Small businesses are the backbone of the U.S. economy. They comprise 99.9% of all firms and employ 46% of private sector workers, so what they say matters. Fortunately, the National Federation of Independent Business (NFIB) does an excellent job of surveying them. In this Beltway Brief, we break down what small businesses are saying and the potential implications for the U.S. economy and investors.

In the latest Survey of Small and Independent Business, optimism remained on the weaker side with the Small Business Optimism Index slipping to 95.3 in May. This is modestly below its 52-year average of 98.0. Of the ten components in the index, three increased, six decreased, and one was unchanged.

For investors, we found the two most interesting takeaways to be the following:

70% of small business owners reported supply chain disruptions were affecting their businesses

The net share of owners planning to raise prices has jumped 10 percentage points since March to 34%.

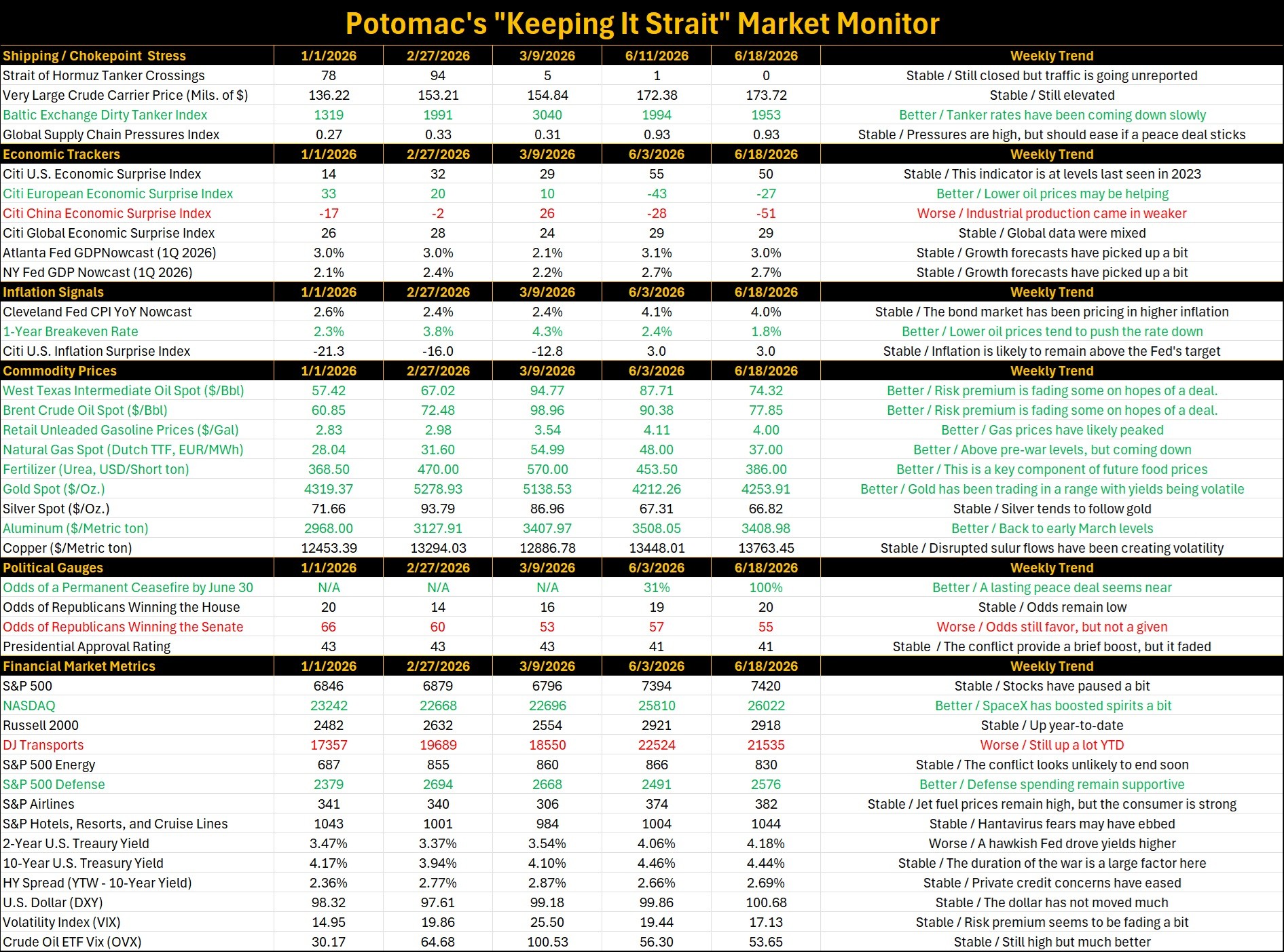

Both developments appear to reflect the impact of the prolonged closure of the Strait of Hormuz (see Figure 1).

Figure 1. Global Supply Chain Pressures Index (Std. Deviations)

Sources: Federal Reserve Bank of New York, Bloomberg L.P., and Potomac. Data as of May 31, 2026.

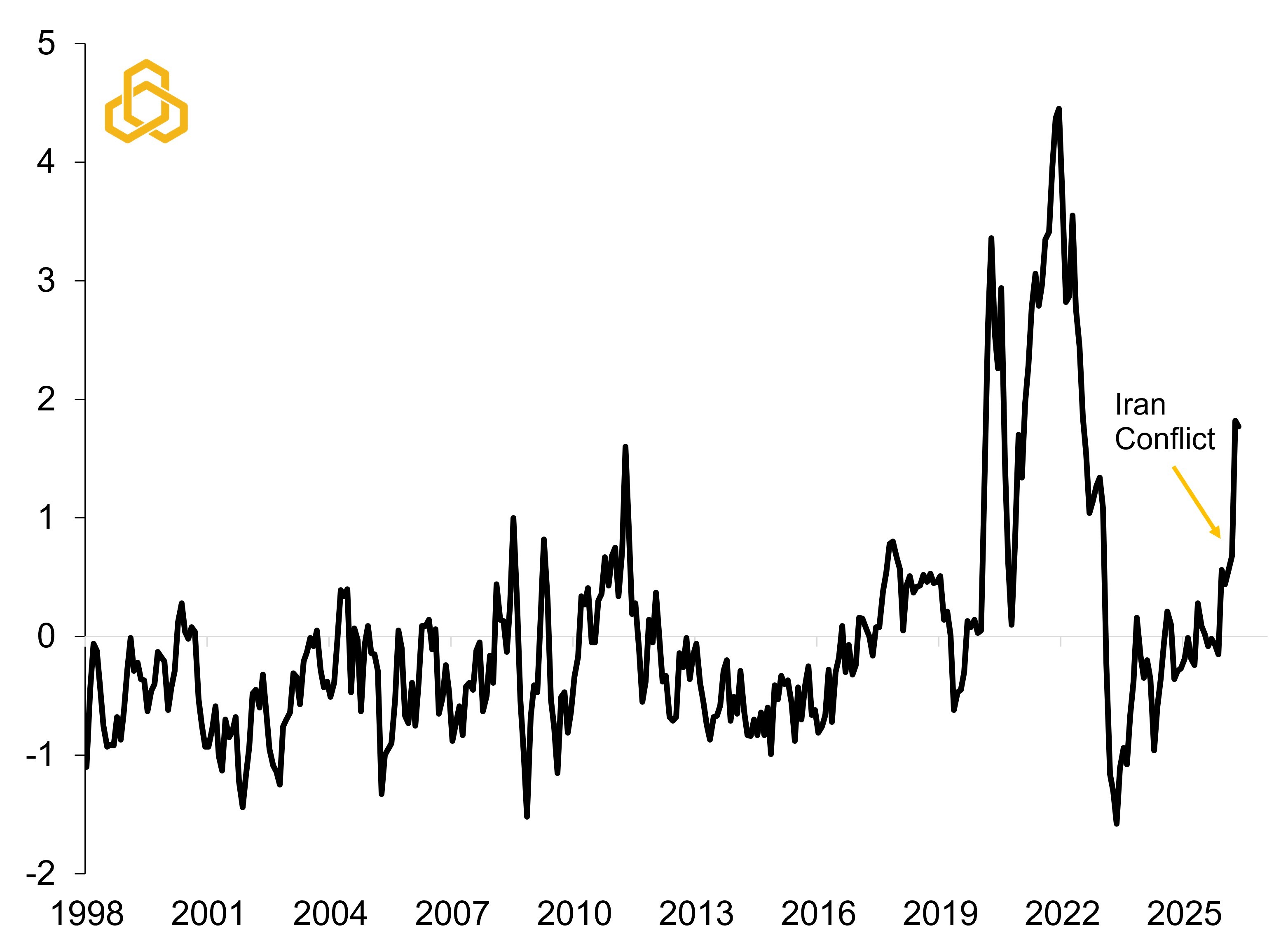

This tells us something about inflation with small business pricing plans typically leading core inflation by about two months. While May's core inflation print was a bit tamer than expected, small businesses are suggesting that we may still see a gradual drift higher over the next quarter or two (see figure 2). If higher energy prices are going to bleed into core inflation, this may be one of the earliest warning signs. A sustained uptick in core inflation would reinforce the bond market's expectations for additional tightening, with investors currently pricing the next rate hike in December 2026. In the latest Federal Open Market Committee Summary of Economic Projections, nine out of 19 official policymakers envisioned one rate hike by the end of this year.

Figure 2. NFIB Plans to Lift Prices in the Next 3-Months vs. Core Inflation

Sources: National Federation of Independent Business, Bureau of Economic Analysis, Bloomberg L.P., and Potomac. Data as of May 31, 2026. Note: “Inflation” is the personal consumption expenditure price deflator excluding food and energy prices.

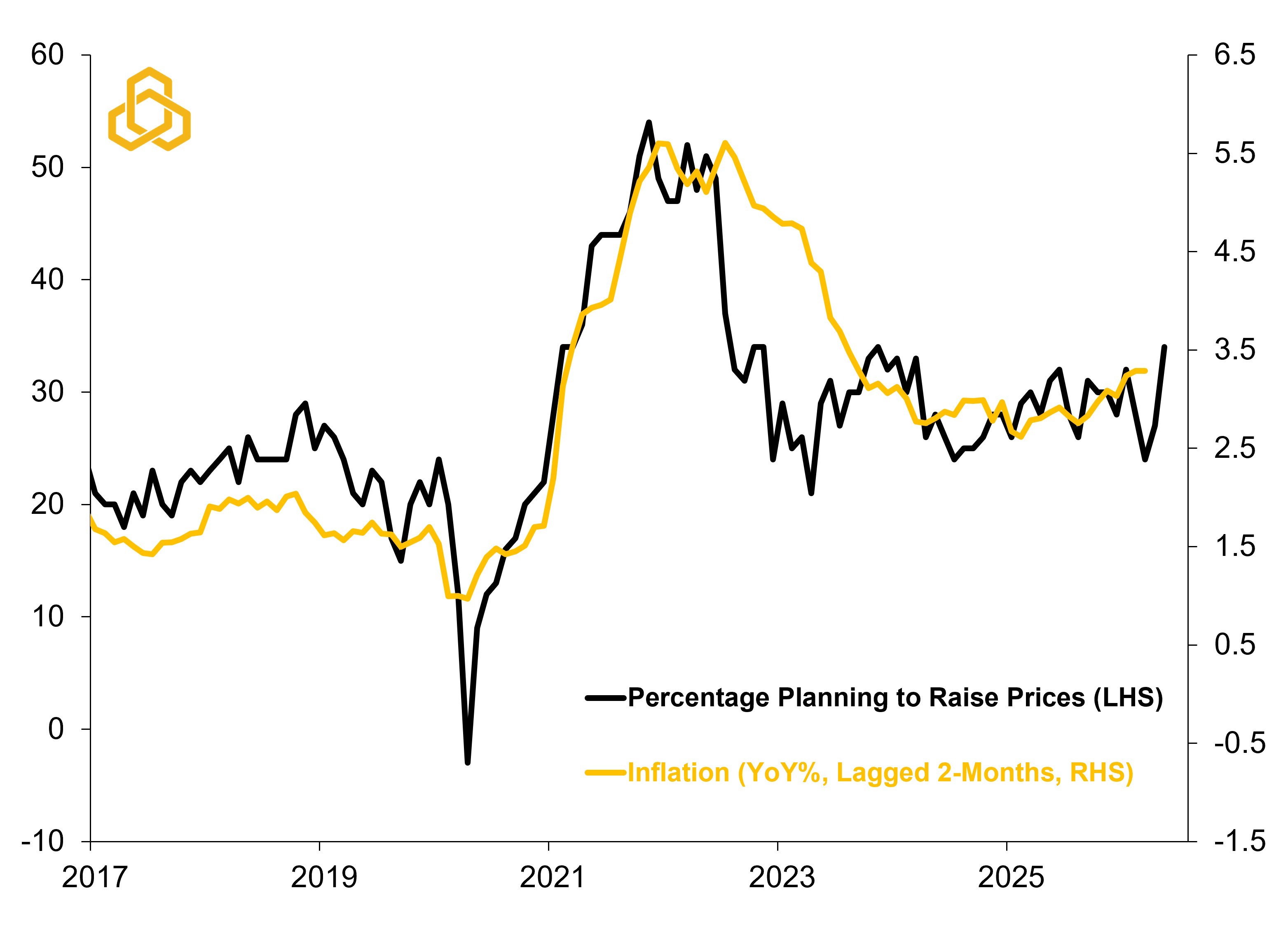

Much of this will depend on the longevity of the ongoing Iran conflict. If the U.S. and Iran have indeed reached a peace deal that reopens the Strait of Hormuz quickly, investors could see a further decline in the risk premium embedded in crude oil prices, providing some relief for small business pricing plans (see Figure 3).

Figure 3. NFIB Plans to Lift Prices vs. the Price of Crude Oil

Sources: National Federation of Independent Business, Department of Energy, Bloomberg L.P., and Potomac. Data as of May 31, 2026 for NFIB and June 16, 2026 for West Texas Intermediate crude oil price.

If that is the case, then perhaps headline inflation may be at or near a peak even if core inflation continues to rise gradually in coming months. This seems the most likely path, but there is still a lingering risk that the conflict renews at a time when there is even less insurance against global oil supply shocks (see Figure 4).

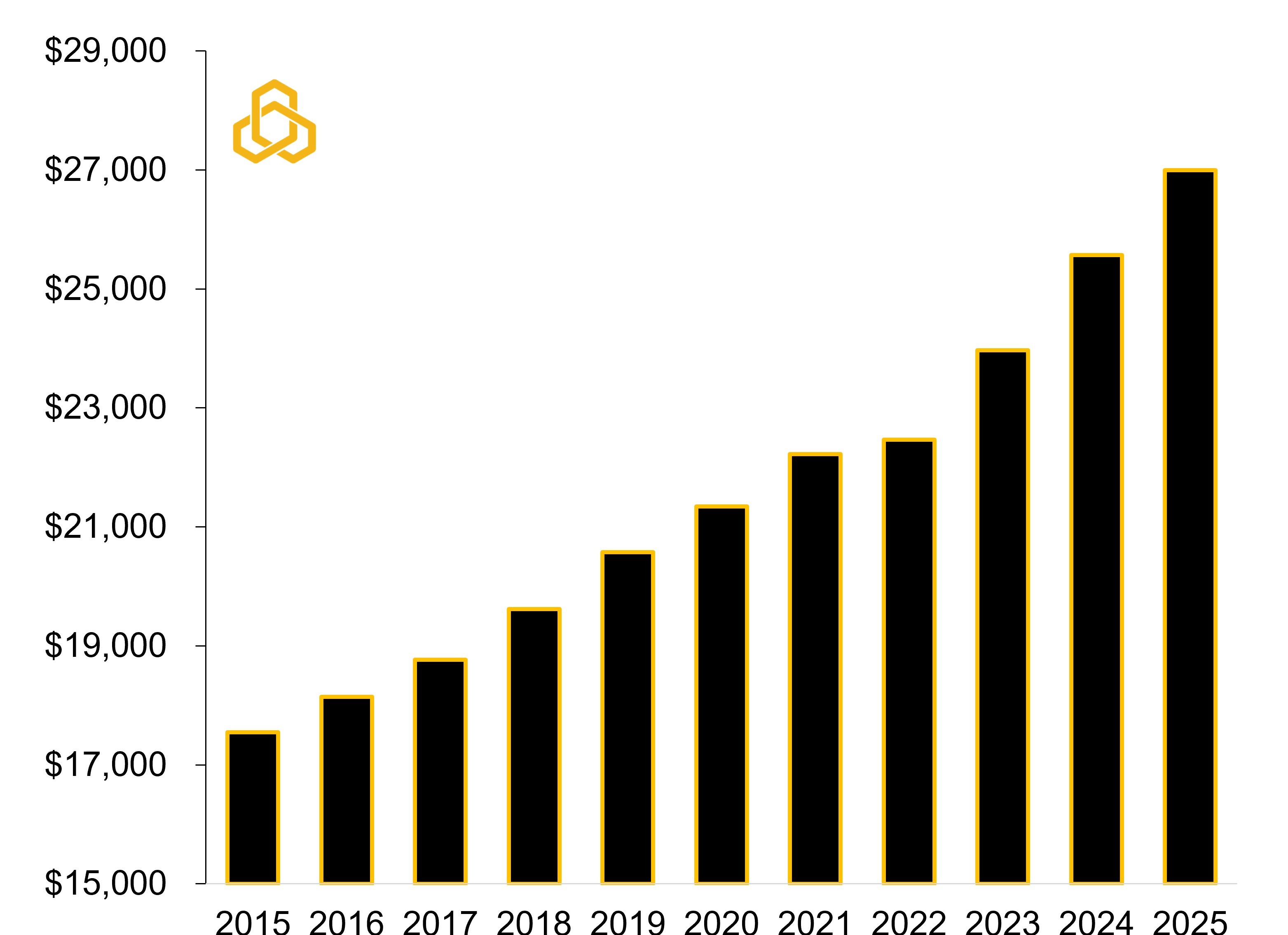

Figure 4. U.S. Strategic Petroleum Reserves (Millions of Barrels)

Sources: Department of Energy, Bloomberg L.P., and Potomac. Data as of June 5, 2026.

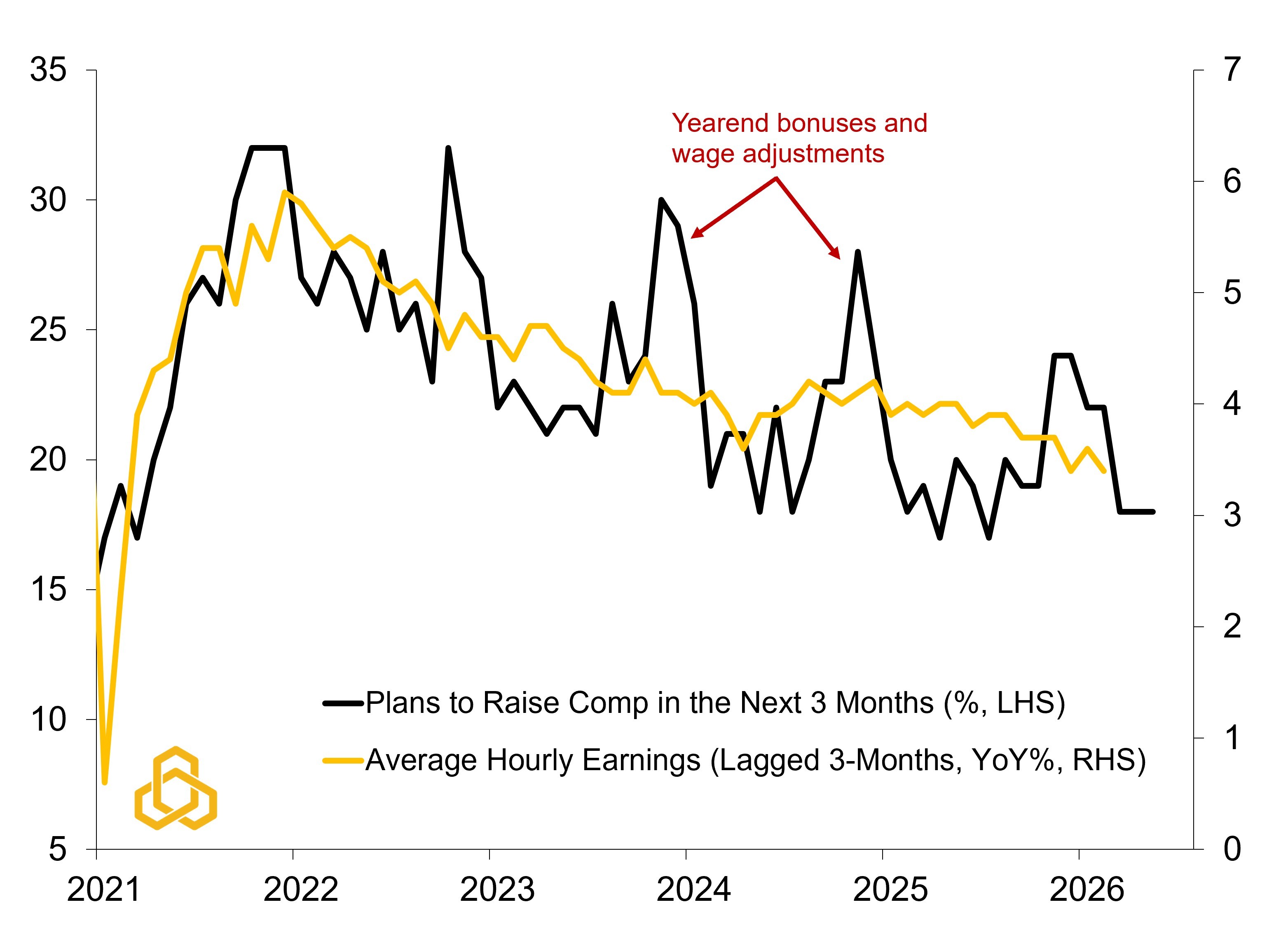

Assuming the U.S.-Iran peace deal holds, this could take some heat off the Federal Reserve to raise interest rates, but it may also depend on shifting labor market dynamics. As we wrote in The State of the Other Mandate: What the Labor Market Is Telling Us, the U.S. labor market has been showing signs of improvement. However, it has not yet shown material signs of wage gains. This aligns with small business compensation plans, with the percentage planning to raise wages continuing to trend lower following the pandemic (see figure 5).

Figure 5. NFIB Plans to Raise Wages vs. Average Hourly Earnings

Sources: National Federation of Independent Business, Bureau of Labor Statistics, Bloomberg L.P., and Potomac. Data as of May 2026.

We did find it notable; however, that the percentage of small companies reporting the cost of labor as their top problem hit an all-time high in the latest survey. This series does not always track well with wage gains however, and we suspect it may have more to do with the rising cost of providing workers with health insurance (see figure 6).

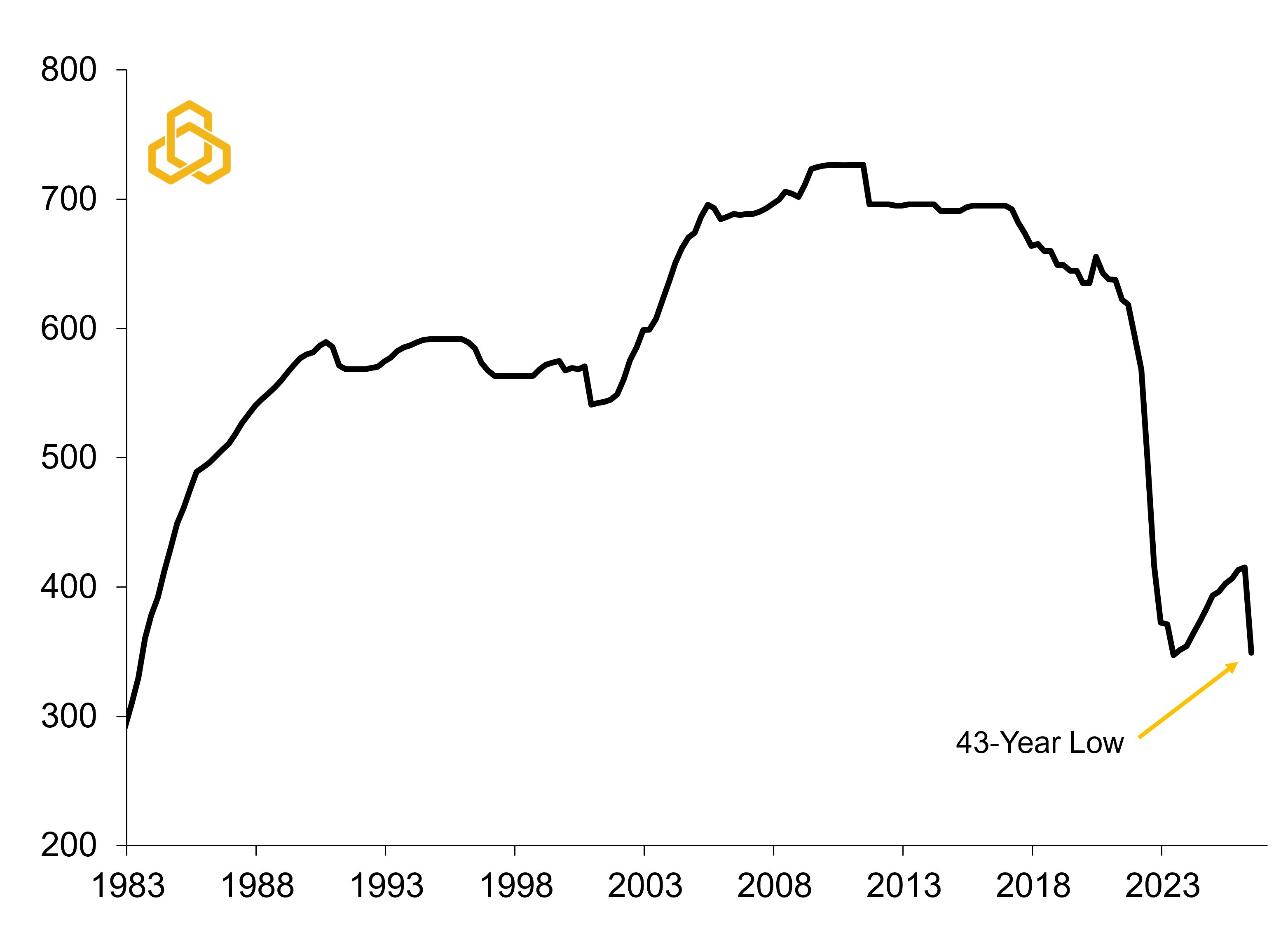

Figure 6. Annual Premium for Employer-Sponsored Family Health Coverage

Sources: Department of Energy, Bloomberg L.P., and Potomac. Data as of June 5, 2026.

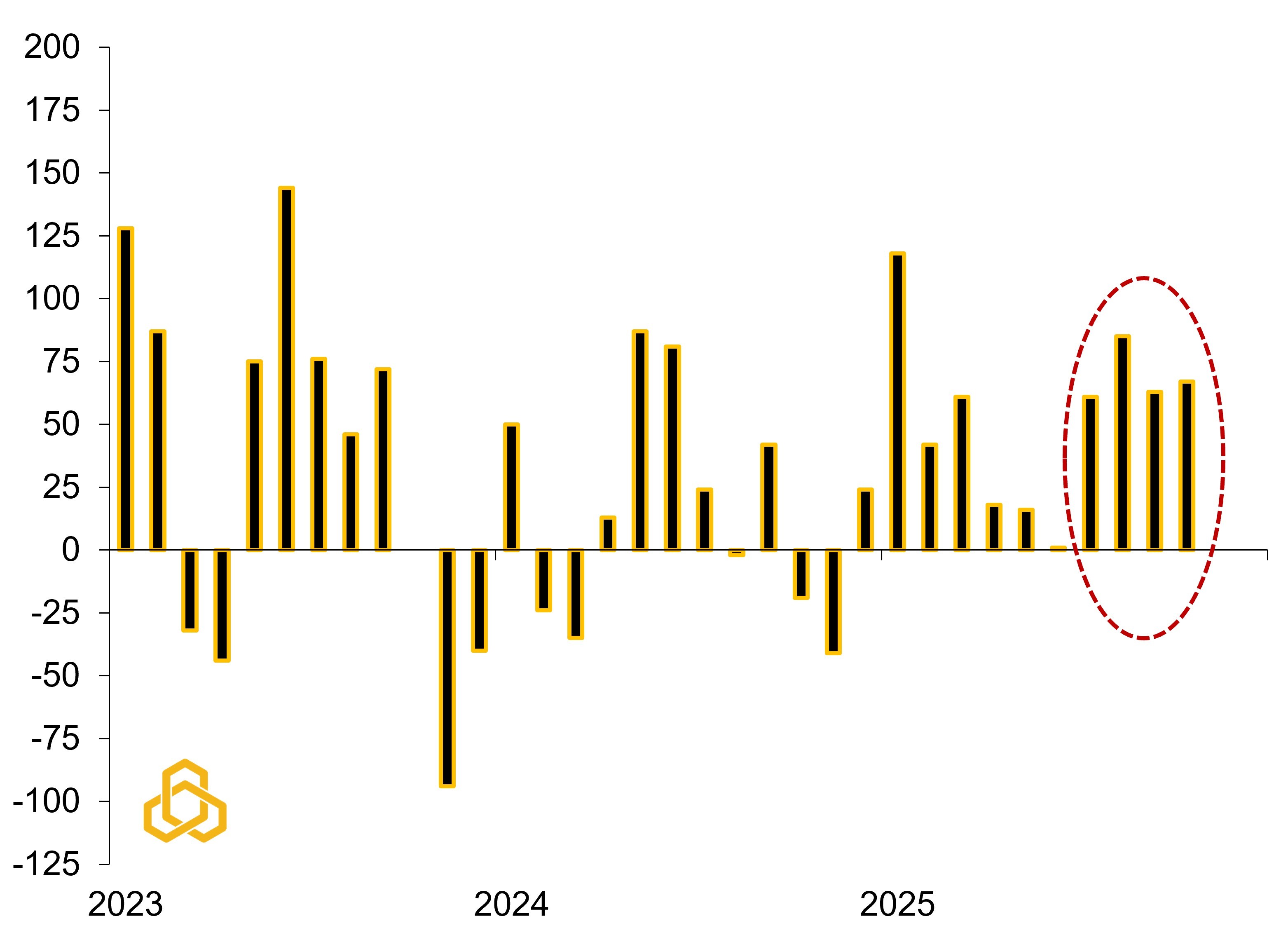

The other datapoint we took note of was that just 9% of small businesses said they intend to hire over the next three months. This is down 13 percentage points from April and marks the lowest reading since May 2020. That sentiment has not yet been reflected in the hard data, with ADP reporting that small business hiring has remained solid year-to-date (see Figure 7). While the survey results do not currently align with many of the economic indicators that have been surprising to the upside, it may still be worth monitoring in the months ahead.

Figure 7. Monthly Change in ADP Private Nonfarm Small Business Jobs (Thous.)

Sources: ADP, Bloomberg L.P., and Potomac. Data as of May 2026.

Taken together, the latest NFIB survey paints a picture of an economy that remains resilient but increasingly complicated. Small businesses are reporting rising pricing pressures tied to supply chain disruptions and higher energy costs, while at the same time becoming more cautious about hiring and compensation plans.

For investors, the most important takeaway may be that inflation risks have not disappeared. Small business pricing plans have historically been a useful leading indicator of core inflation, and recent survey results suggest inflation could drift modestly higher over the coming quarters even if headline inflation begins to ease.

The good news is that much of this outlook still hinges on developments in the Middle East. A lasting U.S.-Iran peace agreement and the reopening of the Strait of Hormuz could reduce energy prices, ease supply chain pressures, and alleviate some of the inflation concerns emerging in the survey data.

For now, small businesses appear to be sending a clear message: growth remains intact, but inflation pressures are proving more persistent than many investors had hoped.

Weekly “Keeping it Strait” Highlights:

The Strait of Hormuz remains closed. However, there are numerous reports that there has been tanker traffic with government-owned ships making it through. According to Rapidan Energy Group, about 2 million barrels a day of oil and related products are flowing out of the Gulf. This may be keeping oil prices in check despite renewed tensions.

Another week of more green than red on the tracker. The primary change has been that U.S. growth trackers have seen an uptick with U.S. economic data surprising to the upside, including a solid jobs report that showed 172,000 jobs being added in May.

The downside to stronger growth is decreased odds of additional rate cuts from the Federal Reserve. While it fluctuates daily, the market is still looking for at least one rate hike by January 2027.