowns, it means how much money can you potentially lose, peak to trough, in a catastrophic market downturn. The chart below provides the max drawdown of the three possible funds in our scenario.

This isn’t the “conservative” way to start your retirement.

---09")

Source: Ycharts

Target Date Funds Rely Too Heavily on Bonds

Most, but not all, target date funds increase bond exposure as they get closer to the fund’s target date. While most investors assume that increasing bond exposure means more protection, that may not always be the case.

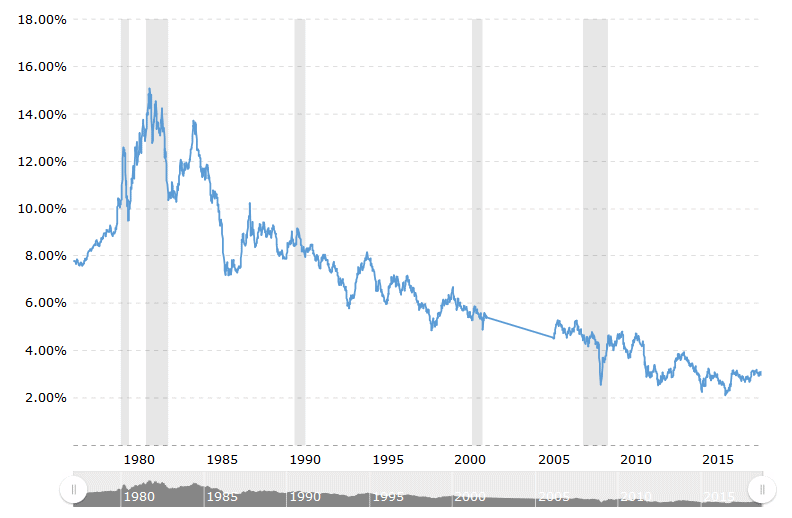

Bond prices decrease in a rising interest rate environment. If we look at the data, bond rates have dropped substantially since the early 1980s.

In July of 1984, the 30-year treasury yield was 13.5%, and in July 2018 that same rate was down to 3.1%.

Imagine a situation where you assumed increased bond exposure would protect you, but stocks and bonds decline in tandem prior to your retirement.

Like everything else in an investment portfolio, personalization is key. In addition to the risk of rising interest rates, too much investment in bonds too soon can spell problems for long-term cash flow in retirement if they don’t provide the income you need.

Unfortunately, because most investors treat the selection of a target-date fund as a one-time decision, many are likely unaware of how and when their allocation between equities and bonds is scheduled to change over the lifetime of their investment.

Conclusion

The allure of target date funds is easy to see. They offer the idea of a simple investment decision without the need for an individual to continually monitor that investment.

The truth, however, is that target date funds can take control out of an investor’s hands, and that lack of personalization and attention to detail can lead to serious consequences and an investment portfolio that doesn’t support what they want for their life and family.

If you’d like to have an experienced financial advisor, who will put your best interests first, take a look at your current retirement plan to see how well your current investments are supporting your goals for the future, click here.

We’ll review your portfolio and give you a Risk Score Analysis at no cost and no pressure to work with us.

Disclosure: This information is prepared for general information only and should not be considered as individual investment advice nor as a solicitation to buy or offer to sell any securities. This material does not constitute any representation as to the suitability or appropriateness of any investment advisory program or security. Please visit our FULL DISCLOSURE page.