From Transitory to Temporary: Preparing for Powell’s Exit

There is an irony to how this may end. The Fed Chair most associated with the word “transitory” is now entering a transition period of his own.

On May 15, Jerome Powell’s current term as Chairman of the Federal Reserve is set to expire. Yet he may not leave the stage. Powell could remain in place as Chair Pro Tempore while Kevin Warsh’s nomination remains frozen due to a different type of blockade.

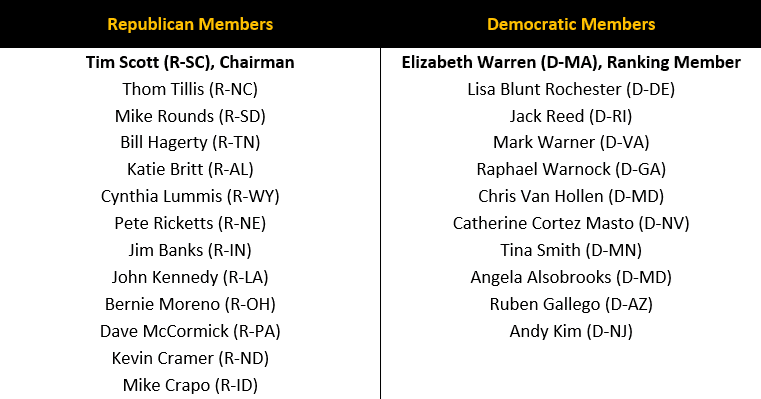

While Warsh appeared before the Senate Banking Committee Warsh. on April 21, Senator Thom Tillis (R-NC) has indicated he will not support the nomination until the Department of Justice (DOJ) investigation into the Fed’s renovation project is resolved. With the Committee split 13 Republicans to 11 Democrats, his vote is pivotal. Currently, any vote would likely result in a deadlocked 12-12 vote.

Figure 1. Current Senate Banking Committee Members

Sources: United States Committee on Banking, Housing, and Urban Affairs. Date as of April 21, 2026.

That leaves three broad paths.

First, the investigation concludes quickly and clears the way for confirmation. This seems unlikely given there have been no hints that the investigation is set to wrap up.

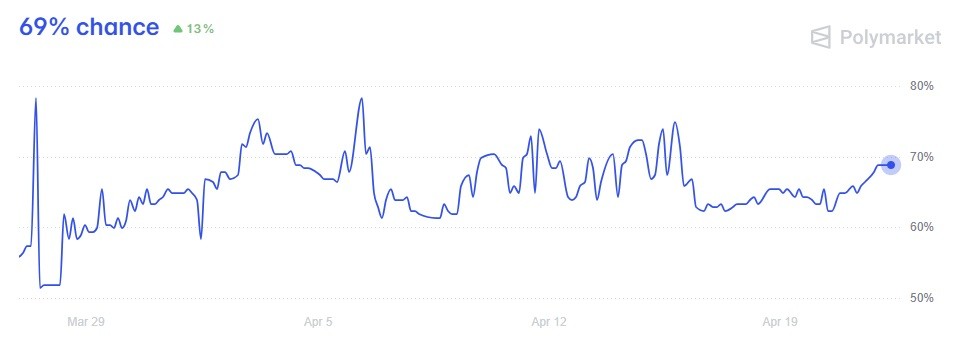

Second, the matter shifts from the DOJ to congressional oversight, turning a criminal overhang into a political one. That could be enough to break the blockade and seems like a viable option with betting markets thinking this could happen by the end of June (see figure 2).

Figure 2. Polymarket Odds that Trump Drops Powell Investigation by June 30 (%)

Sources: Polymarket (Trump drops Powell investigation by…? Predictions & Odds 2026 | Polymarket) and Potomac. Data as of April 22, 2026. Note: Political betting market odds are forecasts. All forecasts are expressions of opinions and are subject to change without notice and are not intended to be a guarantee.

Third, Powell stays on temporarily while Washington sorts itself out. This is a more complicated option because President Trump could attempt to remove him from that post should he choose to stay. The legality of such a move is debated, but some believe the President could remove Powell as Chair, but not as a Governor.

If President Trump does remove him, he could appoint Vice Chair Philip Jefferson, Governor Christopher Waller, or Governor Michelle Bowman as Chair of the Board of Governors. He could not, however, appoint the Chair of the Federal Open Market Committee, as that position is selected by the Committee itself. While having one member as Chair of the Board and another as Chair of the FOMC is possible in theory, it has not happened in the modern Fed era.

Technically, this could leave Chair Powell as the leading voice of monetary policy regardless of the President’s wishes until the Warsh logjam breaks. Our suspicion, however, is that the more likely outcome is a quiet de-escalation of the case, or a push toward a non-criminal resolution and the Tillis blockade comes to an end.

The Real Question for Investors

Our base case remains that Warsh ultimately becomes Chair. The real question for investors is not who holds the title in May, but whether the policy regime changes afterward. The larger risk may not be an immediate change in the rate outlook, but a different reaction function over time.

In our view, markets appear far less sensitive to Fed succession drama than they might have been earlier in the cycle. Additional rate cuts have already been priced out this year amid higher commodity prices, geopolitical risk, and renewed inflation concerns. If the Fed is already seen as on hold (see figure 3), the immediate occupant of the Chair may matter less in the near term.

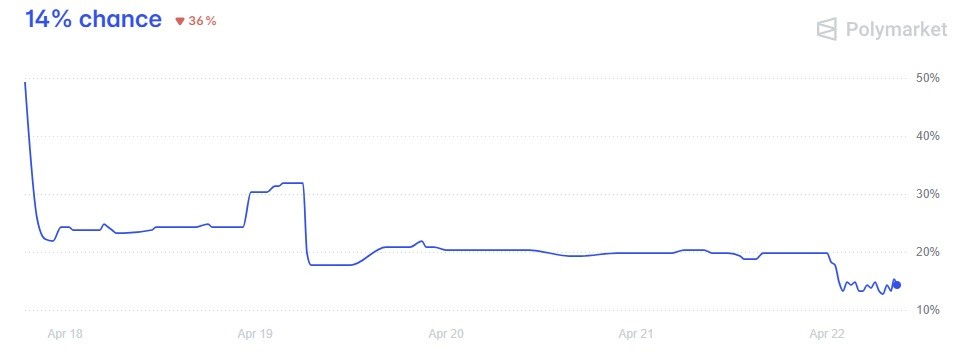

Figure 3. Polymarket Odds Kevin Warsh Cuts Rates at First Fed Meeting (%)

Sources: Polymarket (Kevin Warsh cuts rates at first Fed meeting? Predictions ... 2026 | Polymarket) and Potomac. Data as of April 22, 2026. Note: Political betting market odds are forecasts. All forecasts are expressions of opinions and are subject to change without notice and are not intended to be a guarantee.

That does not mean leadership is irrelevant. A Warsh-led Fed could look different in style and communication. Warsh has argued against heavy reliance on forward guidance. In practical terms, that could mean fewer signals ahead of meetings, more emphasis on actual decisions, and greater volatility around FOMC announcements. Markets accustomed to telegraphed outcomes may need to adjust.

A less telegraphed Fed could also raise event-risk premia around policy meetings, increase the value of diversification, and create a wider trading range for rates and equities during key decision windows.

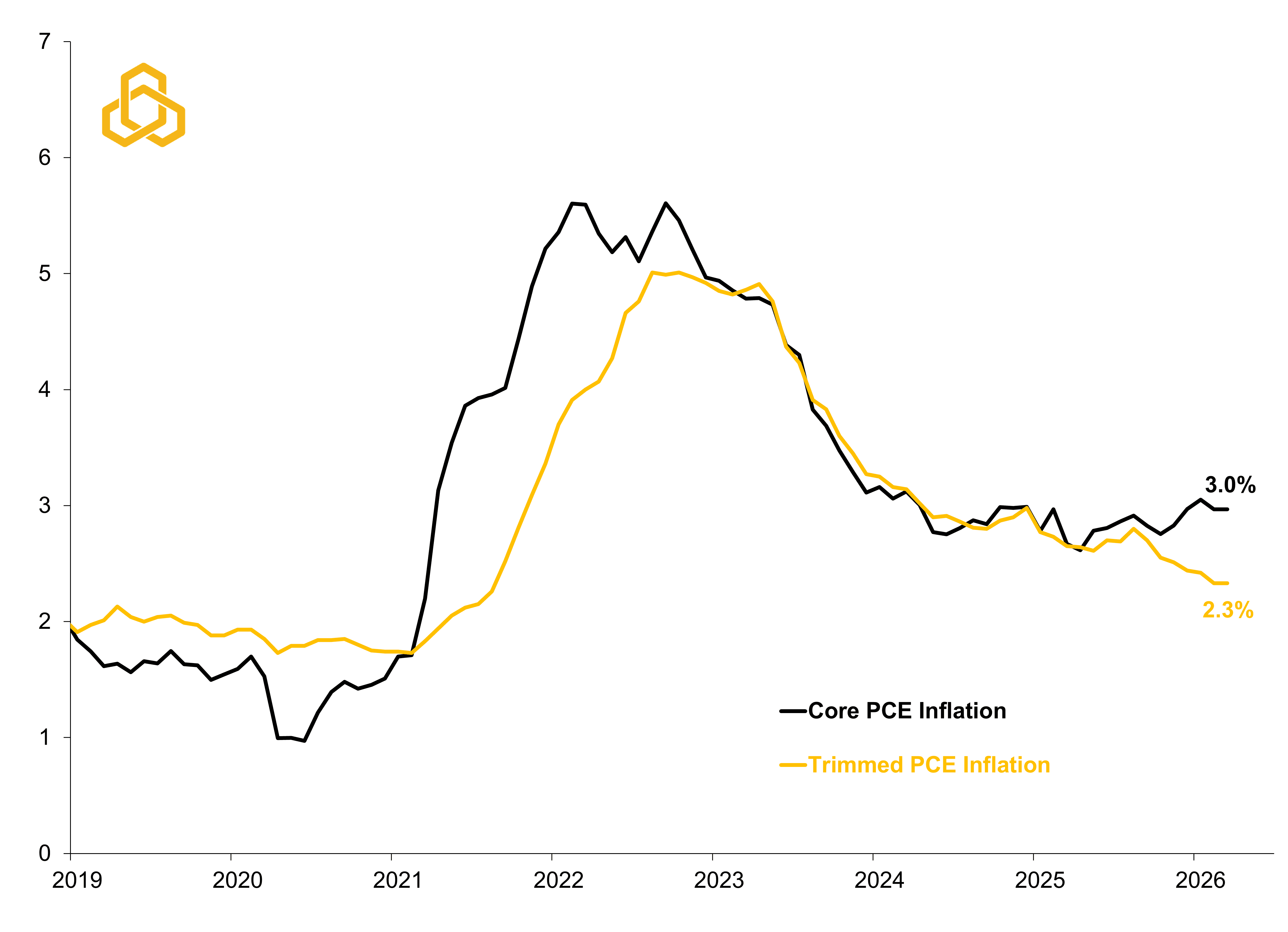

Warsh has also pointed to measures such as trimmed personal consumption expenditure (PCE) inflation, which is an inflation metric compiled by the Federal Reserve Bank of Dallas that removes the largest increases and decreases across all categories to get a more fundamental read on inflation. By using such a metric, Warsh seems to believe that it could keep the Fed from reacting to headline moves in inflation data (see figure 4).

Figure 4. Core PCE Index vs. Trimmed PCE Index (YoY%)

Sources: Bureau of Economic Analysis, Federal Reserve Bank of Dallas, Bloomberg L.P., and Potomac. Data as of March 2026. Note 1: Core PCE is the personal consumption expenditure chained price index, excluding food and energy and is a measure of inflation that the Fed follows closely instead of the consumer price index (or CPI). Note 2: The trimmed PCE metric removes the largest price increases and decreases across all categories and can be viewed as a cleaner signal of inflation.

There could also be secondary changes: less emphasis on the so-called dot plot, a different tone from Governors, and a greater willingness to offset lower rates with balance-sheet reductions over time. However, we think that the change of guard may not be as disruptive as some think due to the constraint of the recent geopolitical inflation shock.

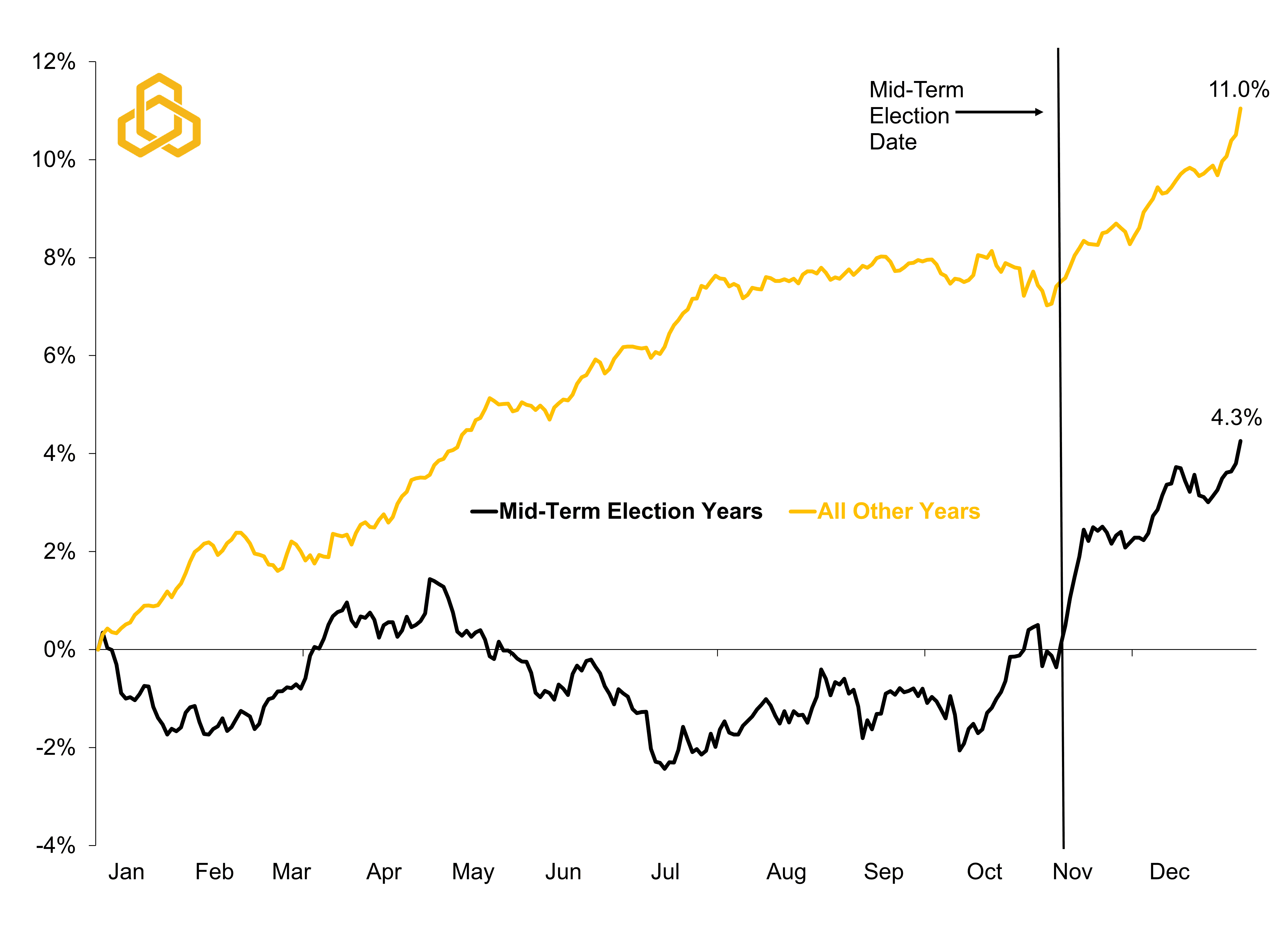

In the end, May 15 may be the wrong political date to watch with the midterm elections in November probably being the more important market-moving event. Since 1950, midterm years have often seen weakness into late summer and early fall before stronger year-end performance once political uncertainty begins to clear (see figure 5).

Figure 5. S&P 500 Index Average Returns Since 1950 (%)

Sources: Standard & Poor’s, Bloomberg L.P., and Potomac. Data as of December 31, 2022. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

Warsh may dominate headlines this spring, but the midterm elections in November will probably matter more than whomever holds the Chair title in May.

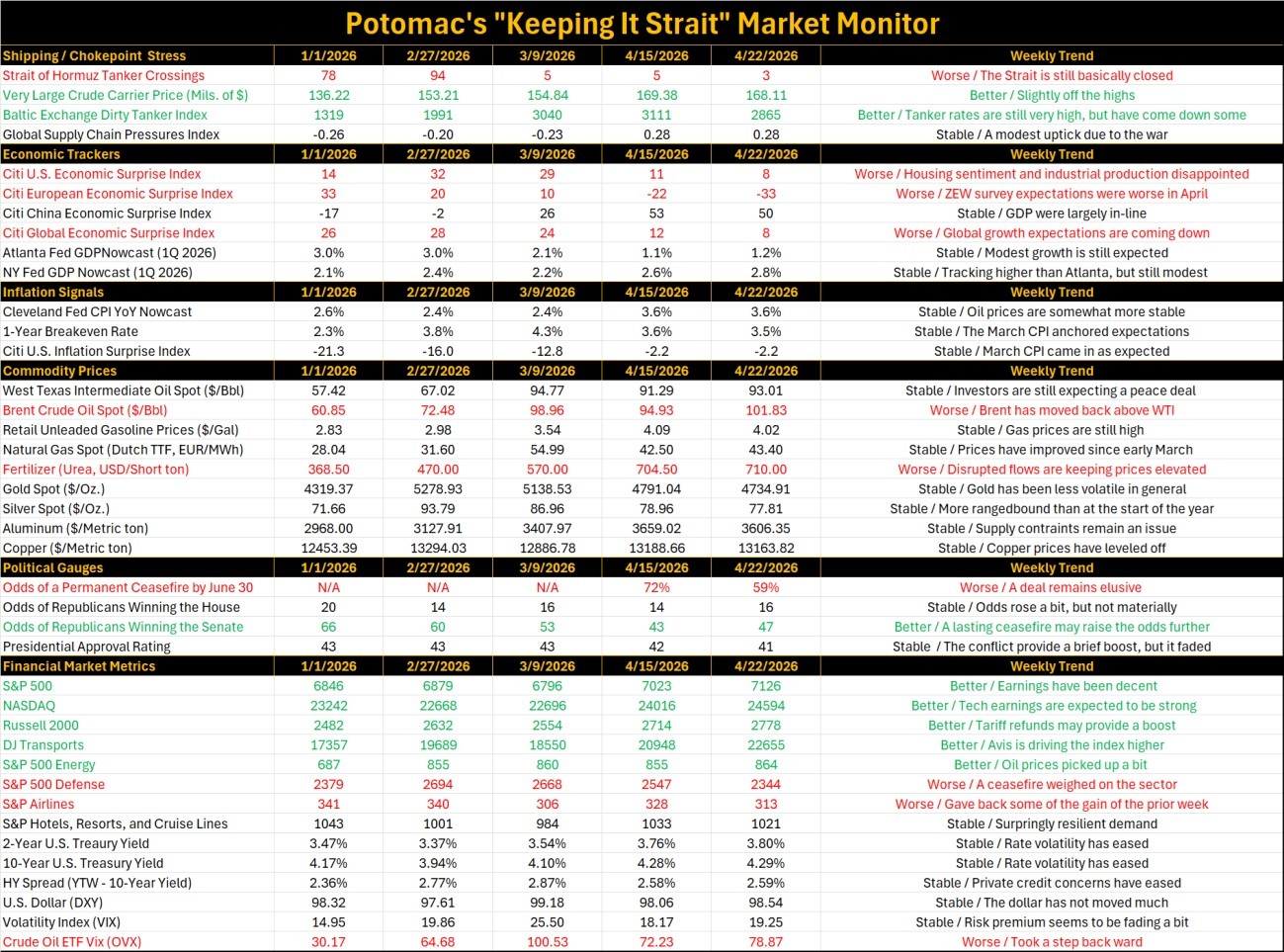

Weekly “Keeping it Strait” Highlights:

Despite ceasefire extensions, the Strait of Hormuz effectively remains shut with only 3 tankers making it through during the past week. The odds of a permanent ceasefire by June 30 slipped from 72% last week to 59% currently.

Economic surprise indices in the U.S. and Europe worsened with industrial production and ZEW survey expectations pulling down the indices, respectively. The Citi European Economic Surprise index has fallen from 33 at the start of the year to minus 33 currently (a reading below 0 is consistent with economic data missing expectations).

The odds of Republicans winning the Senate increased from 45% to 47% on hopes that an end to the Iran conflict could bring down gas prices.