Despite seven up weeks in a row for the S&P 500, there is an internal Clash (get it) in the market. In the spring, breadth was strong but the indices were weak because the top‑weighted stocks were lagging. Now, breadth is deteriorating, but it does not seem to matter. The indices are being held up now that the monsters have rebounded.

Such is the nature of capitalization‑weighted indices in a world dominated by passive flows.

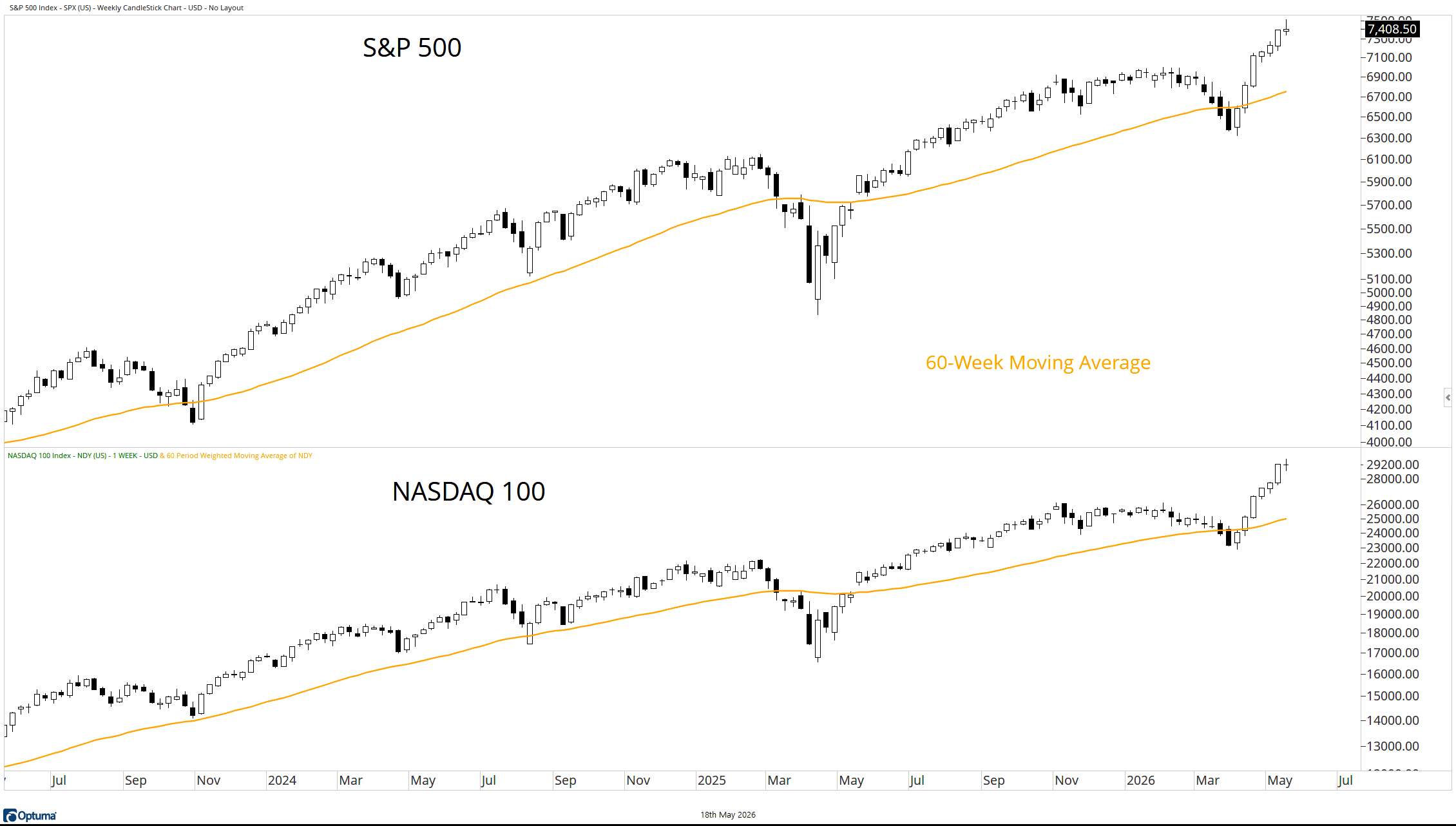

S&P 500 and NASDAQ 100

While the S&P 500 logged lucky number seven, the NASDAQ 100 did not. Both remain above rising 60‑week moving averages, but both showed a change in character last week. For the first time since the end of March, neither index closed the week near the top of its range.

Maybe it’s nothing. Or maybe we will look back and realize that last week mattered. Only time will tell, as I still do not possess that mythical crystal ball that others claim to have.

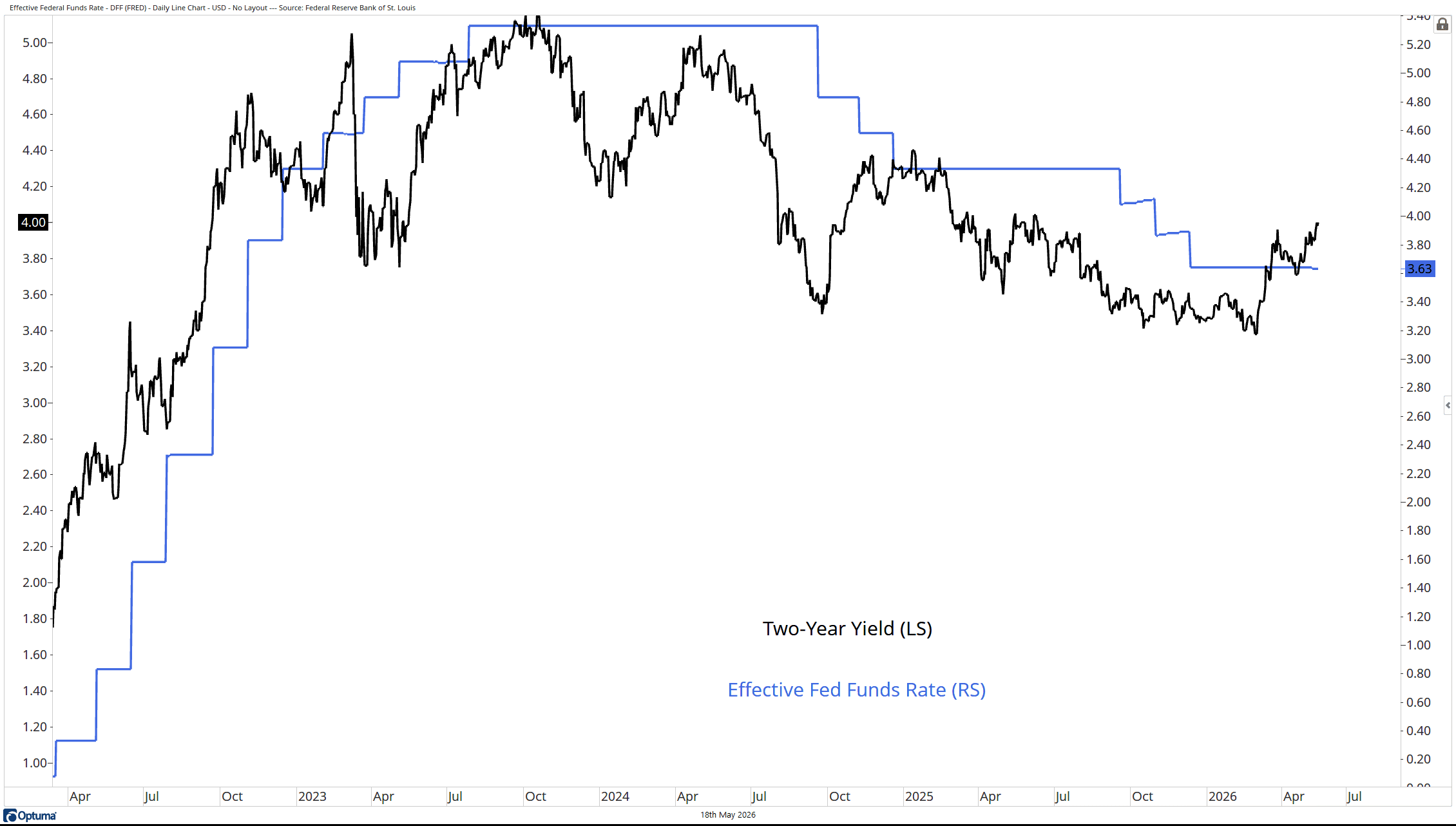

Source: Optuma

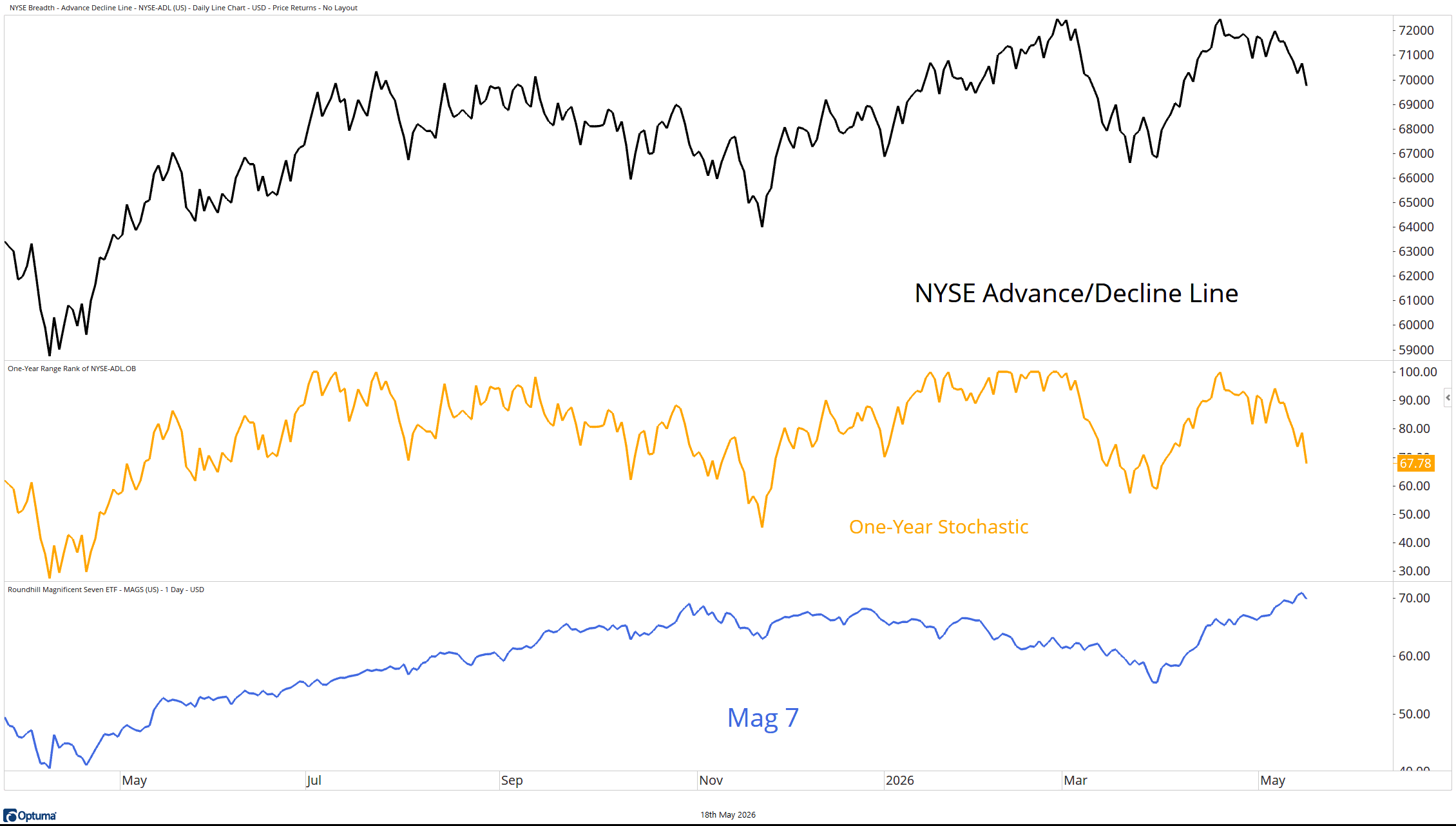

Breadth One

The NYSE Advance/Decline Line has failed to confirm the new high in the S&P 500, at least for now. This is what we call a negative divergence. Divergences can be large or small, but generally speaking, we do not want to see the one‑year stochastic near 60 while the S&P 500 is pressing all‑time highs.

The S&P 500 can continue to work if the Mag 7 stays near record levels. Remember how the flows work. The S&P 500 is capitalization‑weighted and dominated by passive flows. As long as people are employed and contributing to retirement accounts every paycheck, the largest stocks attract the most capital.

Source: Optuma

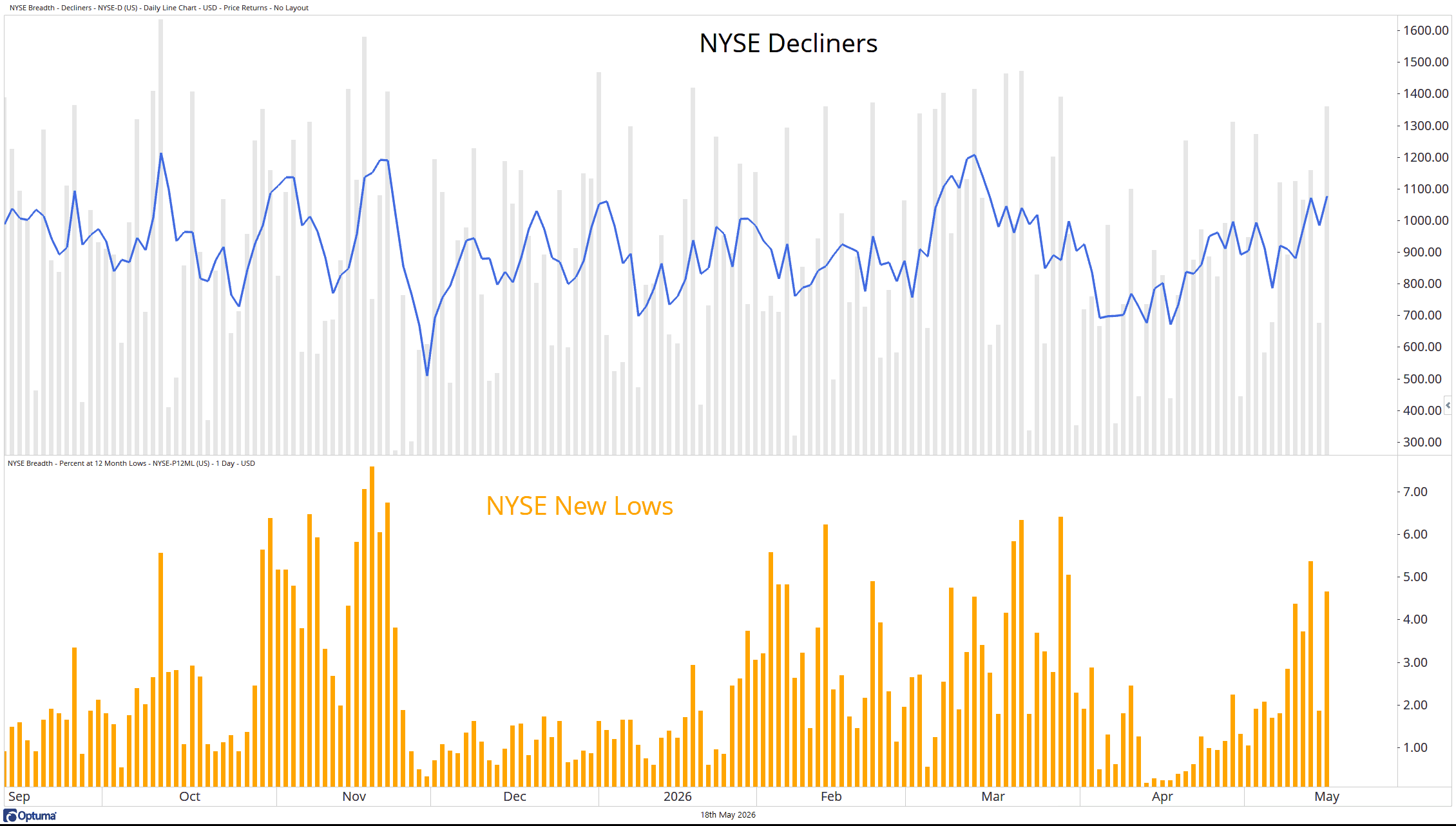

Breadth Two

With the Advance/Decline Line rolling over, we know the number of decliners is rising. This does not appear to be the result of one or two bad days. The five‑day moving average of decliners has been trending higher since early April.

At the same time, NYSE new lows have also been increasing.

Source: Optuma

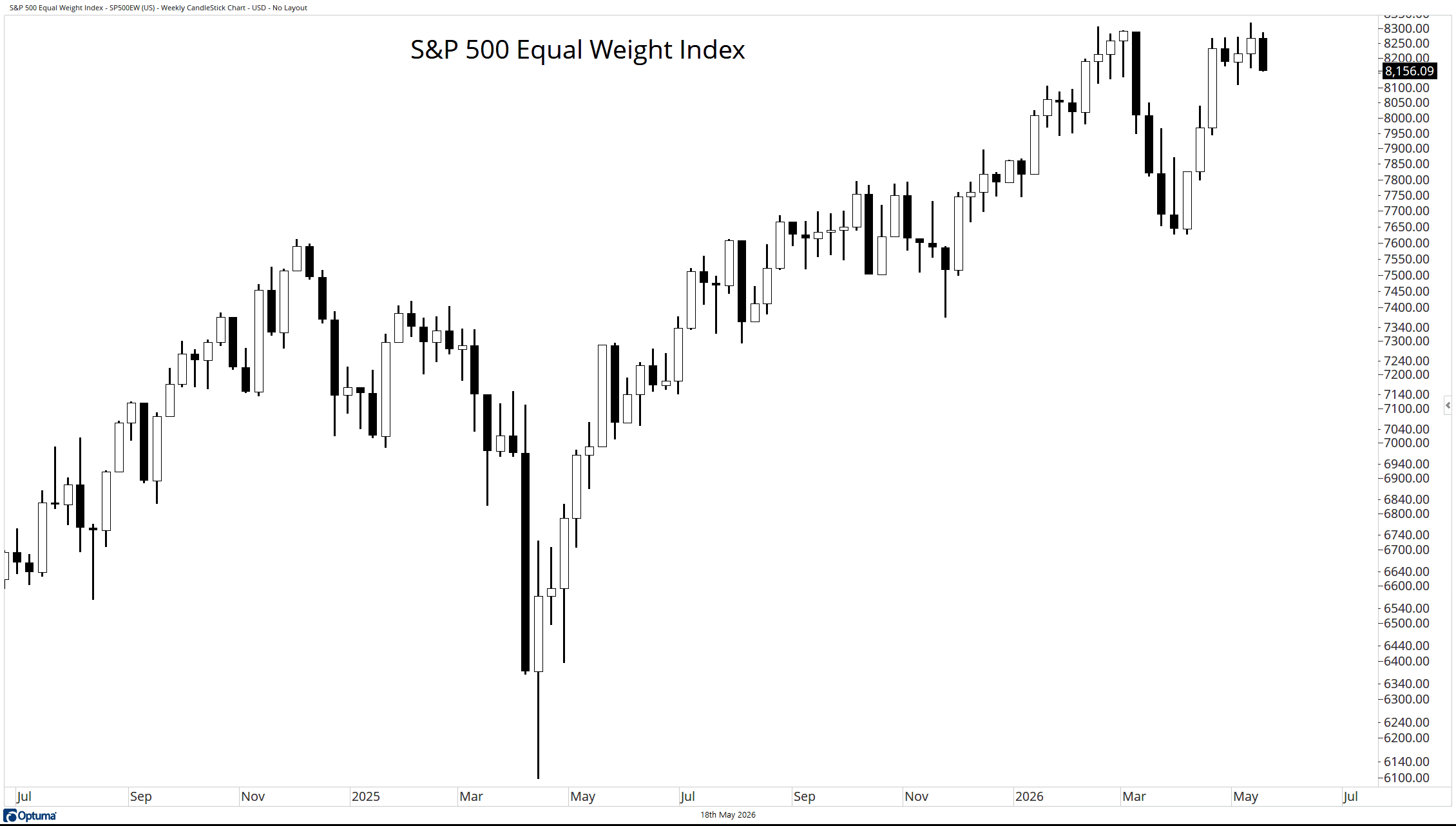

S&P 500 Equal Weight Index

When we strip out the capitalization weighting, the “broad market” is struggling. The Equal Weight S&P 500 failed to make a new high and closed last week at the low of the range.

It is also trading below where it was in early February.

That tells a very different story than the headline index.

Source: Optuma

Where is the Market on Rate Cuts?

Looking at the spread between the two‑year yield and the Effective Fed Funds Rate, it is fair to say the market may be shifting toward hikes rather than cuts.

If rate cuts were part of the bullish thesis, they should not be anymore.

Source: Optuma

Final Thoughts

The market cannot seem to make up its mind. It is in a Clash (get it again) with the Mag Seven. When the biggest stocks are working, weak breadth does not seem to matter. But when they weaken, strong breadth gets overwhelmed.