Most Popular Types of Retirement Accounts Among Teachers

403(b) Accounts

A 403(b) is a retirement plan available to educational and health care institutions, in addition to certain non-profit organizations (police, firefighters, churches, etc.). This type of account is named after the section of the IRS code governing it and grows tax deferred until you begin to withdrawal from it at retirement.

Certain employees of tax-exempt organizations are eligible to participate. Participants include, but are not limited to, doctors, professors, nurses, teachers, ministers and administrators. Like a 401(k), employees must work through their employer to setup and participate in their plan. Although the options can vary, employees execute a salary reduction agreement to make pre-tax contributions.

These contributions are then sent to custodians chosen by the employer (such as Fidelity Investments). Contributions grow tax-deferred until the time of retirement, when withdrawals are taxed as ordinary income.

A 403(b) also offers favorable contribution limits to investors. In 2018, those limits were $18,500 per individual. Combined with a “catch up” limit of $6,000 for anyone over the age of fifty, you could contribute up to $24,500 of your own money to a 403(b) plan. In 2019, the contribution limit is rising by $500 up to $19,000. All of these limits do change from year to year and details can be found on the IRS website.

Plans that function similarly to a 403(b) but are named slightly different include: 401(a) and 457(b) plans.

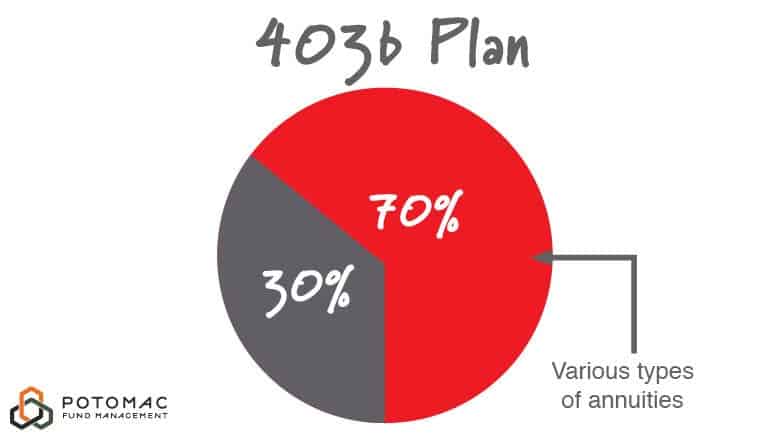

According to a study done by the Spectrum Group over 70% of the assets in 403(b) plans are comprised of various types of annuities.

Pensions

Social Security Benefits

Spending and Saving for Teachers:

How Your Profession Impacts Your Retirement Strategy

Budgeting and Saving

If you listen to the talking heads on cable business channels, you’re likely to believe that successful retirement is all about jumping in on the hot stocks, putting all your money into things called “options”, “calls” or “puts” but it’s unlikely that any of those strategies are going to lead to you feeling more confident in having the money to retire, and they’re all more liable to give you a bad night’s sleep instead.

It’s not as sexy as unearthing the next great tech company, but much of retirement success comes down to your behaviors and habits.

This focus on financial habits is especially important in a field where earning power is limited and pay raises are tightly controlled and often dependent on years in service and your education level.

Here are three quick behavior tips:

- Build positive money habits – When you do get a raise, chunk up any additional money you get into buckets. It’s okay to spend some of it, but you must remain disciplined. Put some toward debt, some toward savings, and another amount can be for spending.

- Understand your limits – No one knows you better than yourself. If your income isn’t likely to rise above a certain threshold, then figure out ways to maximize your saving opportunities now before you reach the point of no return.

- Plan with realistic goals – Some of the satisfaction with your retirement will come down to personal expectations. Maybe your retirement won’t see you taking a trip to Hawaii every year—so what is a plan that is both realistic and will still make you happy? Set your sights on what you can achieve, and you’ll feel more fulfilled.

If any of this seems daunting then you may want to consider hiring a financial coach who can offer guidance.

Take Advantage of Employer Benefits

Sometimes employers will offer to match contributions to your account if you’re invested in a defined-contribution plan. And sometimes, those matching contributions are tied to how much you contribute yourself.

Let’s not beat around the bush—these types of employer benefits are huge for long-term success. Do whatever you can do to ensure that you are taking full advantage of benefits like this and getting all the benefits your employer owes you.

If you contribute 7% to your retirement account and your employer offers a 3% match, then you’re up to 10% of your income and over time that additional percentage will make a huge difference in your retirement portfolio.

The 403b for Teachers

Earlier in this write up we took a brief look at 403b accounts.

If you skipped that section, here’s a quick rundown:

What is it?

A retirement plan available to educational and health care institutions, in addition to certain non-profit organizations (police, firefighters, churches, etc.).

Who can use it?

Certain employees of tax-exempt organizations are eligible to participate. Participants include, but are not limited to, doctors, professors, nurses, teachers, ministers and administrators.

Why is it a good option?

Contribution limits are favorable. Earnings are tax-deferred.

With that out of the way, let’s look more in-depth at why this type of account can be a good option for you.

How Can a 403b Benefit Teachers

If your employer offers a 403b, you should absolutely take advantage of it.

Investing offers you a tremendous opportunity to put money you save to work for your future retirement needs. Think of it like getting a little extra money in your paycheck without having to work additional hours.

Instead, your money works for you behind the scenes while you continue to work, allowing you to reap the rewards later.

The money you earn today is worth more in the present than in the future because of inflation. This is a concept called the time value of money.

You can see a real-life example of this idea in the prices of many basic goods you purchase—for instance, a gallon of milk costs more today than it did 30 or 40 years ago and will likely cost more 30 or 40 years from now.

Inflation, as it is known, erodes the purchasing power of the money you save today so it won’t buy as much in the future. But you can counter the effects of inflation by seeking to grow your savings over time by investing it.

At the very least, you need to earn a return on your savings each year to match the annual inflation rate. That helps you break even by maintaining your money’s purchasing power.

Now, making your money work for you is something that can apply to any investment account, but 403b accounts offer a few major benefits over other types of investment accounts:

- Contribution limits are very favorable for you, they come from your pre-tax earnings up to the annual limit and are automatically deducted from your paycheck.

- Tax-deferred growth helps you keep and reinvest more of the money you earn on your investments, because any gains or earnings you realize on your investments won’t be taxed until you withdraw them. When tax-deferred growth and earnings stay in your 403b account, they can compound over time to help you accumulate greater wealth.

- You can gain access to several investment options from professional investment managers using pooled investment vehicles such as mutual funds.

All these benefits won’t be worth much to you, however, if you don’t personalize your investment approach in such a way that the risk you take correlates to the goals you want to achieve.

Understanding the Role of Risk for Your Retirement

People who work in finance have many ways to talk about risk and many of their terms don’t make much sense to the average investor—alpha, beta, Sharpe ratio and so on. At the end of the day, how much do you, or frankly most financial professionals, really understand about these terms?

The answer is: not much.

No one really understands risk, so investors don’t talk about it and the consequences are significant. Only one in four clients say their financial advisor has talked about how much their investments may decline if the market crashes.

And what if you don’t have a financial advisor at all?

It’s a good bet that most people aren’t even thinking about risk at all—taking that number down to zero out of four clients discussing risk.

People think about risk and reward trade-offs nearly every day, most often outside of the context of the investment markets.

Consider these choices:

- “Should I buy life insurance?” You weigh the risk of paying too much premium for a life policy, versus the reward of knowing your beneficiaries get some degree of financial protection.

- “What should my car insurance deductible be?” You may reward yourself with lower premiums by choosing a higher deductible, but you risk paying more out of pocket if you have an accident.

- “Should I go to the gym or stay on my couch?” You risk the poor health consequences of a sedentary lifestyle for the reward of easy entertainment.

Measuring and discussing investment risk needs to be kept simple. The one risk measurement you should care about the most (whether you realize it or not) is maximum drawdown risk—how much can you potentially lose in a catastrophic market downturn?

Click on the video below to see the benefits of tactical money management:

Remember, investing is a marathon, not a sprint.

It’s easy to get caught up in the latest hot stock, but the investors who survive and prosper are those who can manage their investment risk.

When It’s Time to Talk to a Professional

With all that being said, it’s not easy to plan for your retirement on your own.

Sure, there are many people who love the DIY aspect of investing. But between lesson plans, office hours, and that summer vacation (that, let’s be honest, isn’t much of a vacation at all)how much time do you have to put toward making sure your finances are matching up to give you the kind of retirement you want to have?

If you find yourself identifying with any of these four scenarios, then it’s time to talk to a professional:

- You aren’t comfortable with choosing your own funds – Did you open a 403b and just checked off a few boxes without understanding how those choices fit together for a cohesive plan? Maybe you are invested in a single target-date fund that matches up with your expected retirement date.

- A market downturn makes you scared/uncomfortable – Remember max drawdown in our risk section earlier? If you don’t know how much you can lose in your account and still feel comfortable with your finances, then you probably don’t have a solid plan in place for retirement at all.

- You often worry about your investments – You shouldn’t stay up at night worrying about how much you’ll have saved for retirement. You shouldn’t have your mind drifting off during class if you noticed during lunch that the markets are taking a sudden dip. If you worry a lot, it’s a sure sign that it’s time for a professional to step in to offer you guidance.

- You have complex questions that need answers – Complexity can be different for everyone. If you live in a state where you will receive Social Security benefits, and you have a Pension, it could be that you have questions about how both of those benefits will work together to provide you with a retirement that aligns with your goals in life.

See yourself in one of these four situations? We’re here to help.

A Little About Potomac Fund Management

Potomac Fund Management is an SEC registered fee-only investment advisor. Our team of professionals shares three core beliefs:

- Small businesses form the strength of the economy.

- Technology, when used correctly, should enhance our lives—not take it over.

- Relationships and customer service still matter, and not everything has to be delivered with a ticket number.

As a fiduciary and fee-only advisor, we sit on your side of the table to educate and deliver risk-managed investment strategies specific to your situation. We don’t believe in or sell complicated commission-laden investment products.

We put our money where our mouth is and invest our own personal assets in the same strategies, we recommend to you.