Under Pressure

Dan Russo, CMT

March 9, 2026

As you read the title of this week’s note, I hope that, like me, you’re picturing Bowie and Freddie Mercury. And if you don’t know what I’m talking about, I can’t help you.

But pressure is exactly what the market is beginning to feel. For weeks, we’ve highlighted that megacap stocks have been making it difficult for the market to move higher, even as the “rest of the market” has been doing just fine.

Last week, the knees finally started to buckle under that pressure.

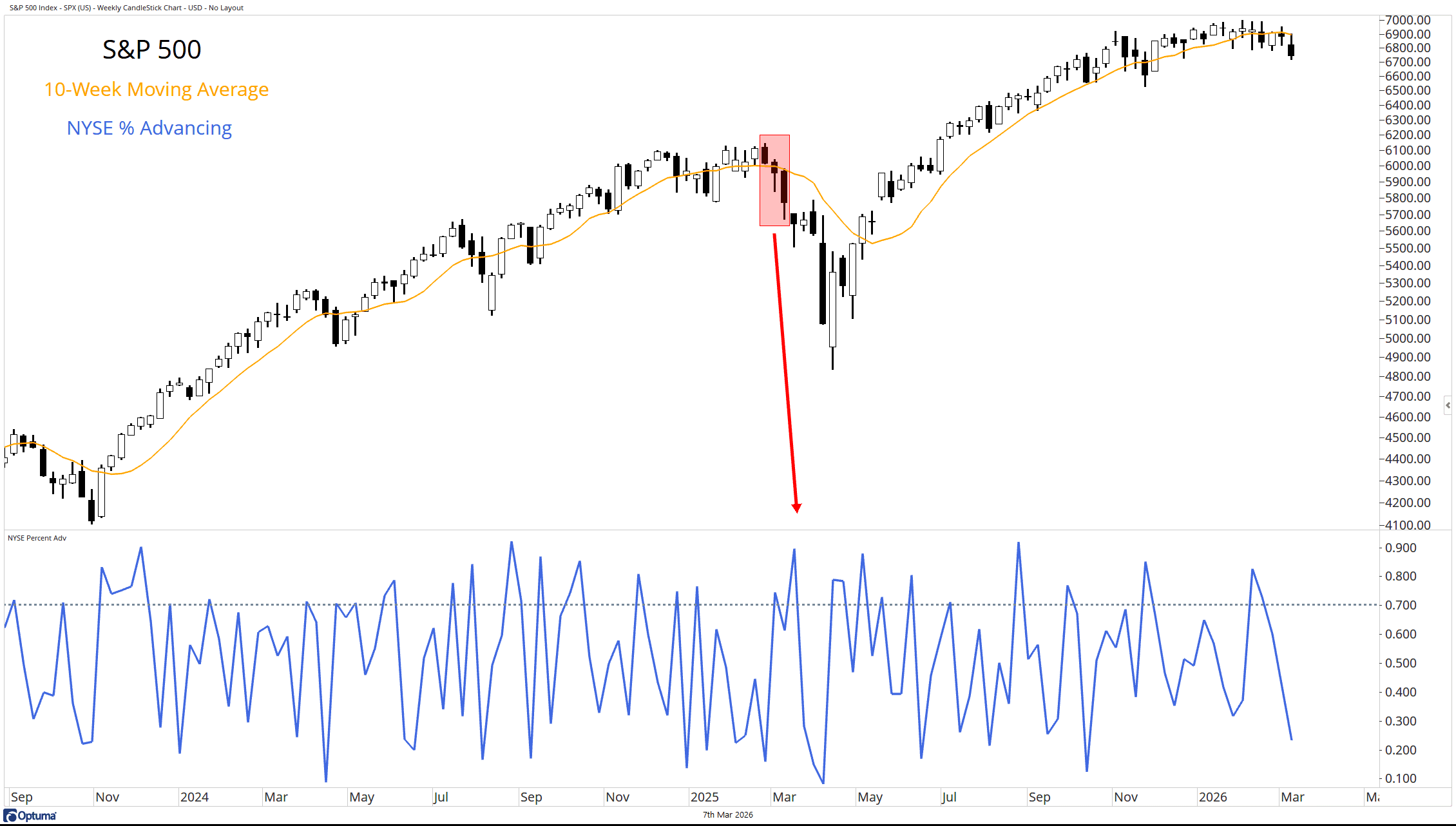

S&P 500

Since I’m writing from a different location today (Miami), I thought I’d start with a different chart. Here’s the S&P 500 with its 10-week moving average. For the second consecutive week, and the third time in the past four, the index closed below that moving average. More importantly, the moving average itself is now beginning to turn lower.

At the same time, the percentage of advancing stocks on the NYSE fell sharply last week, echoing the dynamic we saw in March of last year.

Source: Optuma

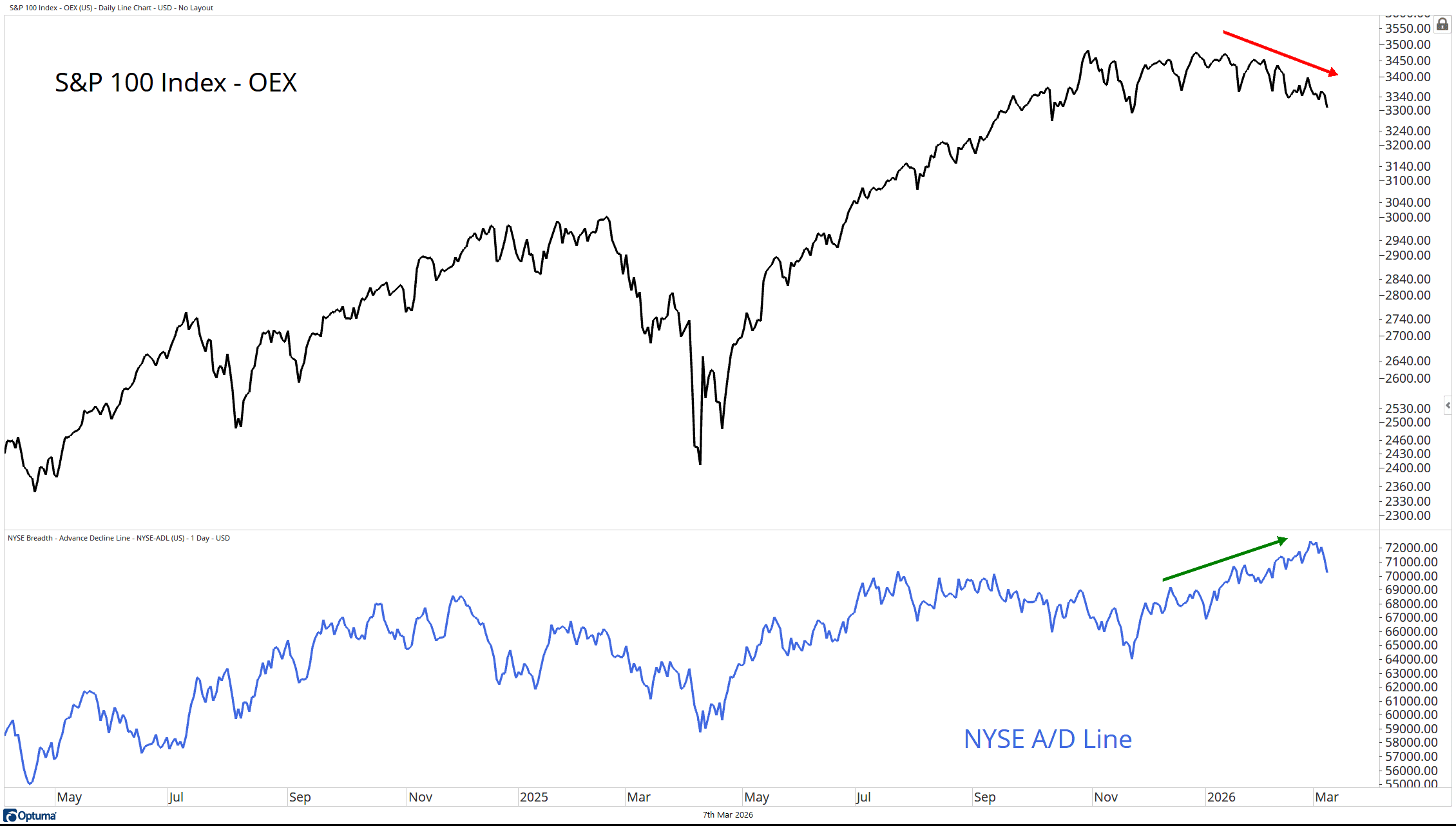

S&P 100

We don’t often feature the S&P 100, which according to Bloomberg is a capitalization weighted index of 100 highly capitalized stocks selected from the S&P 500 for which options are listed.

The index has been under pressure since October and made a new low for the year on Friday. It has also failed to confirm the NYSE Advance/Decline Line’s move to new highs, consistent with what we’ve been saying all along: the largest weights simply haven’t been participating.

Source: Optuma

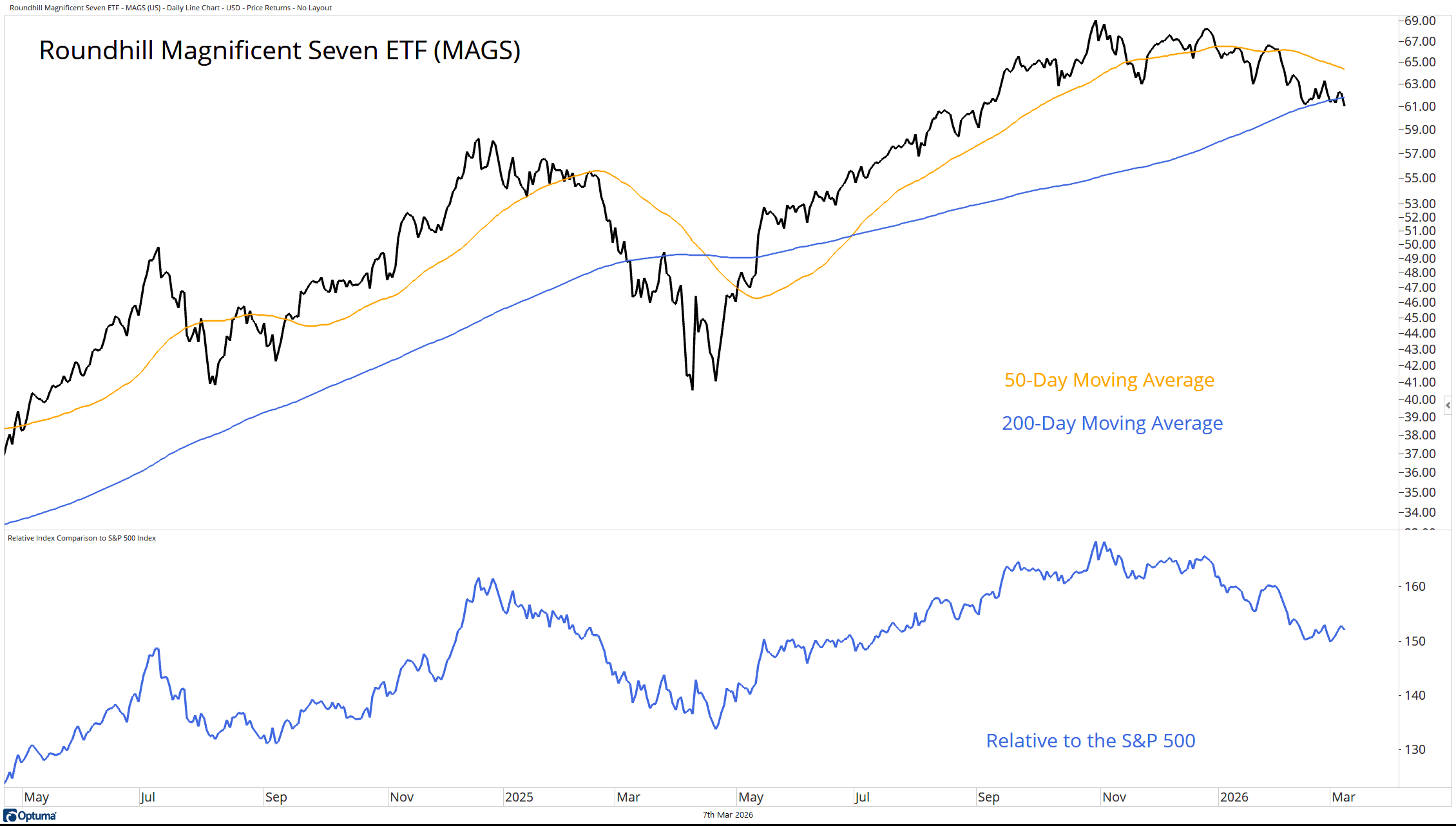

The Mag 7

Speaking of new lows for the year, the Roundhill Magnificent Seven ETF (MAGS) has joined the list. The fund now sits below both its 50 and 200-day moving averages and is in a clear downtrend relative to the S&P 500.

This is a lot of weight for the rest of the market to carry. For context, the Mag 7 stocks reside primarily in three sectors: Information Technology, Communication Services, and Consumer Discretionary. Together they account for more than 50% of the S&P 500.

If these groups continue to fall, who’s left to hold the market up? Materials at roughly 2%? Energy at 3.5%?

Source: Optuma

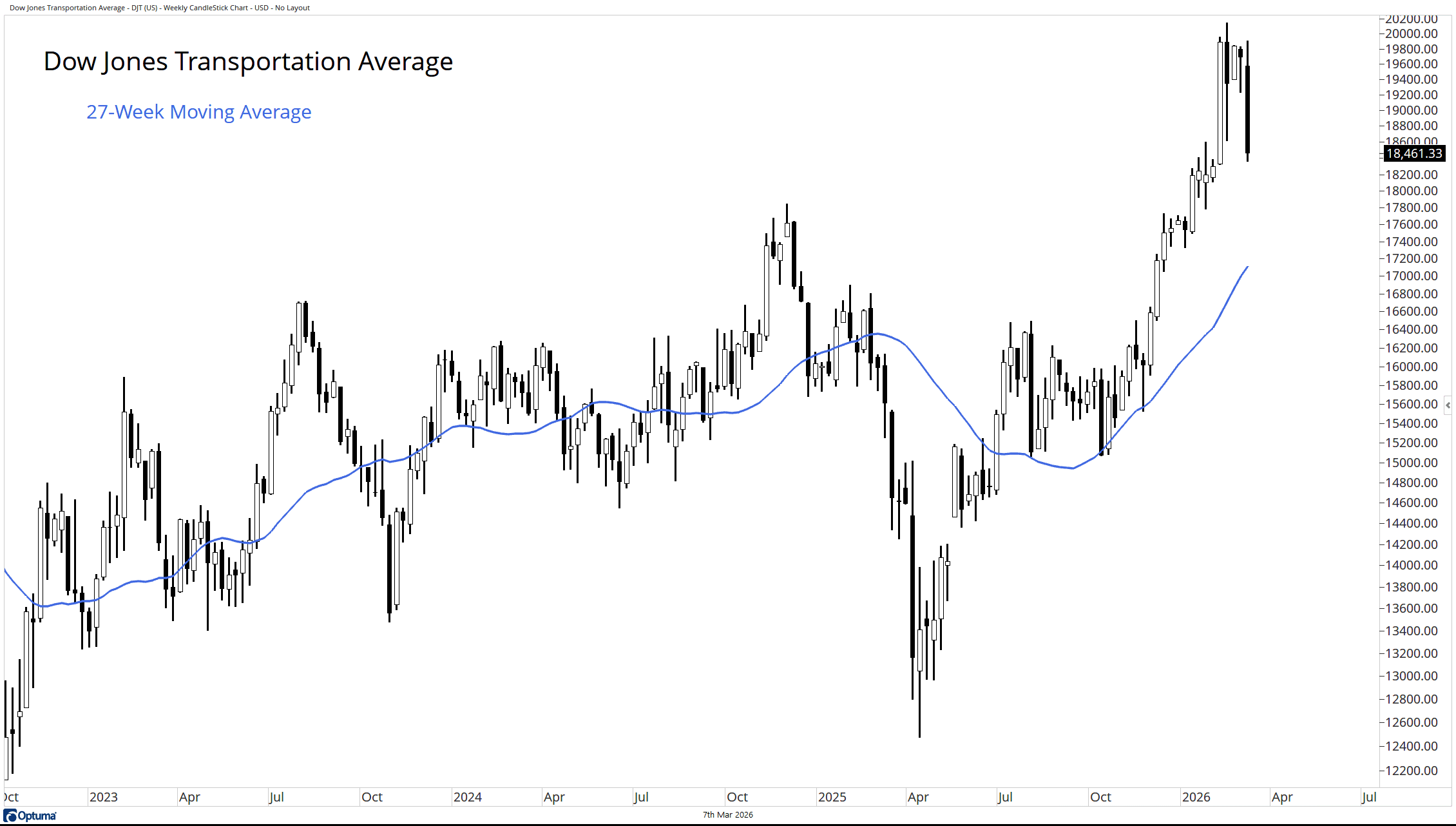

Dow Jones Transportation Average

Meanwhile, the Dow Jones Transportation Average came under pressure last week as well. While the index remains well above its rising 27-week moving average, last week’s action may have been an early warning that this key level is now coming into play.

Source: Optuma

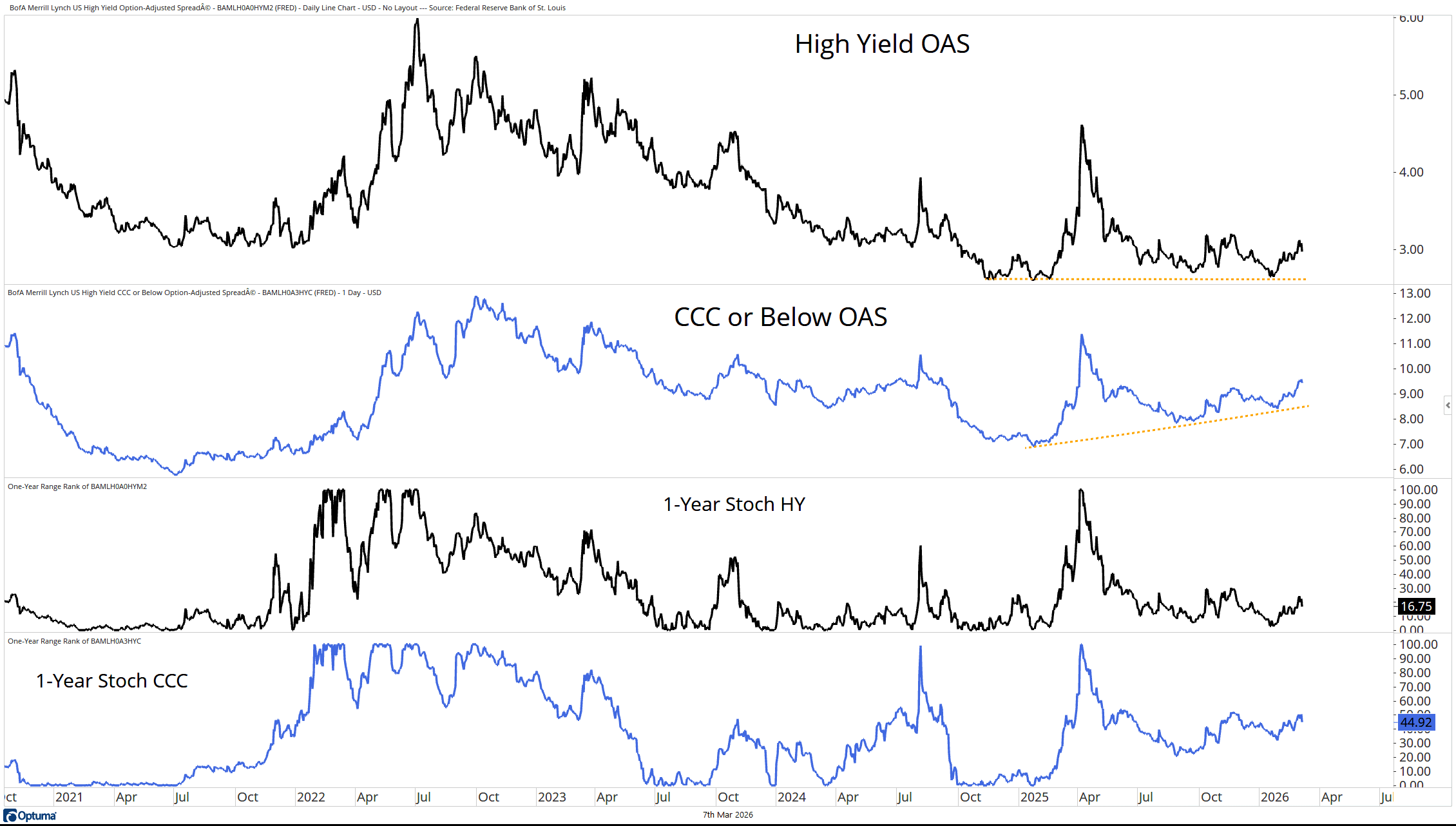

Credit

All of this is unfolding as credit markets are beginning to move top of mind for investors. Fair warning: this chart is a bit wonky, but bear with me.

An option-adjusted spread (OAS) measures the yield premium investors demand over Treasuries. The lower the spread, the less compensation investors require for taking credit risk.

In traditional high-yield bonds, spreads remain relatively tight, with the one-year stochastic below 17%. But in CCC-rated and below credits, investors are demanding an increasingly larger premium. The one-year stochastic there is approaching 45%.

In plain English, investors are growing more concerned about the worst-quality credit. The likely culprit is stress in private credit. Last week, BlackRock limited withdrawals from one of its private credit funds. Last month, Blue Owl did the same.

Source: Optuma

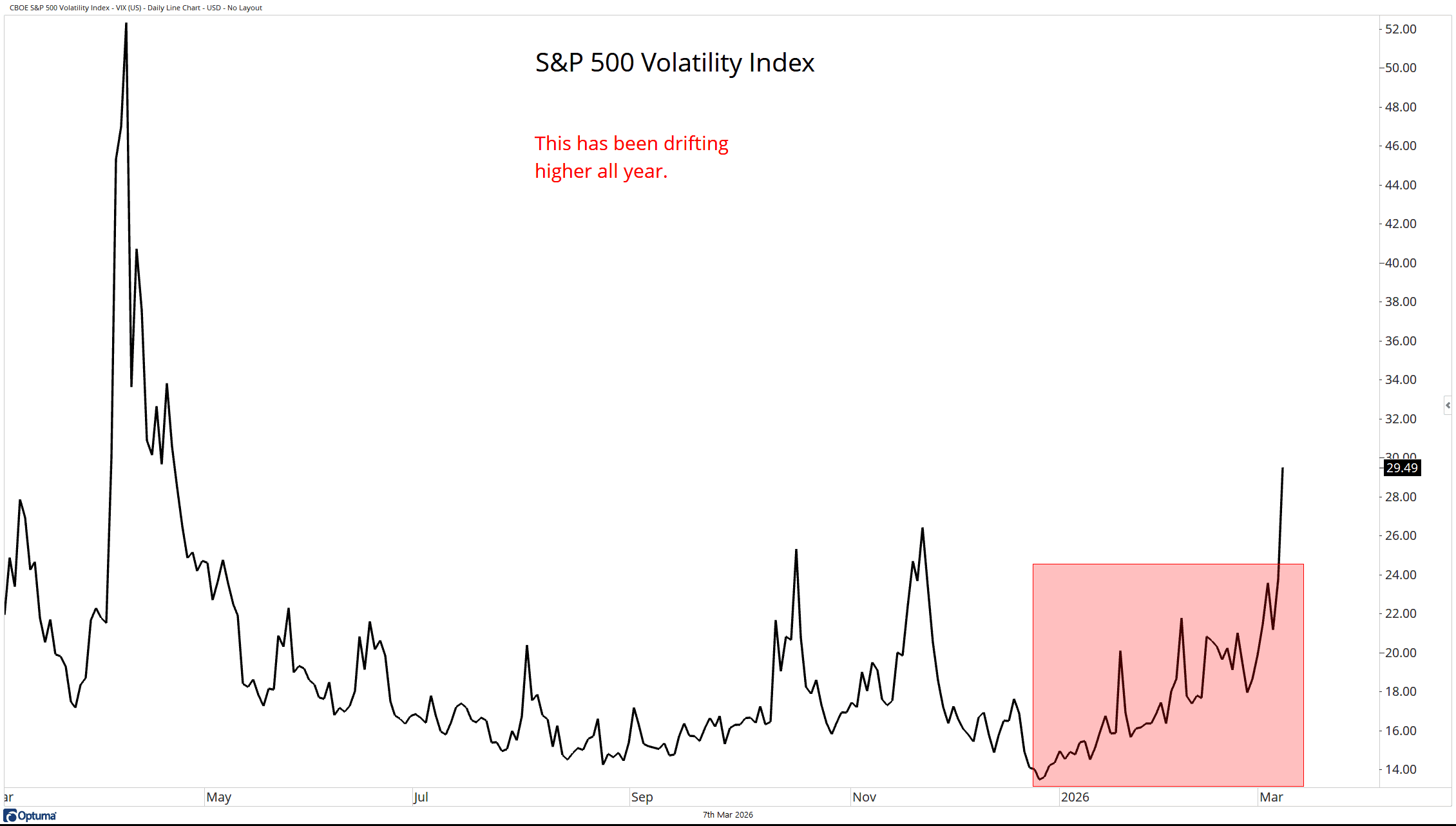

The VIX

All of the above contributed to a sharp spike in the S&P 500 Volatility Index last week. The move pushed the VIX to its highest level since last April’s “Liberation Day” tantrum.

Notably, we’ve been highlighting the rising trend in volatility all year.

Source: Optuma

Final Thoughts

The simple fact of the matter is, if the biggest stocks in the market can’t get into gear, there is only so much that the rest of the market can do. The “little guys” are starting to buckle under the pressure. There needs to be a catalyst for them to fully break…perhaps that will be the private credit market?

PFM-316-20260309