No More Goldilocks for Gold? Here is What Changed.

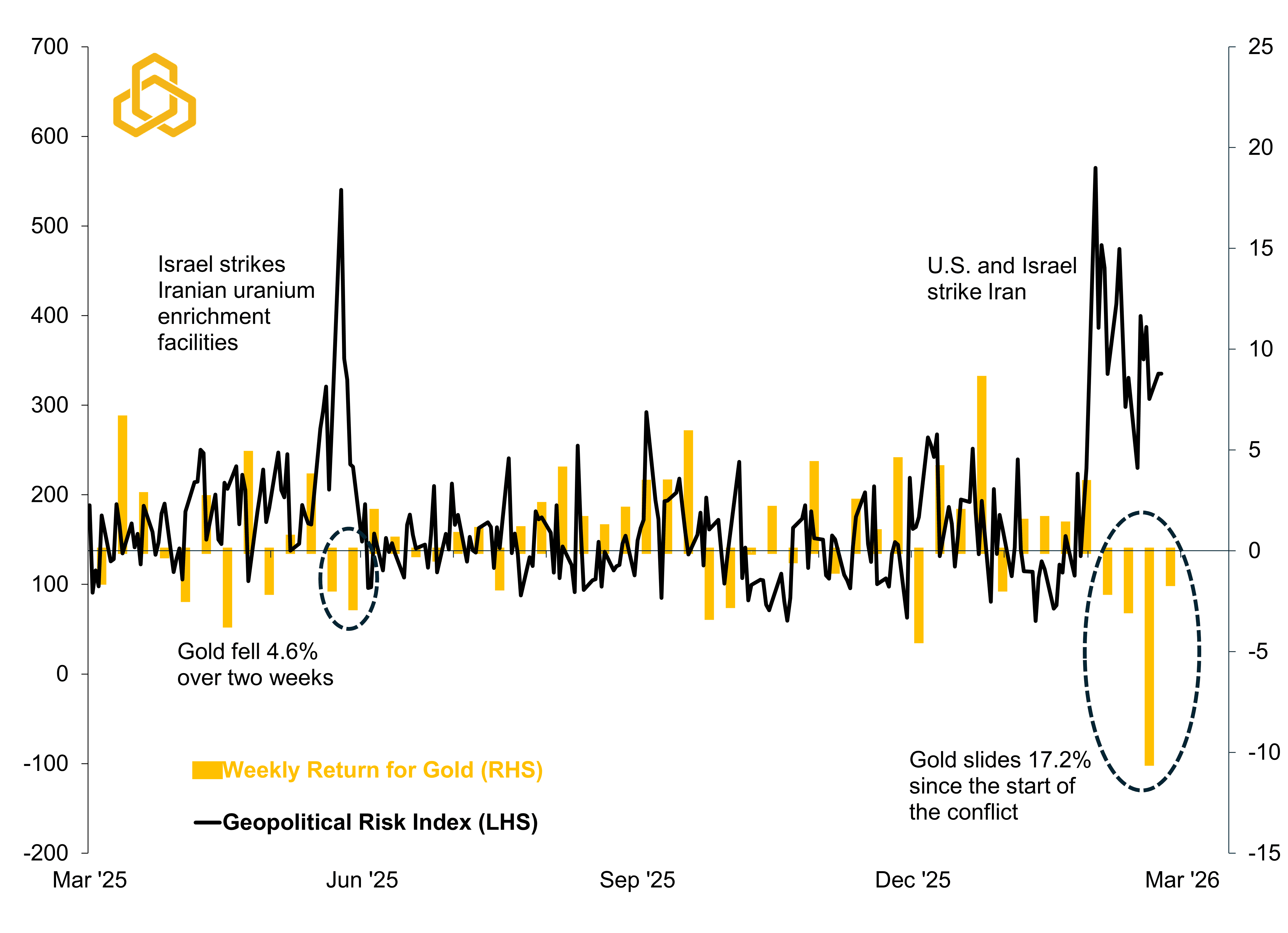

Gold prices have tumbled 17.2% since March 2nd while geopolitical tensions in the Middle East continue to simmer with strikes on oil infrastructure becoming an increasing threat should talks fail (see figure 1). Why isn’t the safe-haven working?

We have heard some say that it is because investors are selling what they can due to liquidity issues, to lock in gains, or that central bank demand is fading. We have heard that one several times. However, we think it largely has to do with rising uncertainty about monetary policy.

Figure 1. Caldara Iacoviello Geopolitical Risk Index (%) vs. Gold Prices ($/Oz.)

Sources: Bloomberg L.P. and Potomac. Data as of March 23, 2026.

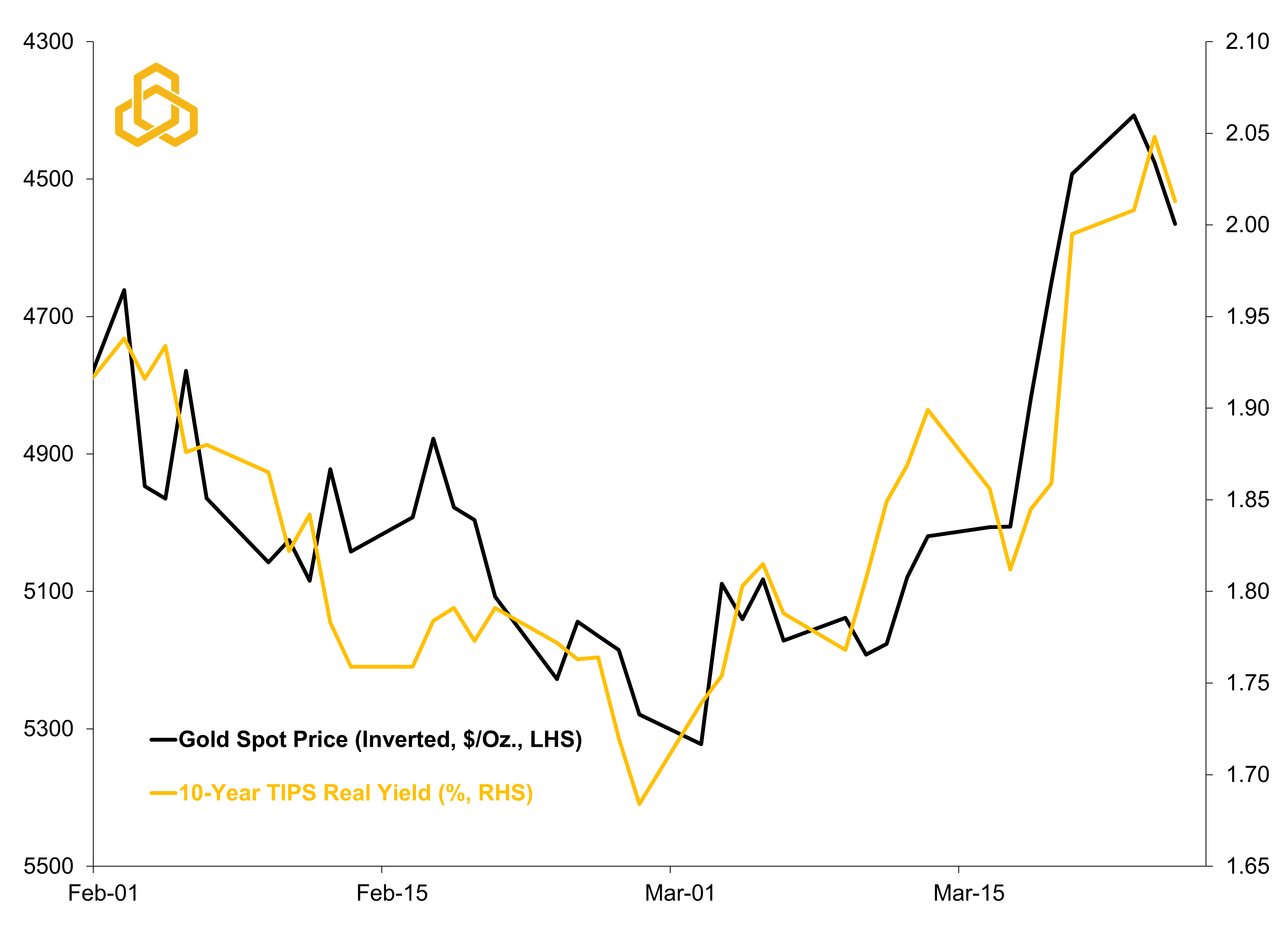

Gold is a non-yielding asset. While rising inflation expectations would normally increase the appeal of holding gold, the path for monetary policy is highly uncertain right now and that is reducing the desire to hold non-interest-bearing assets like gold. This relationship broke down in mid-2023 as central banks ramped up gold purchases, but it appears to be reasserting itself following the recent surge in real yields (see figure 2).

Sources: U.S. Department of Treasury, Bloomberg L.P., and Potomac. Data as of March 24, 2026.

The reason this relationship exists is because financial instruments like the two-year U.S. Treasury yield and the 10-year Treasury Inflation Protected Securities (TIPS) real yield are repricing the future path of Fed policy in advance of actual Federal Open Market Committee (FOMC) rate decisions. Even though the Fed is still forecasting one more rate cut in 2026, the futures market disagrees.

Typically, the Federal Reserve focuses on core inflation, which excludes food and energy prices, because they can be volatile due to geopolitics, weather, or other forces that do not truly reflect that state of the underlying economy. However, the recent conflict in Iran is bringing that into question with traders starting to price out rate cuts for the remainder of the year and even considering a rate hike in response to the closure of the Strait of Hormuz.

Federal Reserve Bank of Chicago President Austan Goolsbee summed up the confusion well by saying, “We could be back to an environment with multiple rate cuts for the year if inflation behaves…and I could see circumstances where we would need to raise rates if it was going a different way, and inflation was getting out of control.”

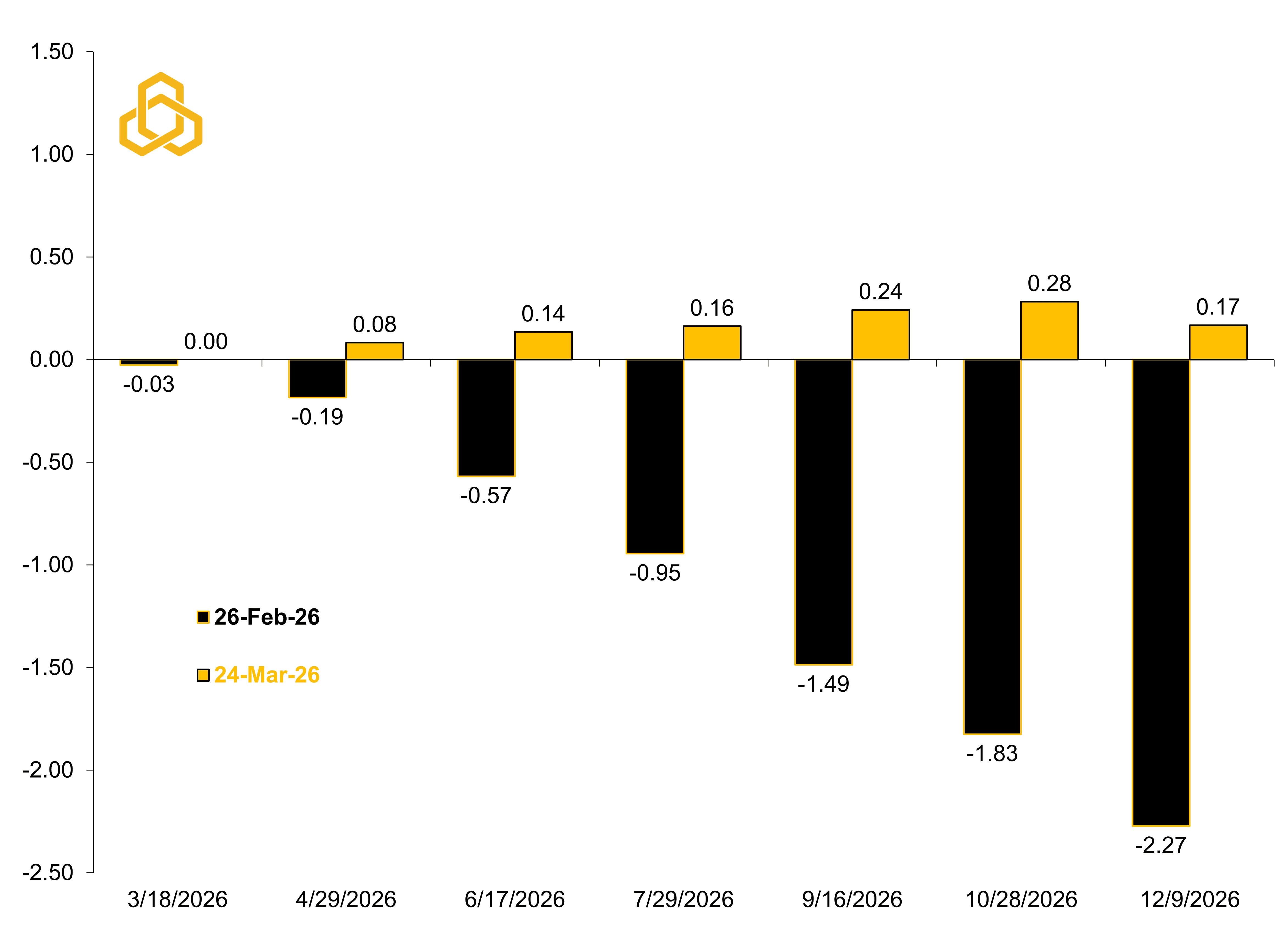

At the time of this writing, the market believes there is roughly a 23% chance of a rate hike by yearend. It sees just 7% odds of a rate cut. This is a rapid change from just one day before the initial strike when the market was fully pricing in two rate cuts by year end (see figure 3).

Figure 3. Fed Funds Futures Implied Number of Rate Cuts/Hikes

Sources: CME Group, Bloomberg L.P., and Potomac. Data as of March 24, 2026. All forecasts are expressions of opinion and are subject to change without notice and are not intended to be a guarantee.

This is a bit surprising to us because the Federal Reserve already had time baked in with the next rate cut not expected until at least July even before the war started. In our opinion, that should give them enough time to assess the inflationary impact of the conflict with betting markets suggesting a potential ceasefire by summer.

While it will take several months to get official inflation data, oil prices react immediately, and the Fed should have a reasonable idea of how oil prices will impact inflation ahead of the official data releases. That said, Chair Powell has shown many times before that the Committee operates with an abundance of caution and can be slow to react.

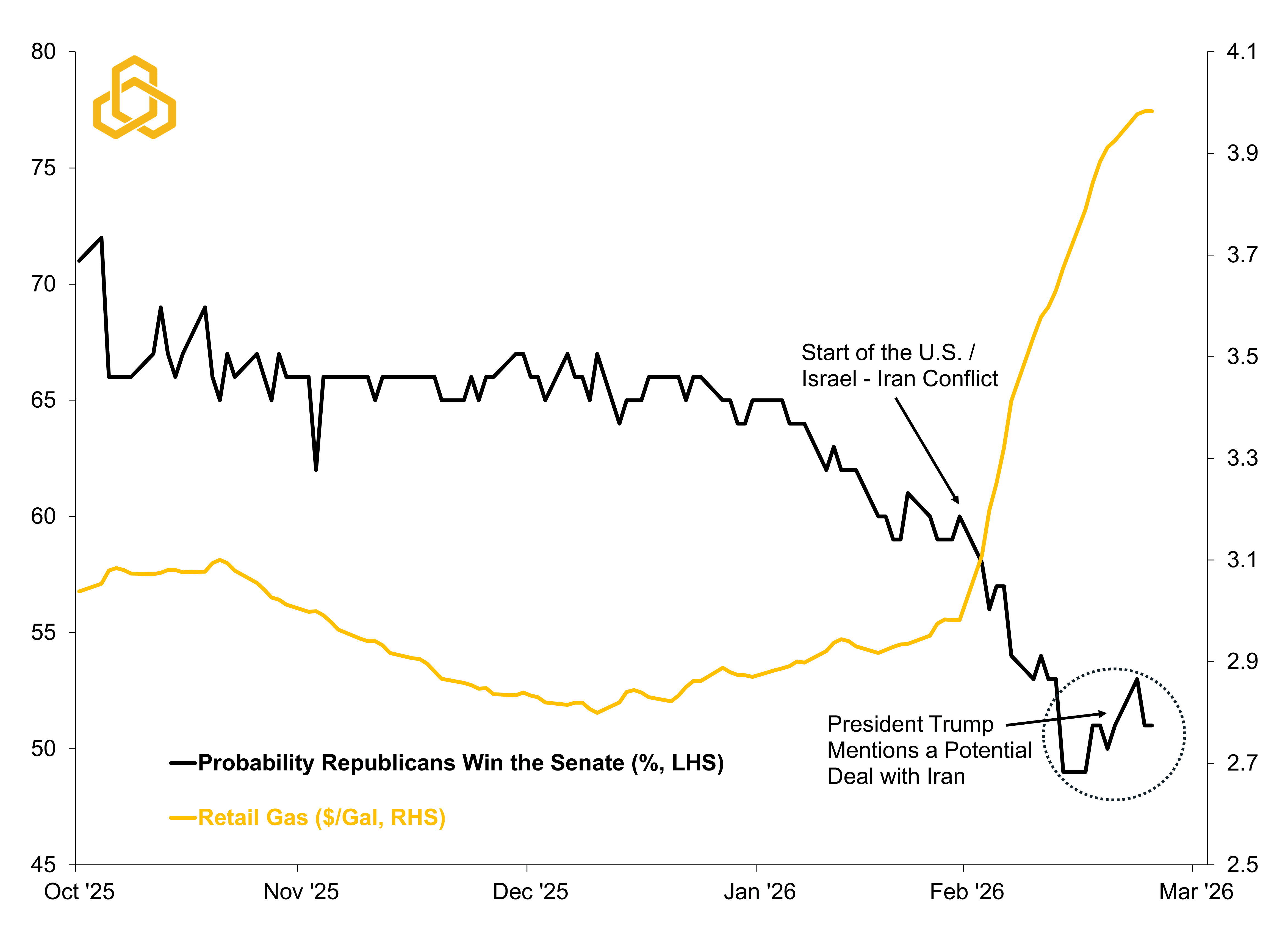

Only time will tell, but we suspect that rising political pressures in the U.S. ahead of the mid-term elections will incentivize a quicker de-escalation than markets currently anticipate (see figure 4).

Figure 4. Odds of Republicans Winning the Senate (%) vs. Gas Prices ($/Gal.)

Sources: Polymarket, American Automobile Association, and Potomac. Data as of March 23, 2026. All forecasts are expressions of opinion and are subject to change without notice and are not intended to be a guarantee.

As Benjamin Graham wrote in his book, The Intelligent Investor, “In the short run, the market is a voting machine…” and this would not be the first time that the bond market caused the President to change course with Liberation Day still fresh in our memories having occurred almost exactly one year ago. If accurate, this could easily put rate cuts back on the table this year and put some luster back into gold.

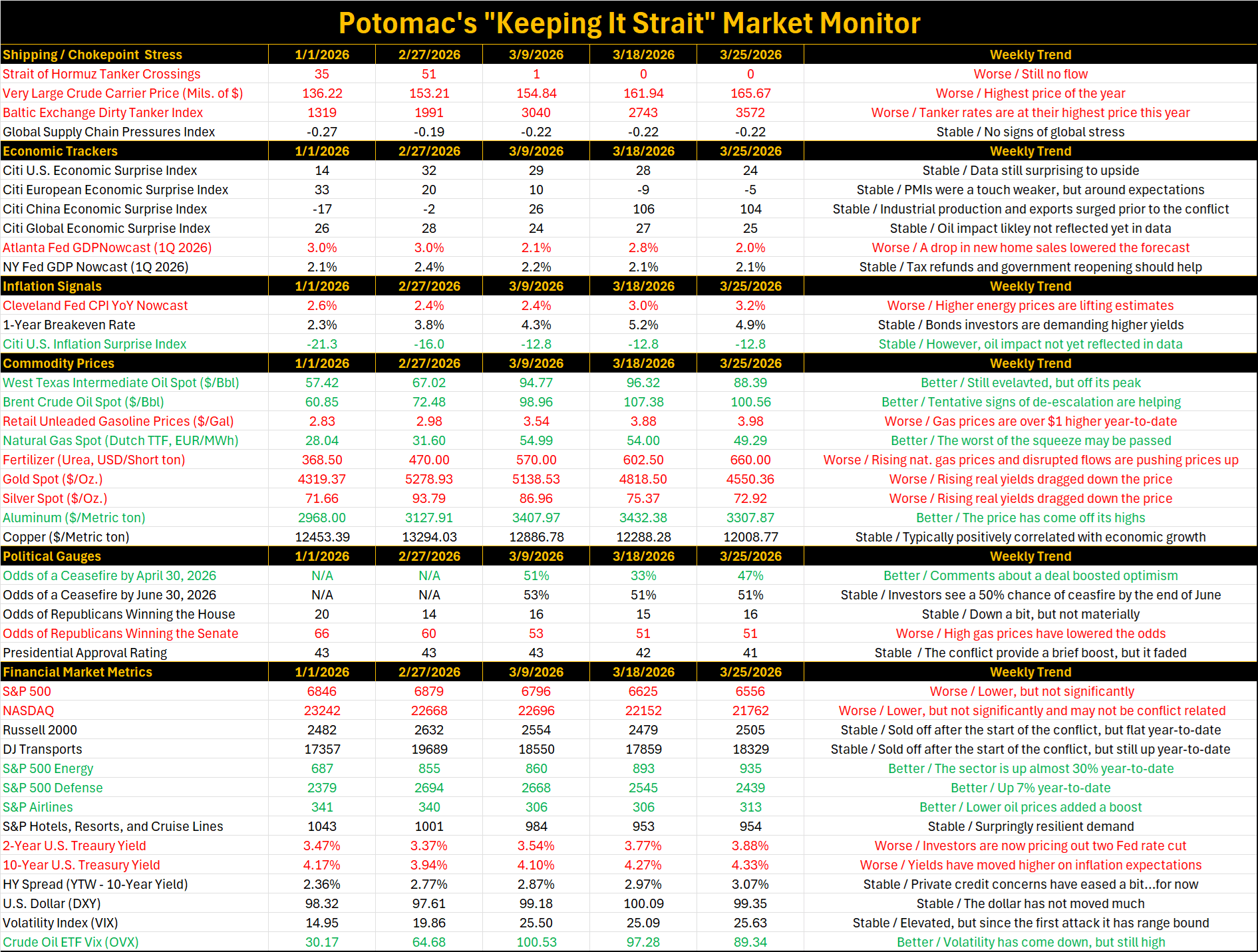

Weekly “Keeping it Strait” Highlights:

The Baltic Exchange Dirty Tanker Index, which measures the cost of shipping crude oil by sea hit an all-time high of 3,572 on record dating back to 1999. It started the year at 1,319.

The Atlanta Fed’s GDPNowcast slipped from 2.8% to 2.0% on weaker home sales and construction spending. It is now aligned with the New York Fed’s measure.

Crude oil volatility (OVX) came down from the previous week as comments of a potential U.S. – Iran deal eased tensions a bit.

The odds of a ceasefire by April 30, 2026 rose from 33% to 47% according to Polymarket’s betting platform.

Source: Bloomberg L.P. and Potomac. Data as of March 25, 2026. Note 1: The dates selected are 2/27/2026 (start of the conflict), 3/9/2026 (initial oil surge/peak as the Strait closed), and the latest week and previous week to compare the weekly trend. Note 2: Economic and inflation surprise index readings about zero imply that data are beating the consensus on average, below zero means that data are missing expectations. Note 3: In commodity prices, we ranked higher oil, natural gas, retail gas, fertilizer, and aluminum prices as bad for the economy because it weighs on growth, we ranked rising gold and silver prices are good due to the investor perspective. Note 4: Political betting market odds are forecasts. All forecasts are expressions of opinions and are subject to change without notice and are not intended to be a guarantee.

PFM-3019-20260319