The concept of a K‑shaped economy gained traction during the COVID‑19 pandemic as economists tried to describe the shape of the eventual recovery. A “V‑shaped” recovery implies a sharp rebound, while an “L‑shaped” recovery suggests a slower and more prolonged period of stagnation. A “K‑shaped” recovery, by contrast, occurs when different segments of the population move in opposite directions.

In simple terms, the “rich get richer” as they benefit from a stimulus‑fueled stock market boom, while the “poor get poorer” as inflation erodes purchasing power.

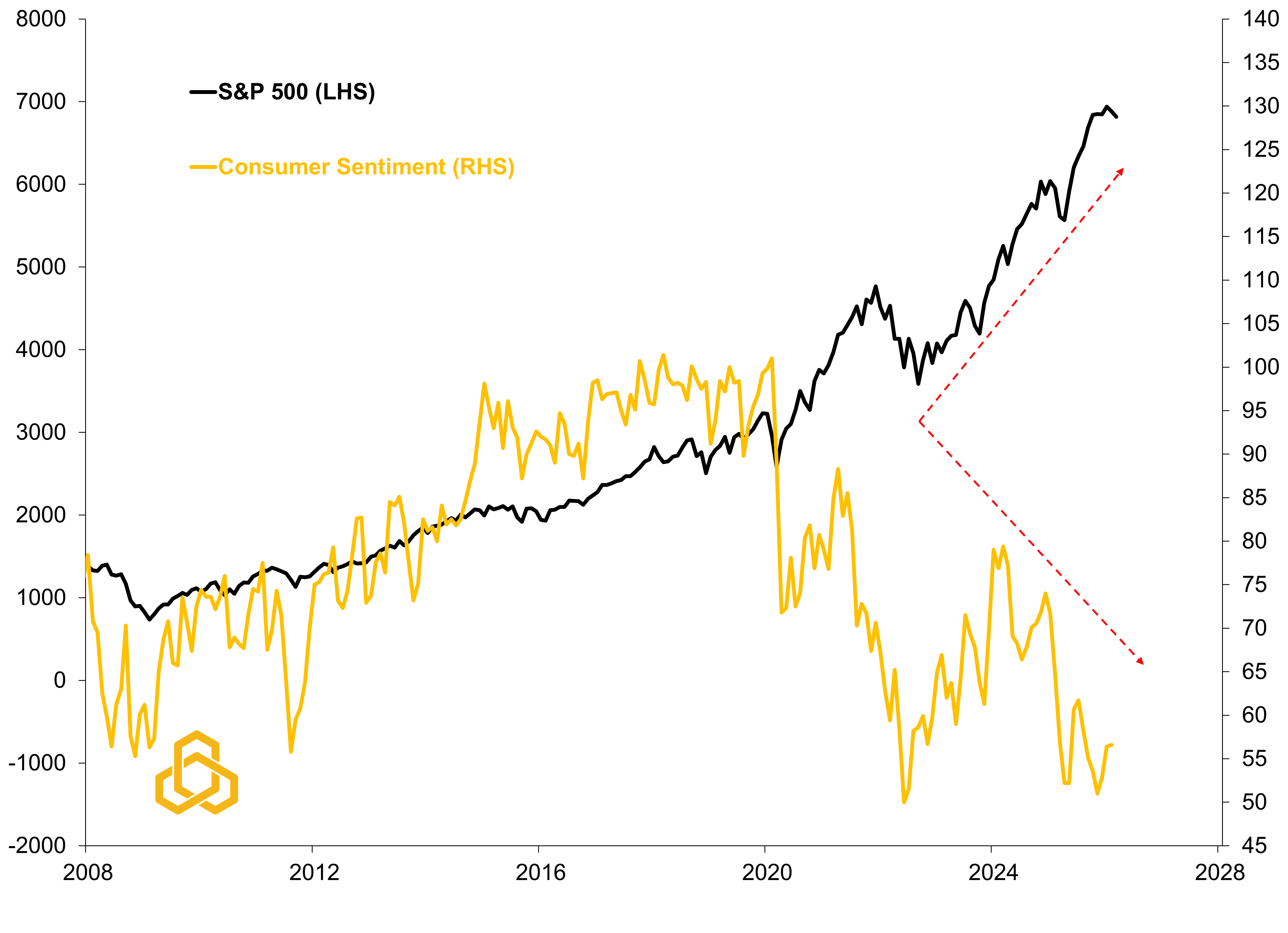

A simple comparison between the S&P 500 and consumer sentiment highlights this divergence and helps explain why policymakers continue to focus on affordability issues. When asset prices rise but sentiment remains depressed, it suggests that the benefits of economic growth are not being felt evenly (see Figure 1).

Figure 1. S&P 500 Stock Market Index vs. Consumer Sentiment

Sources: Standard & Poor’s, University of Michigan, Bloomberg L.P., and Potomac. Data as of February 2026. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

With the U.S./Israel–Iran conflict pushing oil prices higher, inflation pressures could re‑emerge in the months ahead. If that occurs, policymakers may once again attempt to offset the impact through fiscal or regulatory measures. The key question, however, is whether such measures will materially improve consumer confidence.

Under the Hood: Everyone is Miserable

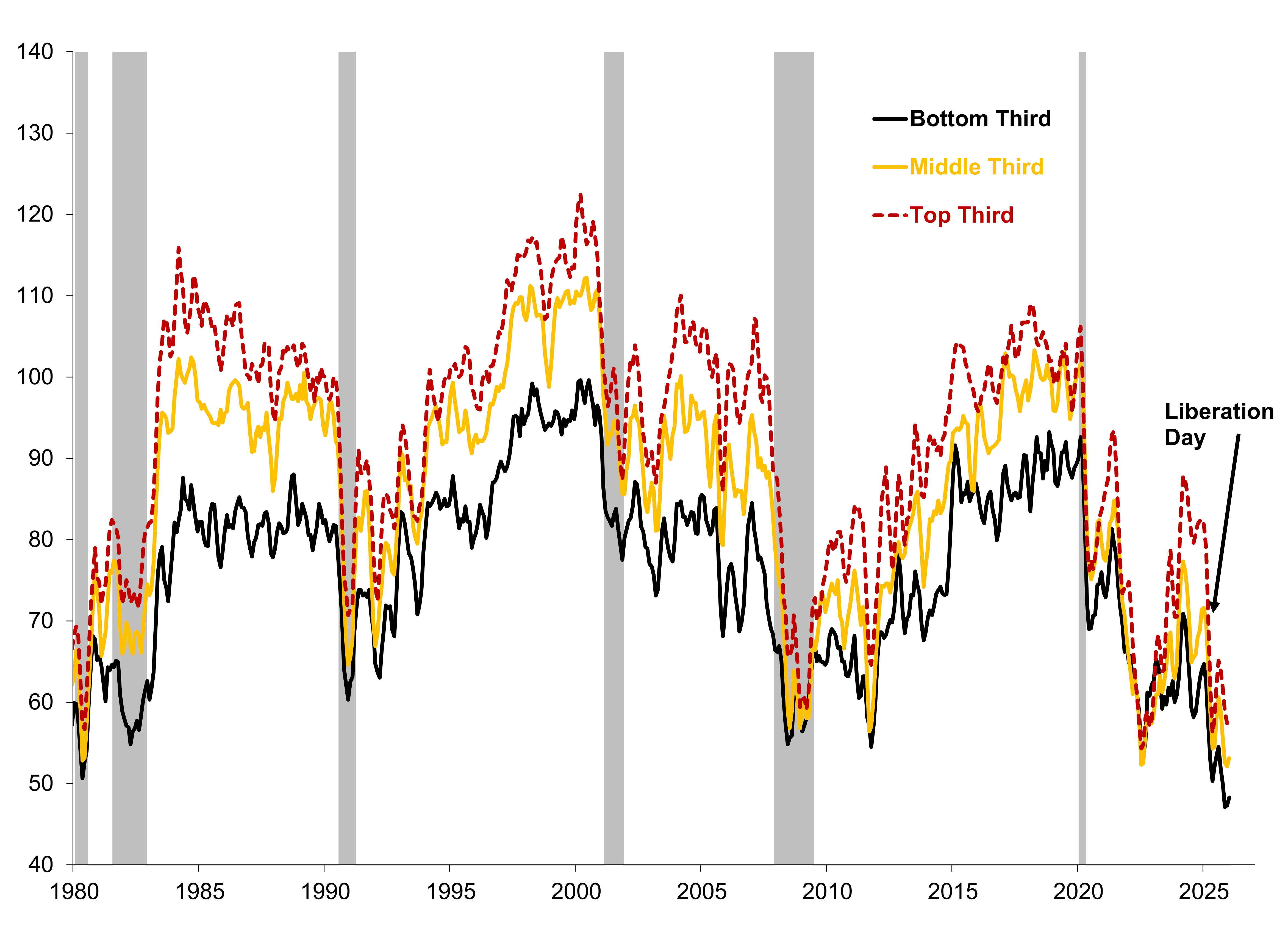

One underappreciated aspect of the current environment is that higher‑income earners are not particularly optimistic either. Despite a stock market that remains near record highs, sentiment among the top one‑third of income earners is still worse than it was during the Global Financial Crisis.

The only comparable episode occurred in July 2022, when inflation reached 8.5% and the S&P 500 had fallen 13.9% year‑to‑date (see Figure 2). In other words, sentiment among higher‑income households today resembles periods that historically coincided with far more severe market stress.

Figure 2. Consumer Sentiment by Income Tercile vs. Recession

Sources: University of Michigan, National Bureau of Economic Research, and Potomac. Data as of January 2026. Note: Shaded regions denote periods of recession.

Tariffs may have played a role in this deterioration. Consumer sentiment fell rapidly both before and after “Liberation Day,” with sentiment among higher‑income households declining particularly quickly. One possible explanation is that small business owners fall within higher income brackets and therefore feel policy shocks more directly.

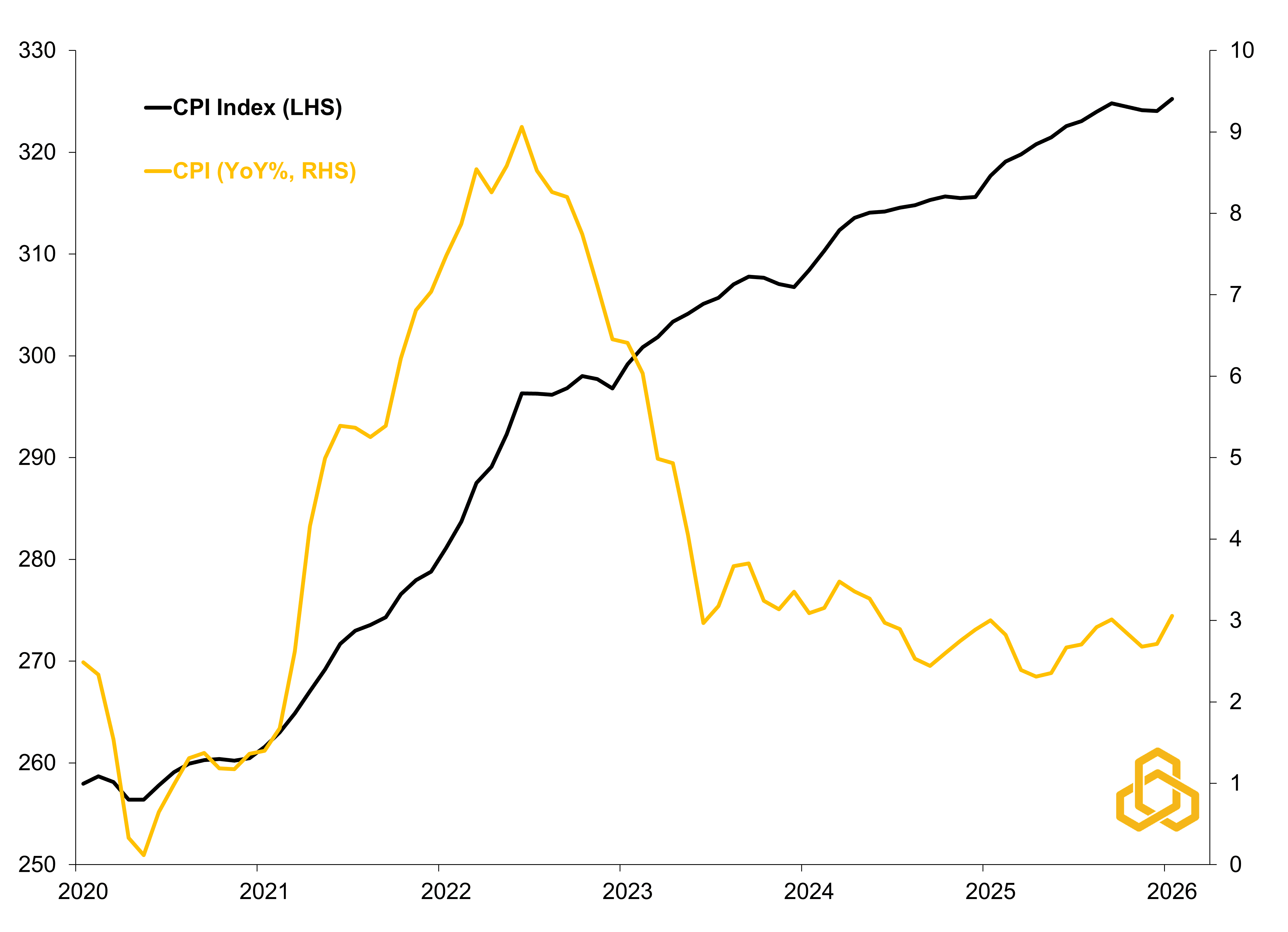

At the same time, the data suggest that consumers remain sensitive not only to the pace of inflation but also to the overall price level. Even when inflation moderates, the cumulative increase in prices continues to weigh on household perceptions of financial well‑being (see Figure 3). Although inflation is likely not the entire story.

Figure 3. Consumer Price Index Level vs. Year-on-Year (%)

Sources: Bureau of Labor Statistics and Potomac. Data as of January 2026.

Artificial Intelligence: The Consumer Sentiment Killer?

It would be difficult today to ignore the rapid rise of artificial intelligence. The technology is advancing quickly and companies across industries are investing heavily in it. While the productivity benefits may be significant, the transition period could prove disruptive.

Consider the current environment: the unemployment rate is just 4.3%, yet higher‑income earners believe there is a 20–25% probability that they will lose their job within the next five years (see Figure 4).

Under normal circumstances, a strong labor market and rising equity prices would support consumer confidence. Instead, fears surrounding technological displacement appear to be weighing heavily on sentiment.

Figure 4. High-Income Earners’ Probability of Job Loss Over the Next 5 Years (%)

Sources: University of Michigan, National Bureau of Economic Research, and Potomac. Data as of January 2026. Note: Shaded regions denote periods of U.S. recession.

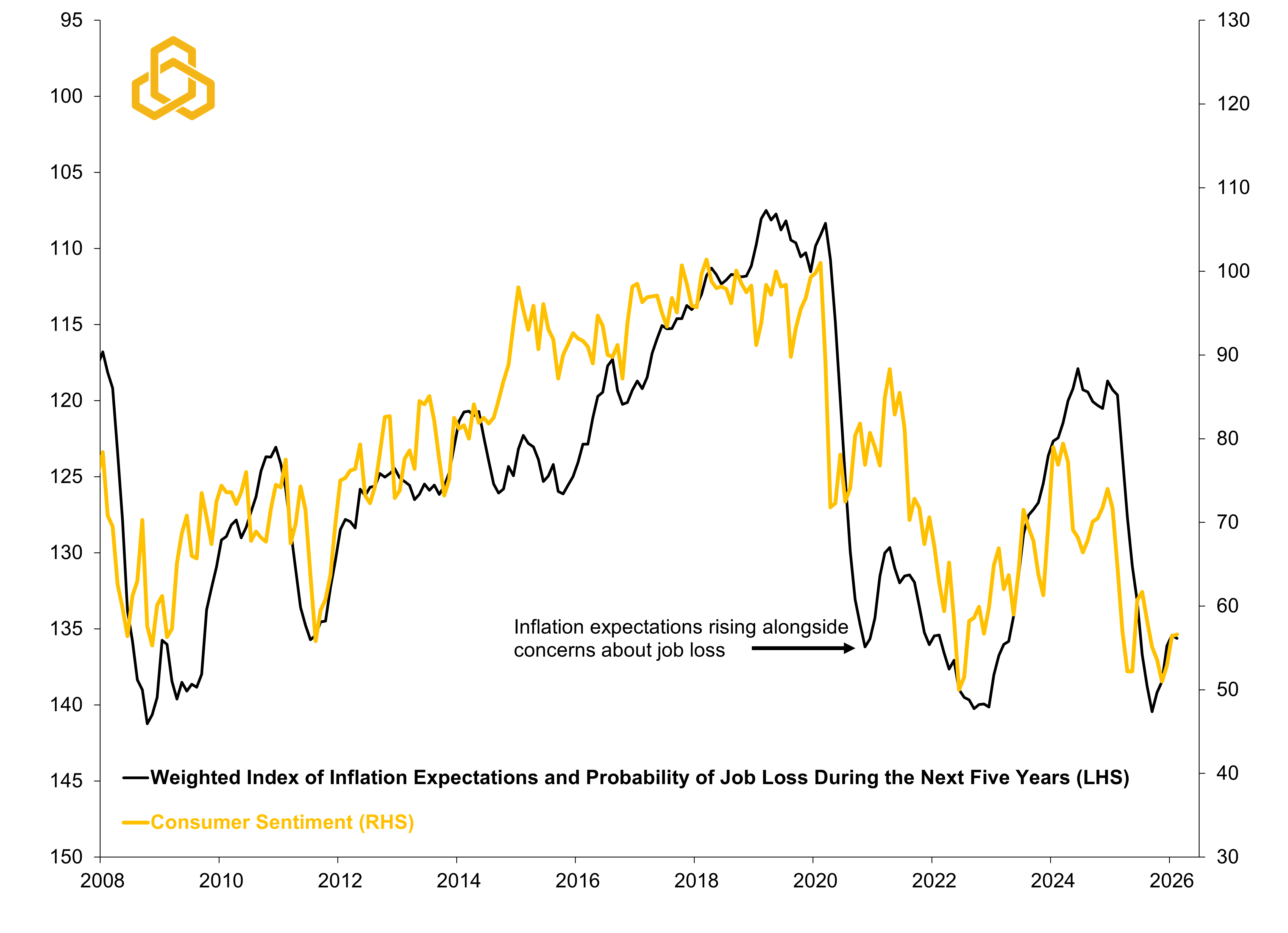

While it is impossible to measure precisely how much artificial intelligence is affecting the official consumer sentiment index, our internal framework suggests that concerns about job security may matter even more than inflation expectations.

Specifically, our weighted index assigns a 60% weight to job‑loss expectations and a 40% weight to inflation expectations. This combined measure tracks consumer sentiment closely, suggesting that the perceived risk of displacement plays an increasing role in shaping household attitudes (see Figure 5).

Figure 5. Weighted Index of Inflation and Job Loss Expectations

Sources: Conference Board, University of Michigan, and Potomac. Data as of January 2026. Note: The Potomac Weighted Consumer Sentiment Index assigns a 40% weight to median inflation rate expectations and a 60% weight to median probability of job loss over the next 5 years. The index is smoothed using a six-month moving average.

A Tortoise and the Hare

Much of the K‑shaped debate has focused on inflation. In many ways, inflation behaves like the tortoise in the classic fable—slow moving, visible, and predictable. Because it evolves gradually, policymakers often have time to respond with affordability measures or targeted relief.

Artificial intelligence, however, resembles the hare. The technology is advancing at breakneck speed, and companies are racing to adopt it to gain a competitive edge.

The potential productivity gains are material, but the transition could carry a meaningful human cost. As firms automate tasks and restructure their workforces, the benefits may accrue quickly to capital owners while labor faces a period of uncertainty and depressed sentiment.

The question is not whether AI will generate economic gains. The real question is whether policymakers will recognize the consequences of those gains quickly enough to manage the risks that accompany the rewards.

PFM-315-20260304