Bear Market in Diversification

Why rising inflation broke traditional diversifiers and why tactical management matters now more than ever.

The U.S. stock market hit a record high on January 27, 2026, as investors prepared for additional Fed rate cuts, fiscal stimulus, and fading inflation. Just two months later investors now see a rate hike almost as likely as a rate cut and are expecting inflation to surge past 3% as the closure of the Strait of Hormuz brings back the specter of rising prices and the S&P 500 approaches a potential 10% correction.

We do not expect another Fed rate hiking cycle or 9% inflation, but market performance in 2022 taught investors an important lesson about diversification. Advisors who worked to maintain globally diversified and risk-balanced portfolios learned an uncomfortable truth. Traditional diversifiers such as bonds, gold, commodities, and managed futures not only lagged equities, but often failed during the exact periods when clients needed protection.

When Traditional Diversifiers Fail

Market history shows that clients rarely abandon a strategy due to missed upside. They abandon it because of fear. Deep and extended drawdowns overwhelm even the most disciplined investors.

Advisors have long relied on diversifiers to soften that emotional burden. Recent cycles revealed the fragility of that assumption. Correlations shifted, performance became inconsistent, and many diversifiers failed to provide support when volatility surged

Many of these diversifiers also carried high volatility and significant maximum drawdowns, which made them difficult for clients to stay invested in over full market cycles.

Why Diversification Failed

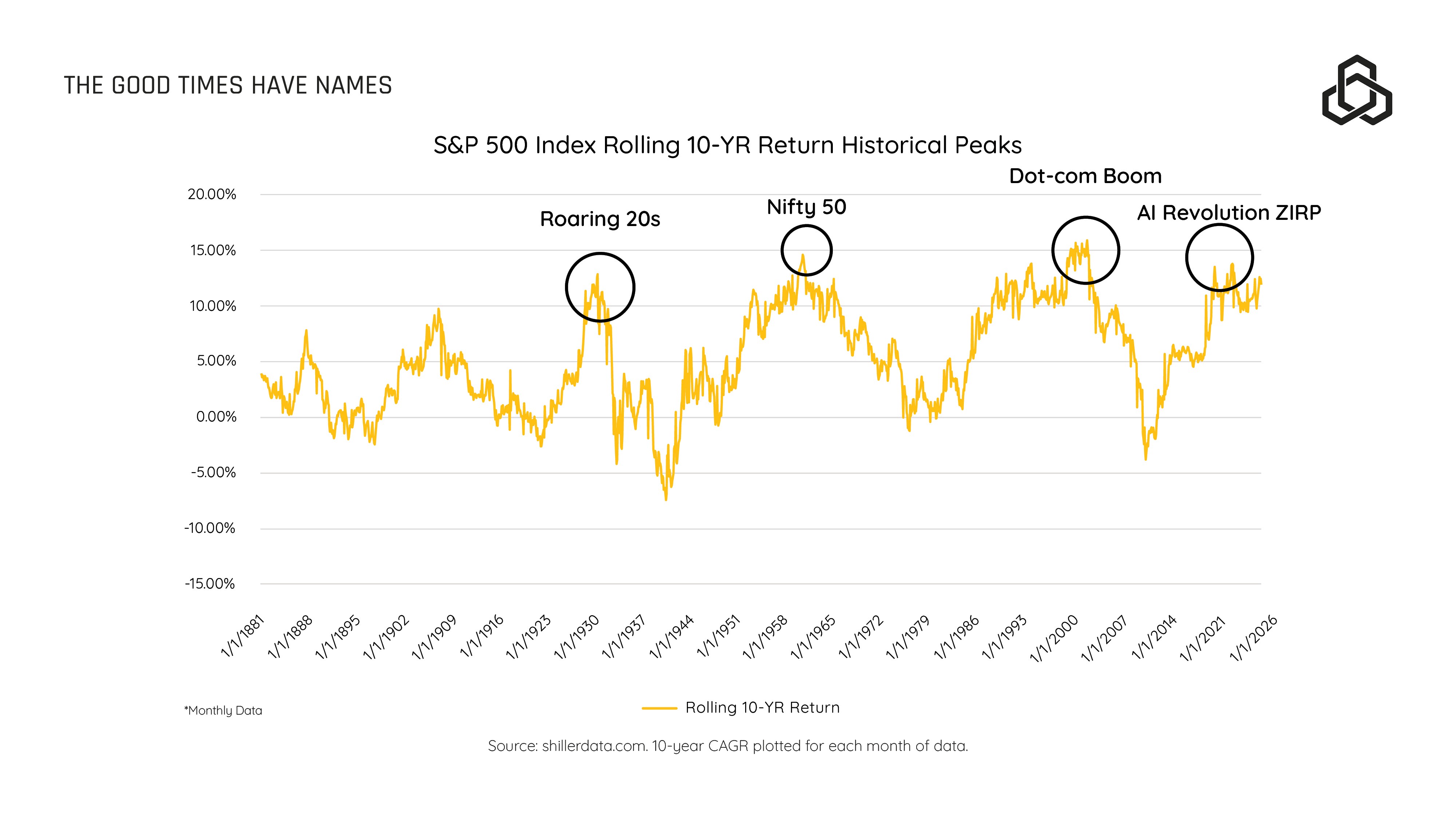

Rolling returns reached historical extremes

Rolling ten-year S&P 500 returns going back to 1881 have historically cycled between high and low ranges. After extreme readings, they typically reverted. Prior periods of unusually strong returns earned memorable labels such as the Roaring Twenties, the Nifty Fifty, and the Dot-com Boom.

We are once again at an extreme. History shows that diversified investors significantly underperformed during similar cycles. Many eventually abandoned diversifiers because they felt pressure to chase equity returns.

Traditional diversifiers broke down at the same time

For decades, advisors relied on the mix of stocks and bonds. Falling interest rates supported bond prices and kept correlations negative until 2022. That year served as a wake-up call as stocks and bonds declined together.

Other common diversifiers also struggled:

Bonds failed during the period when they were most expected to help.

Gold, commodities, managed futures showed high volatility and experienced deep drawdowns.

Global equities failed to keep pace with U.S. large-caps.

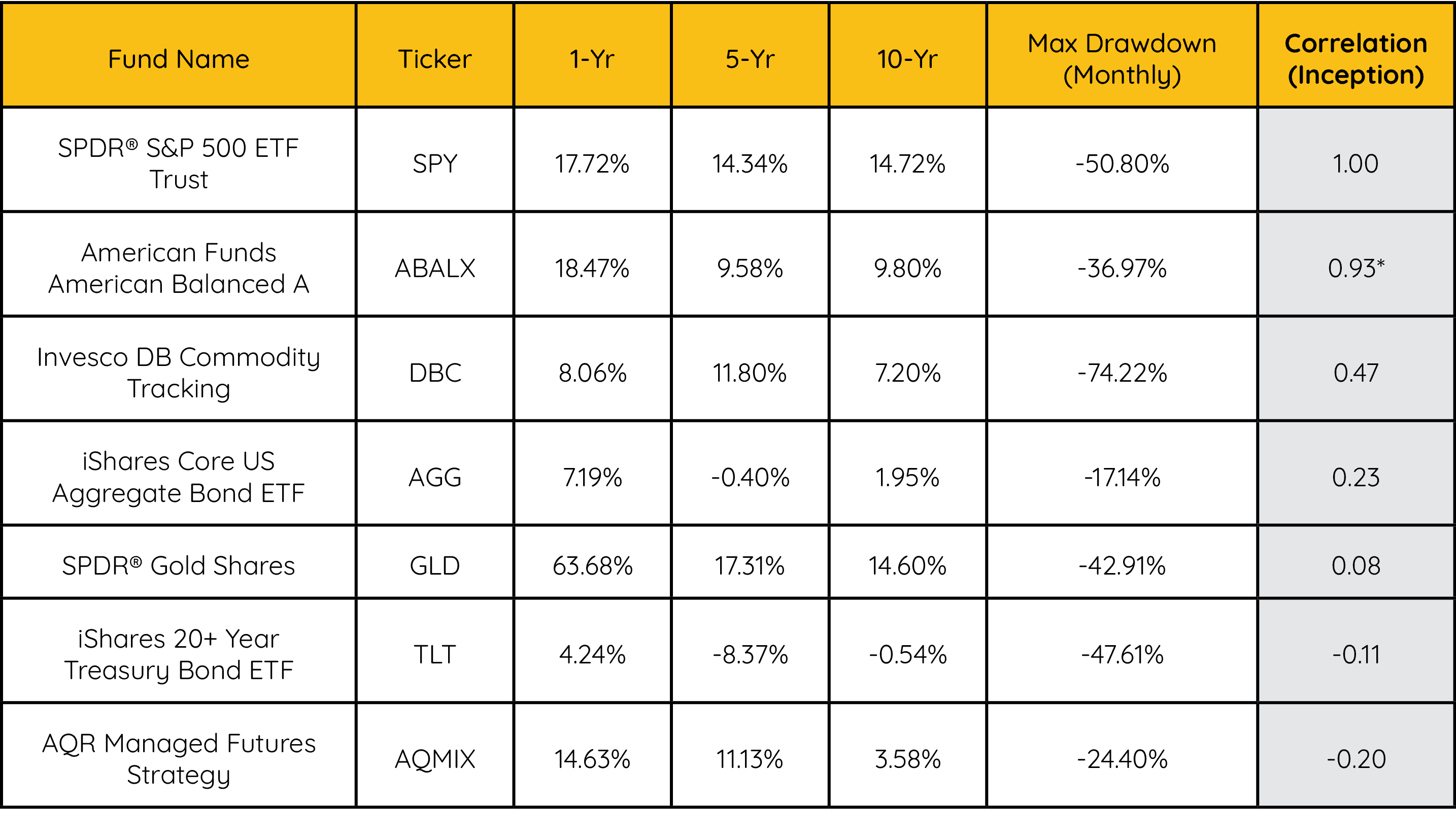

Meanwhile, the cheap, passive SPDR S&P 500 ETF Trust (SPY) compounded at roughly 14.72% per year over the past 10 years, which has made the gap between equities and diversifiers even more difficult for investors to accept.

There has been a major tradeoff. Assets that offer “return” tend to have higher drawdowns (Gold) and/or higher correlations (American Funds) to the S&P 500. Assets that offer lower correlation and/or drawdown usually come with lower returns. See the table below.

Source: FastTrack as of 12/31/2025. *Dataset inception: 9/1/1988

Moving Beyond Traditional Diversification

Traditional diversification depends heavily on correlations remaining stable. However, correlations shift over time. A quick look at the rolling one-year correlation between stocks and bonds shows that the relationship changes over time with inflation often serving as a catalyst for positive correlation and loss of traditional portfolio diversification.

Source: Optuma

Tactical risk management uses a different approach.

It does not attempt to predict market tops or bottoms.

It reduces exposure when risk builds and increases exposure when conditions improve.

It seeks to create a smoother investment experience that clients can follow over time.

Reducing deep drawdowns makes long-term compounding more realistic and client behavior more stable.

Tactical as a Diversifier

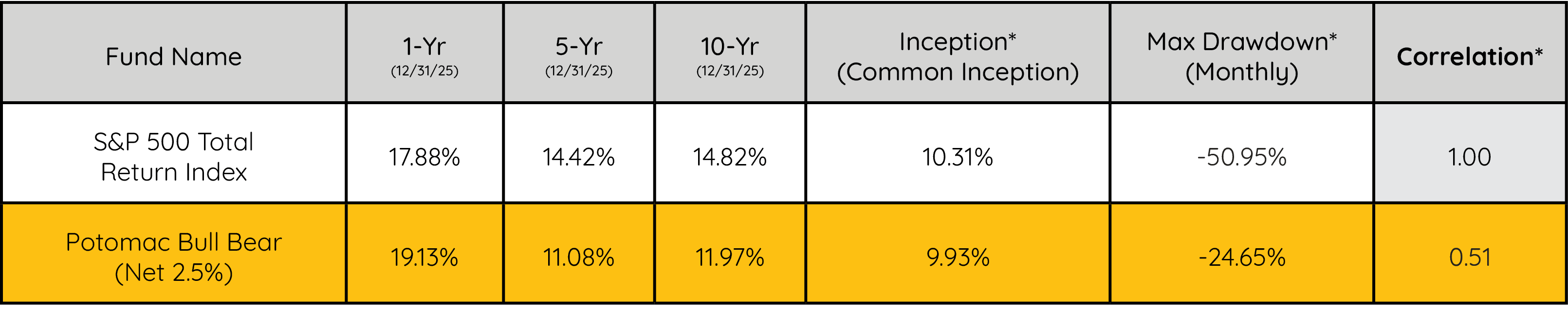

Potomac’s Bull Bear strategy aims to offer competitive long-term returns, lower correlation to the S&P 500, and controlled drawdowns. These qualities are essential for any investment seeking to serve as a true diversifier.

*Calculated since common inception (6/1/2002). Source: FastTrack

As the table above shows, Bull Bear demonstrates:

Competitive one-year, five-year, and ten-year returns.

Maximum drawdown that is meaningfully lower than the S&P 500.

Correlation low enough to function as a genuine diversifier rather than a diluted equity position.

Potomac strategies rely on quantitatively tested systems to manage risk, not on hope that an asset becomes negatively correlated during a bear market.

Why This Matters for Advisors

Investors do not fire advisors because bonds underperformed or commodities were volatile. They fire advisors because they experience drawdowns they cannot emotionally tolerate.

A long bull market hid the structural weaknesses of traditional diversifiers. When correlations broke and volatility rose, traditional approaches proved insufficient.

Advisors now need tools that can:

Manage risk intentionally rather than passively

Provide rules-based downside protection

Offer a return path that keeps clients invested

Build a behavioral advantage during market stress

Tactical strategies can help achieve these goals.

Final Thoughts

The bear market in diversification is not theoretical. It appears in performance data, in client conversations, and in the stress advisors face when correlations fail, and traditional diversifiers break down.

Diversification is still important. However, traditional diversification alone is no longer enough.

In a market environment defined by volatility, correlation breakdowns, and emotional decision-making, tactical risk management offers a modern solution to an old challenge. It helps advisors keep clients disciplined, engaged, and aligned with long-term objectives.