Worse, Not Better

Dan Russo, CMT

March 16, 2026

It’s getting worse, not better. The trends we’ve been highlighting over the past few weeks have continued to break down. We all know why, but as I like to say, the “why” doesn’t matter. The “why” is not what pays you.

Is this the start of a deeper decline, or simply another “buy the dip” opportunity? No one knows for sure.

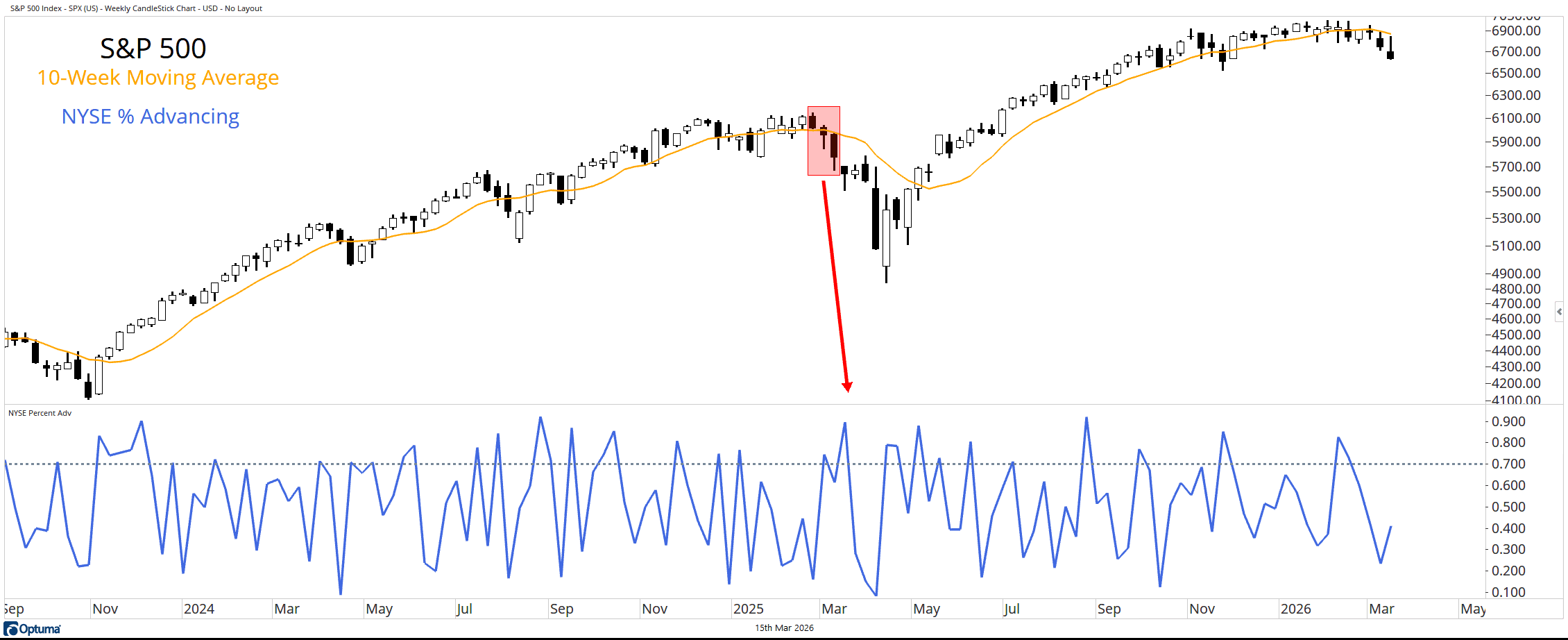

S&P 500

The S&P 500 closed below its now declining 10-week moving average for a third consecutive week. More telling, the index rallied back to that average and failed.

There was a modest uptick in the percentage of NYSE issues advancing, but it simply wasn’t enough. The price setup here looks similar to what we saw last February/March.

Source: Optuma

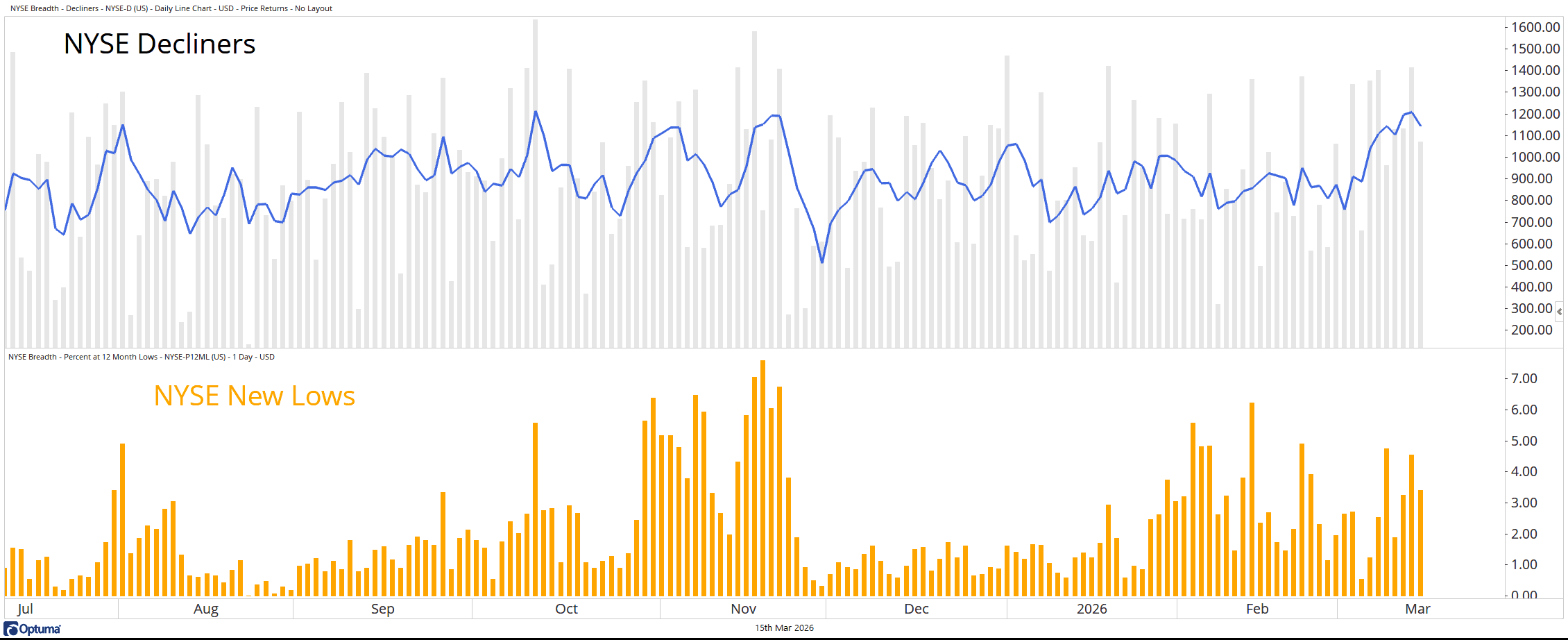

NYSE Decliners and New Lows

The five-day moving average of declining stocks on the NYSE has continued to trend higher throughout March. At the same time, the percentage of stocks making new lows has been creeping higher all year.

That combination is not supportive.

Source: Optuma

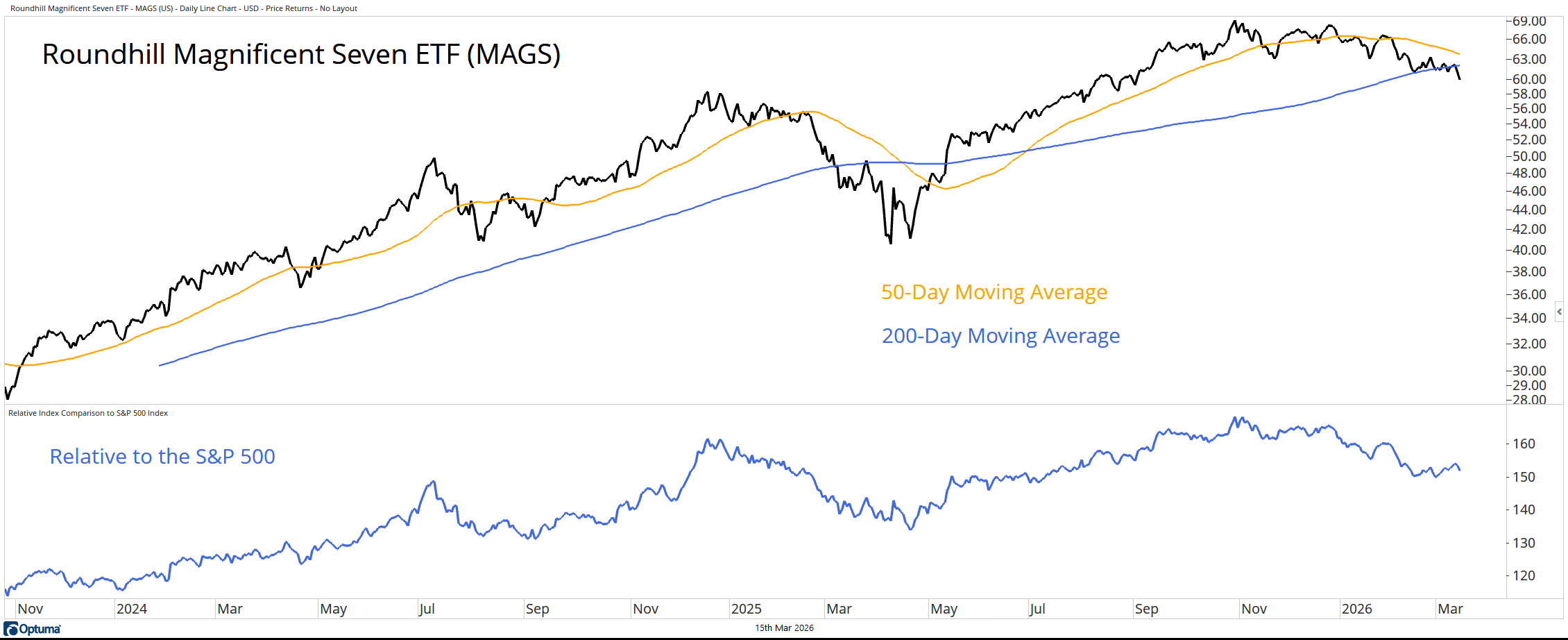

The Mag Seven

The Roundhill Magnificent Seven ETF (MAGS) made a new low for 2026 and remains below both its 50 and 200-day moving averages. The group continues to underperform the S&P 500.

The weight is getting to be too much.

Source: Optuma

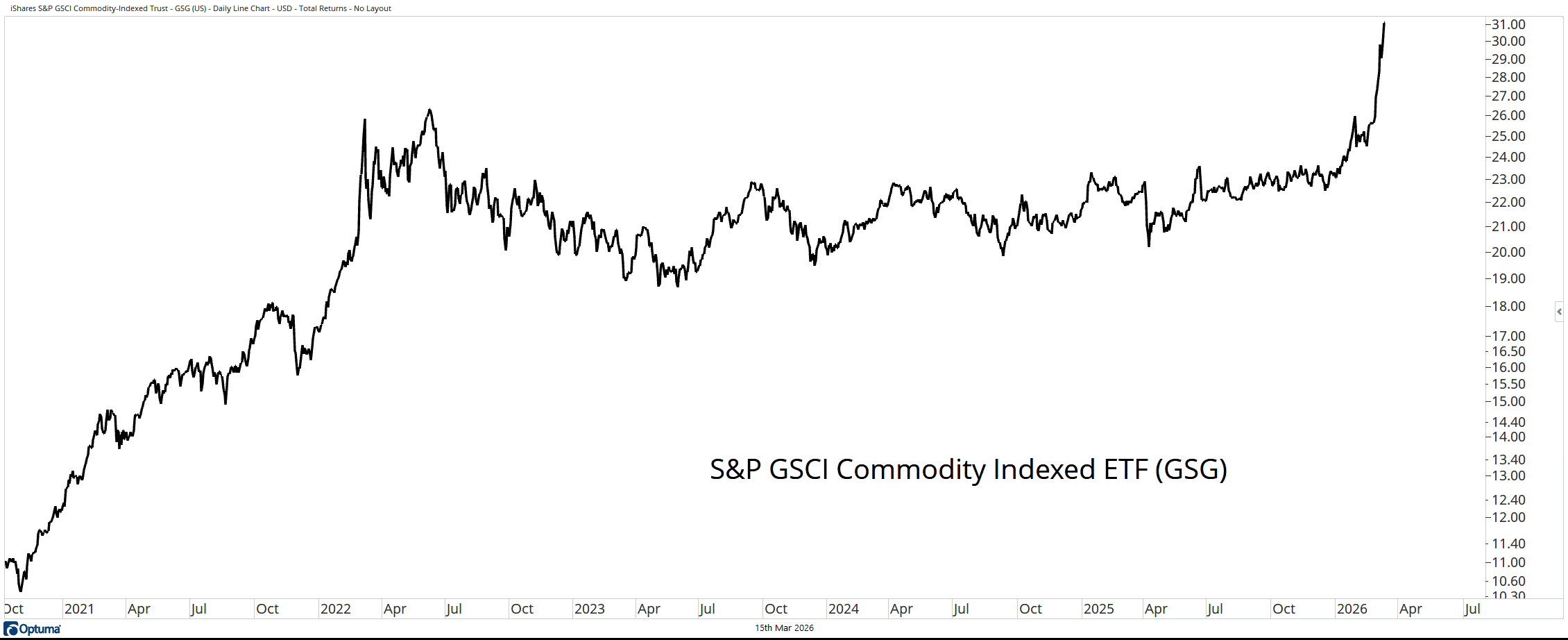

Commodities

We also need to address the move in the S&P GSCI Commodity Indexed ETF (GSG), which is breaking higher out of a nearly four-year base. Unless there’s a meaningful near-term reversal in oil, this trend can persist.

Source: Optuma

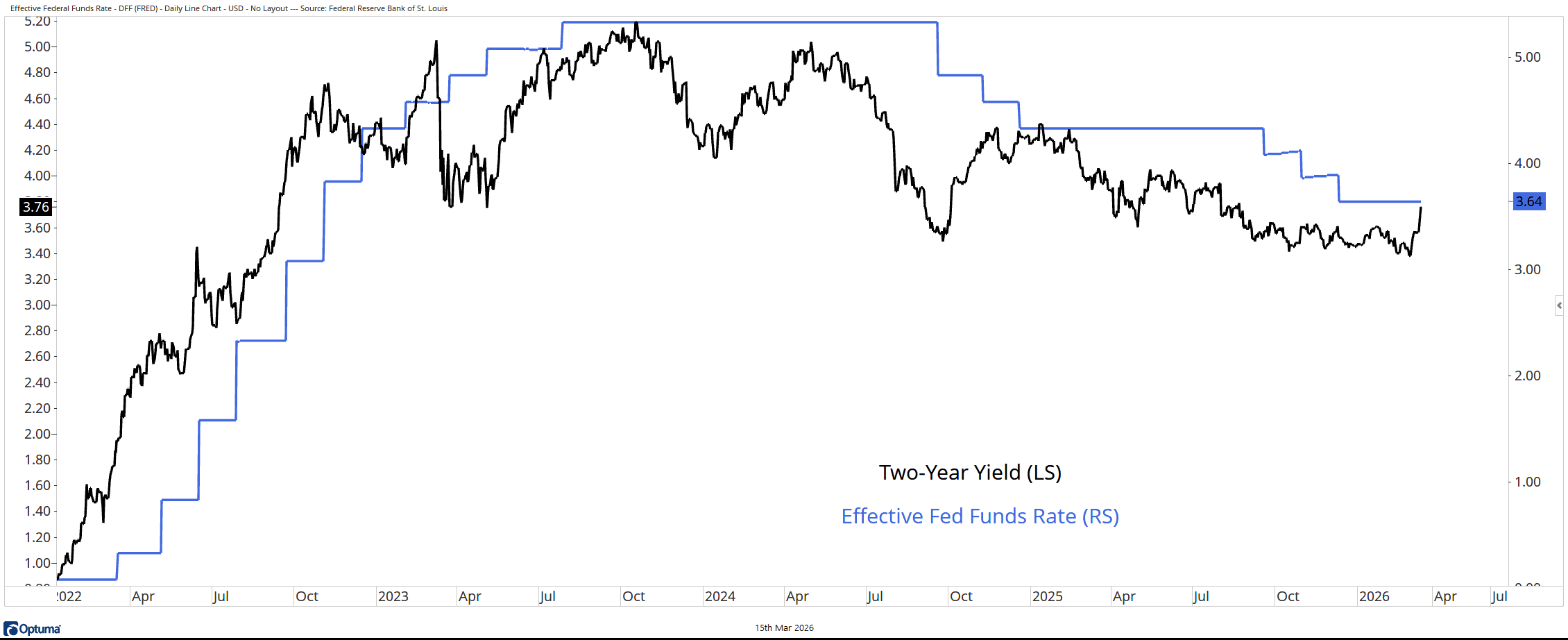

The Two-Year Yield and the Effective Fed Funds Rate

Rising commodity prices are putting upward pressure on inflation expectations. The Two-Year Treasury yield surged last week and is now in line with the current Effective Fed Funds Rate.

In plain English, the bond market is removing rate cut expectations from the equation—for now.

Source: Optuma

Final Thoughts

The S&P 500 is rolling over as the weight of the mega cap Mag Seven-type names becomes too much to bear. At the same time, a massive spike in commodity prices has put upward pressure on inflation, forcing the bond market to rethink rate cuts in 2026.

PFM-318-20260316