The Federal Reserve has two mandates assigned by Congress: price stability and maximum employment. With the war in Iran ongoing, investors remain squarely focused on the inflation side of the mandate, but what is the current state of the other mandate?

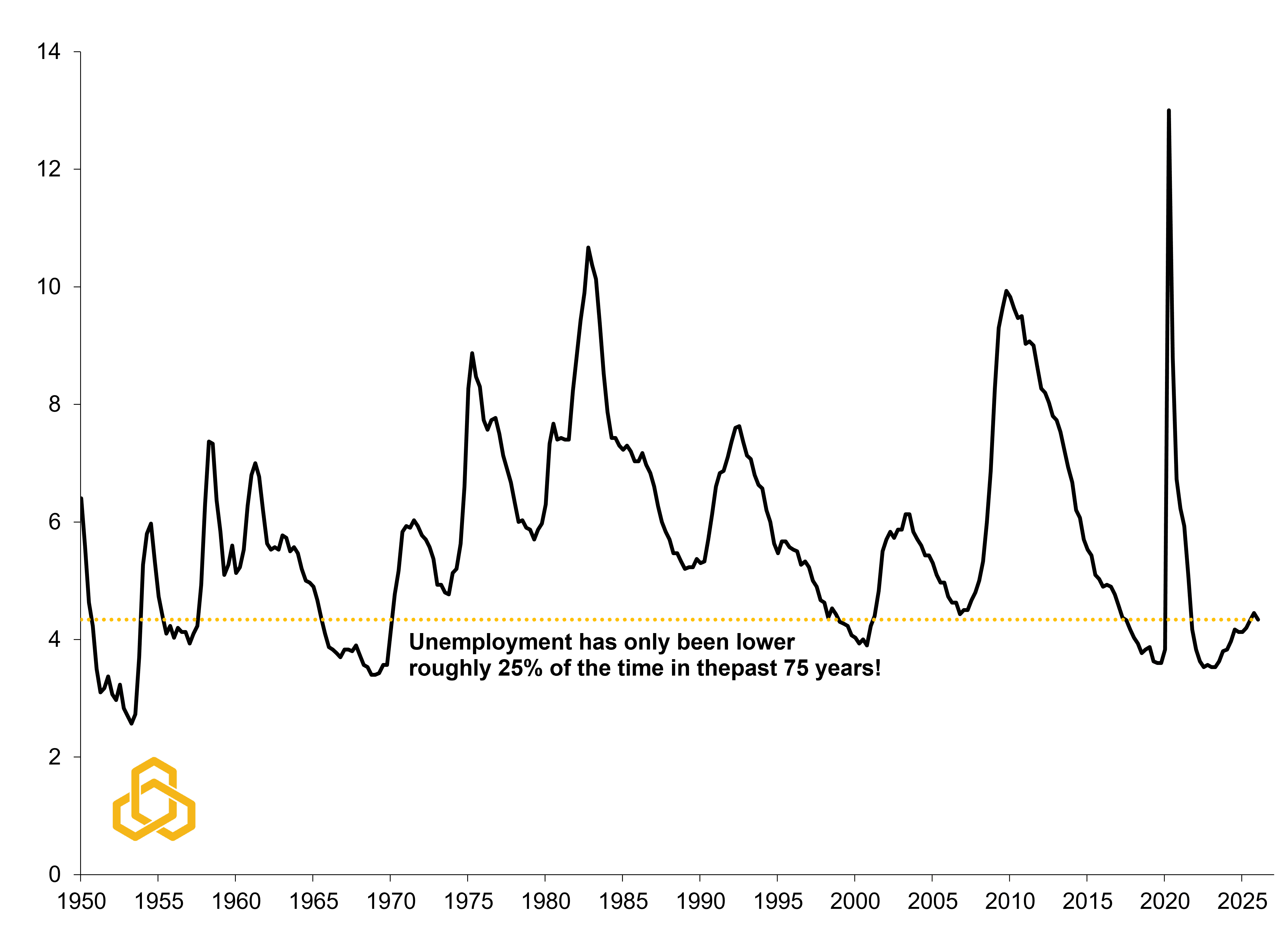

One could easily argue that the labor market remains in good shape with the unemployment rate at 4.3%, and they would be right. Since 1950, it has only been lower about 25% of the time (see figure 1).

Figure 1. U.S. Unemployment Rate (%)

Sources: Bureau of Labor Statistics, Bloomberg L.P., and Potomac. Data as of April 2026

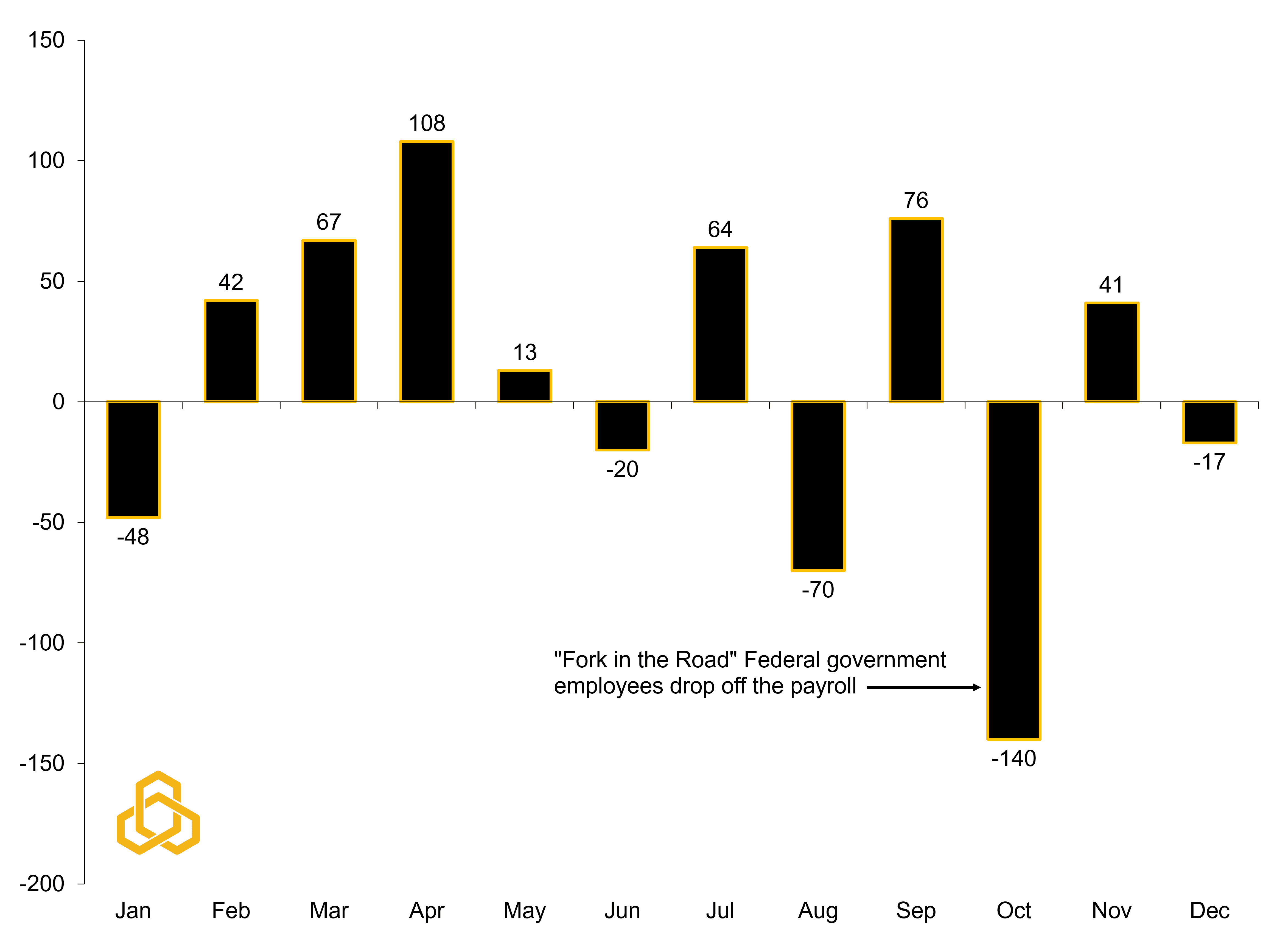

Viewed through this lens, the Fed should feel comfortable shifting its attention to the inflation side of the mandate for the time being. However, low unemployment does not necessarily imply a strong labor market. In fact, the jobs market was far from strong last year, adding just 116,000 jobs in total (see figure 2).

Figure 2. Total U.S. Nonfarm Employment Growth in 2025 (Thous.)

Sources: Bureau of Labor Statistics, Bloomberg L.P., and Potomac. Data as of December 2025.

It is important to note that Federal government employment accounted for a meaningful share of last year's weakness with 330,000 jobs lost due to the Department of Government Efficiency (or DOGE) efforts. However, even excluding those losses, private-sector payroll growth averaged just 24,667 jobs per month in 2025. This compares to an average of roughly 149,000 jobs in 2023 and 85,000 jobs in 2024.

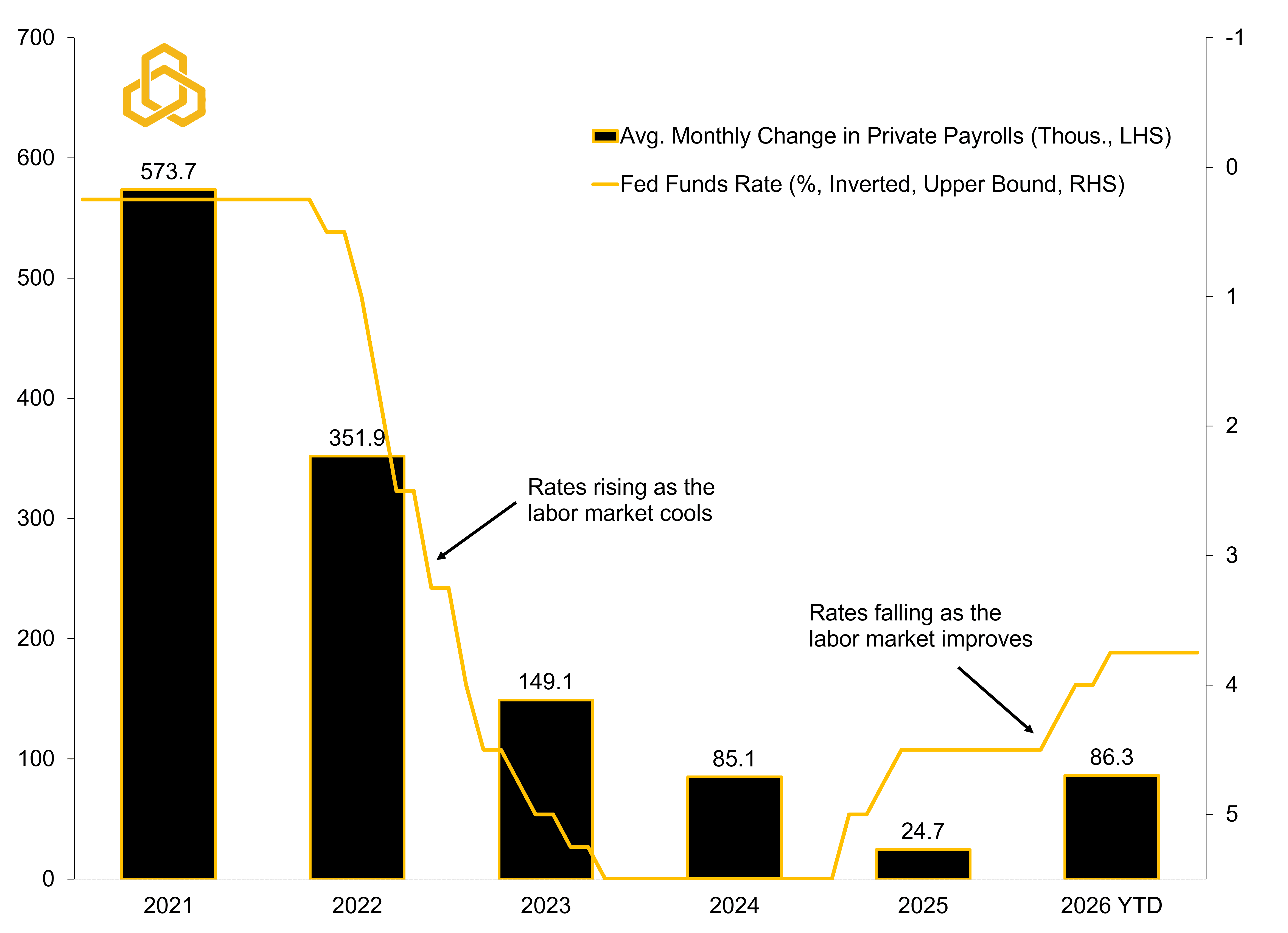

While some may argue that the Fed's monetary policy has not been overly restrictive, the persistent cooling in payroll growth suggests at least some impact. On the upside, private sector job growth appears to be experiencing an uptrend year-to-date with the average improving to about 86,000 jobs per month (see figure 3).

Figure 3. Fed Funds Rate Vs. Avg. Monthly Change in Private Nonfarm Payrolls

Sources: Bureau of Labor Statistics, Bloomberg L.P., and Potomac. Data as of December 2025.

Even so, the improvement has been relatively narrow with Healthcare and Social Assistance jobs accounting for about 64% of all private sector jobs added year-to-date. In fact, job breadth over the past year has been the worst the U.S. economy has ever seen outside of recessions on records dating back to 1991. While headline payroll growth has stayed largely positive, this narrow breadth helps explain why many workers view the labor market less favorably than the unemployment rate alone would suggest.

Fortunately, there are some signs that portions of the labor market may be stabilizing.

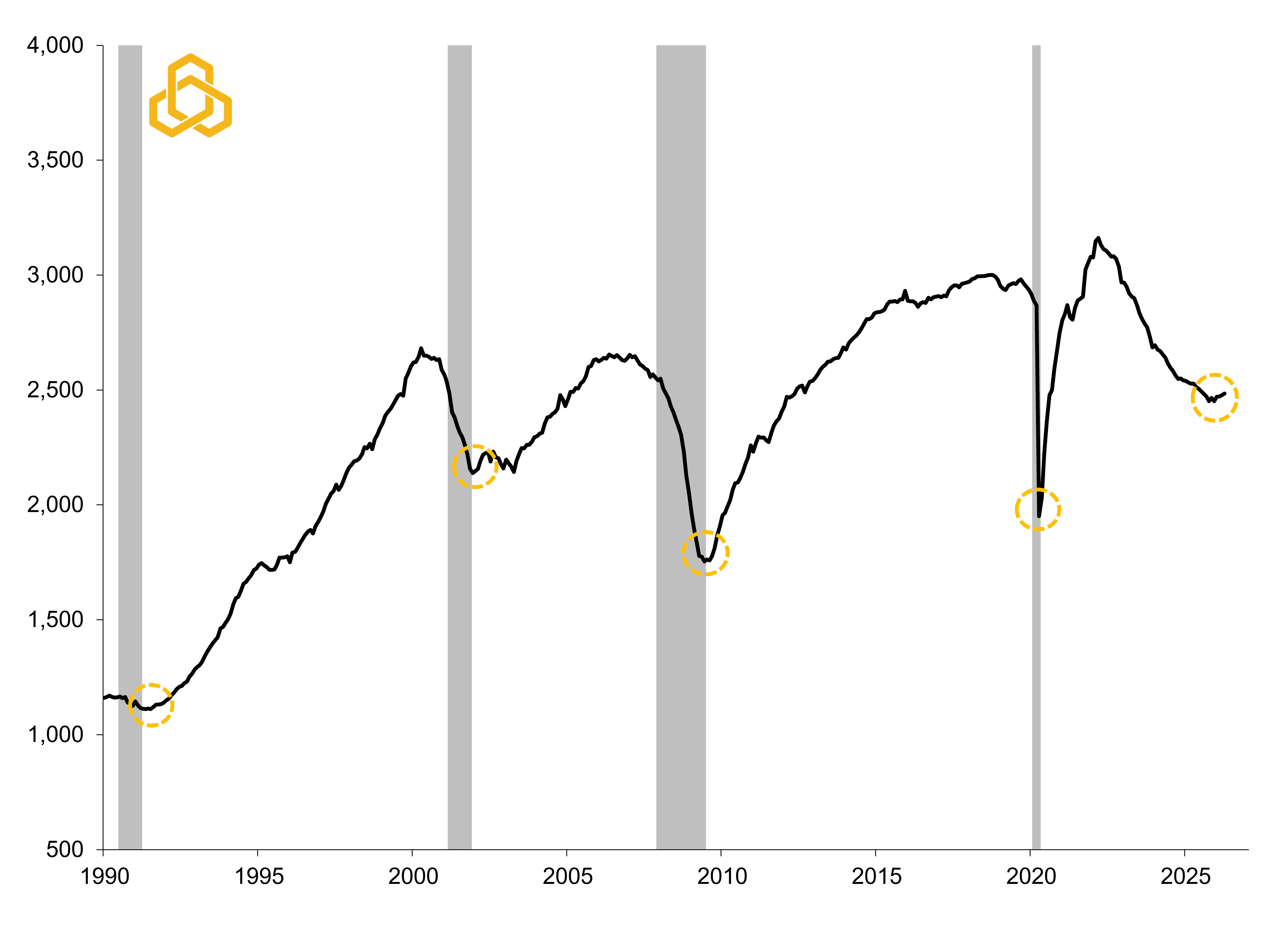

For example, temporary employment has shown growth for four consecutive months now. The last time this occurred was in 2021 when massive fiscal stimulus was working its way through the system. This sector is often viewed as a leading economic indicator because companies tend to hire temporary workers first when demand improves, placing the category at the front end of the hiring cycle (see figure 4).

Figure 4. Temporary Employment (Thous.) vs. Periods of U.S. Recession

Sources: Bureau of Labor Statistics, Bloomberg L.P., and Potomac. Data as of April 2026. Note: Shaded regions denote periods of U.S. recession.

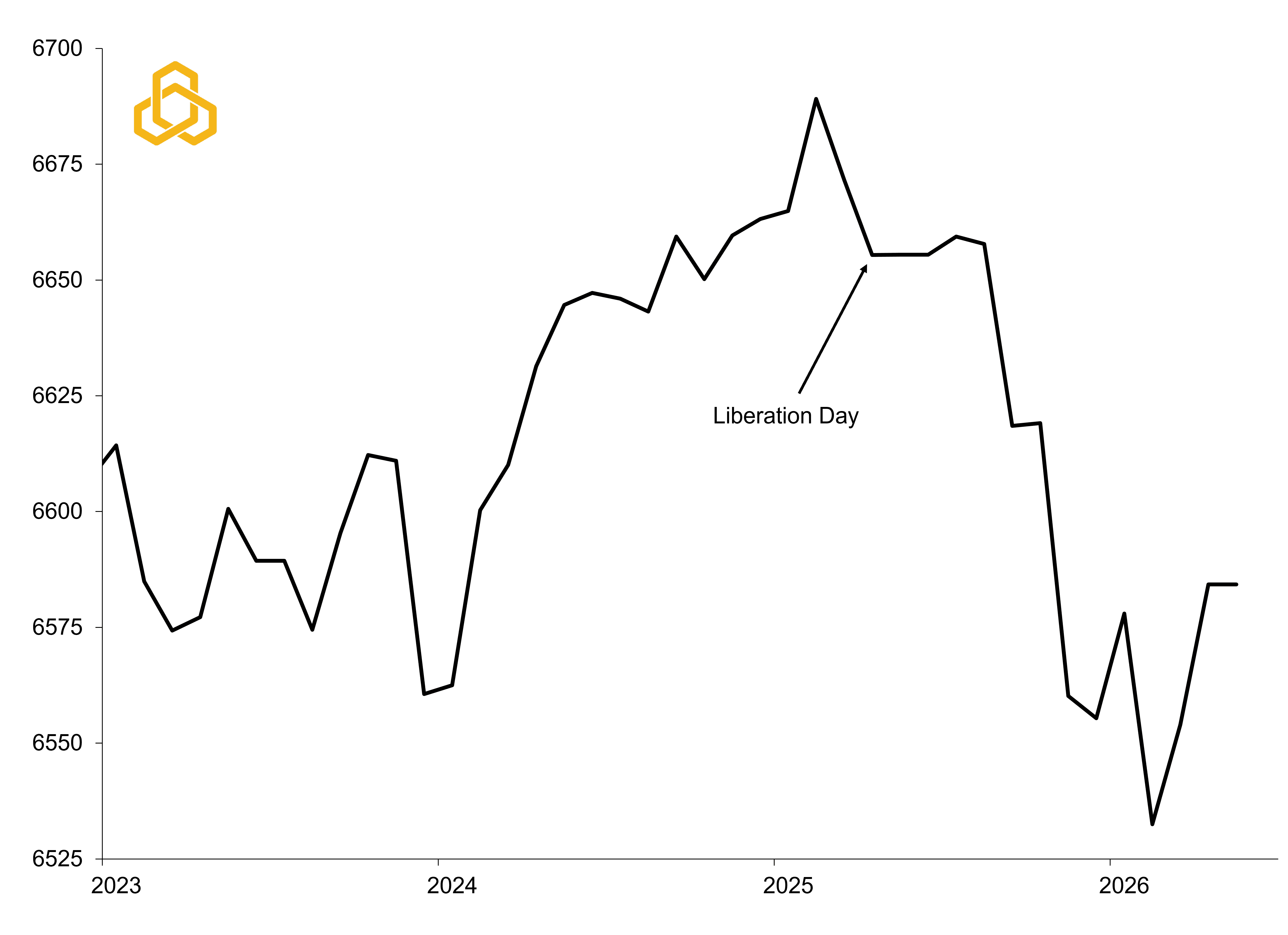

Similarly, transportation and warehousing employment appears to be stabilizing after shedding roughly 108,000 jobs in 2025 as tariffs slowed the demand for goods. Since the start of the year, this sector has added roughly 29,000 jobs and has grown in three of the last four months. While not contributing much to the headline, it is no longer subtracting as portions of the economy appear to be recovering from the spike in trade tensions (see figure 5). This improvement has also been reflected in the Dow Transports, which have rallied 35% since November 2025.

Figure 5. Total Transportation and Warehousing Employment (Thous.)

Sources: Bureau of Labor Statistics, Bloomberg L.P., and Potomac. Data as of April 2026.

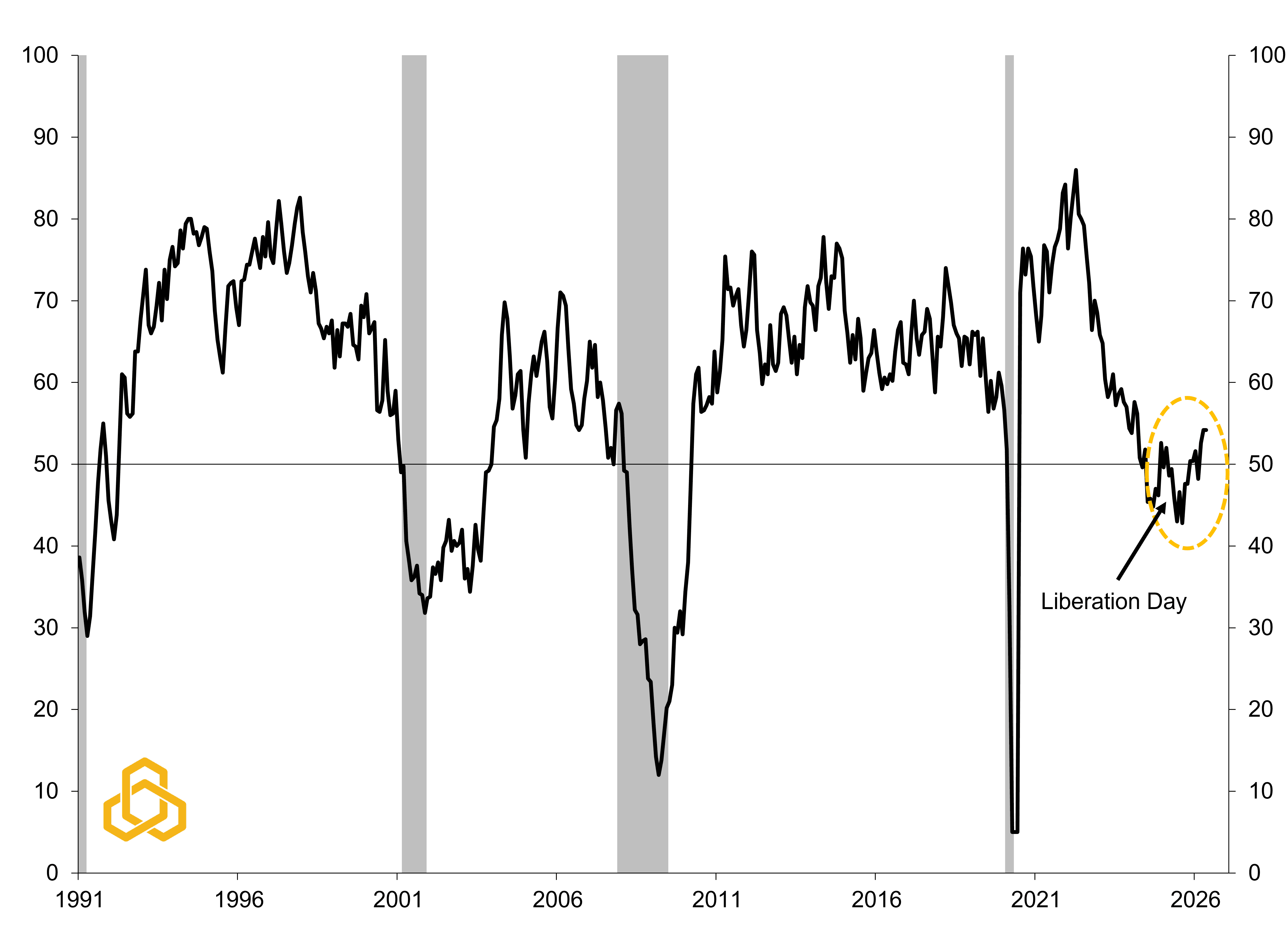

For the time being, this trend looks to be intact with the Institute for Supply Management's new orders component climbing further in May – rising from 54.1 to 56.8. If this strength in manufacturing activity persists alongside the Artificial Intelligence buildout, this should provide continued support for these nascent recoveries in the labor market. Combined, these trends have helped lift the employment diffusion index, a measure of job breadth, back above 50 in four of the last five months (see figure 6).[1]

[1] Diffusion indexes of state and metropolitan area employment changes : Monthly Labor Review : U.S. Bureau of Labor Statistics

Figure 6. U.S. Employment Diffusion Index of Nonfarm Payrolls (3-Months)

Sources: Bureau of Labor Statistics, Bloomberg L.P., and Potomac. Data as of April 2026.

Now, the downside. With inflationary pressures building, this welcome increase in job market breadth may reduce the urgency for additional rate cuts from the Federal Reserve and it is possible that these improvements will keep the prospect of a Fed rate hike (or dare we say hikes) on the table for longer than markets currently expect. Please see our Warsh and Peace piece for additional insights.

The labor market may be taking a back seat for now, but the Fed's other mandate has a habit of finding its way back into the picture when investors least expect it.

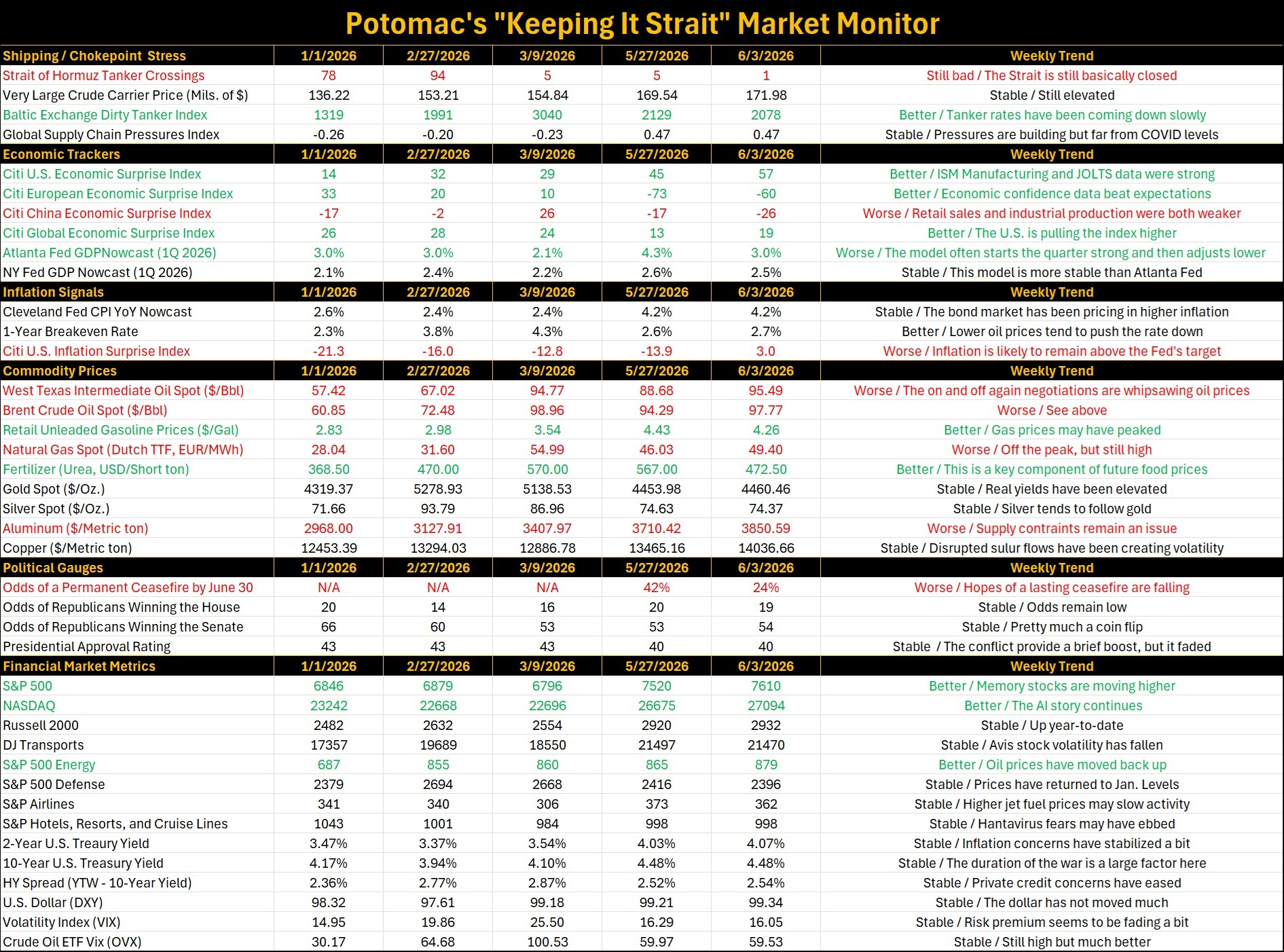

Weekly “Keeping it Strait” Highlights:

· The Strait of Hormuz remains closed. However, according to Polymarket the odds of a permanent ceasefire by June 30 have plunged from 42% to 24%.

· We found it notable that the monitor had more series in the green this week than in the red. The most interesting improvement is U.S. economic data, which continue to surprise to the upside. Job openings were better and manufacturing activity remains solid. There is little evidence yet of a slowing due to the ongoing Iran conflict despite elevated energy prices.

· Equity markets were driven higher in the U.S. on the back of earnings and a surge in memory chip stocks like Micron technology and Intel.