On May 22nd, Kevin Warsh took the oath of office as Chairman and member of the Board of Governors of the Federal Reserve. He was also unanimously selected as Chairman of the interest-rate setting Federal Open Market Committee (FOMC). On May 23rd, President Trump stated that a U.S. and Iran deal was largely negotiated and that the Strait of Hormuz would eventually be reopened as a result.

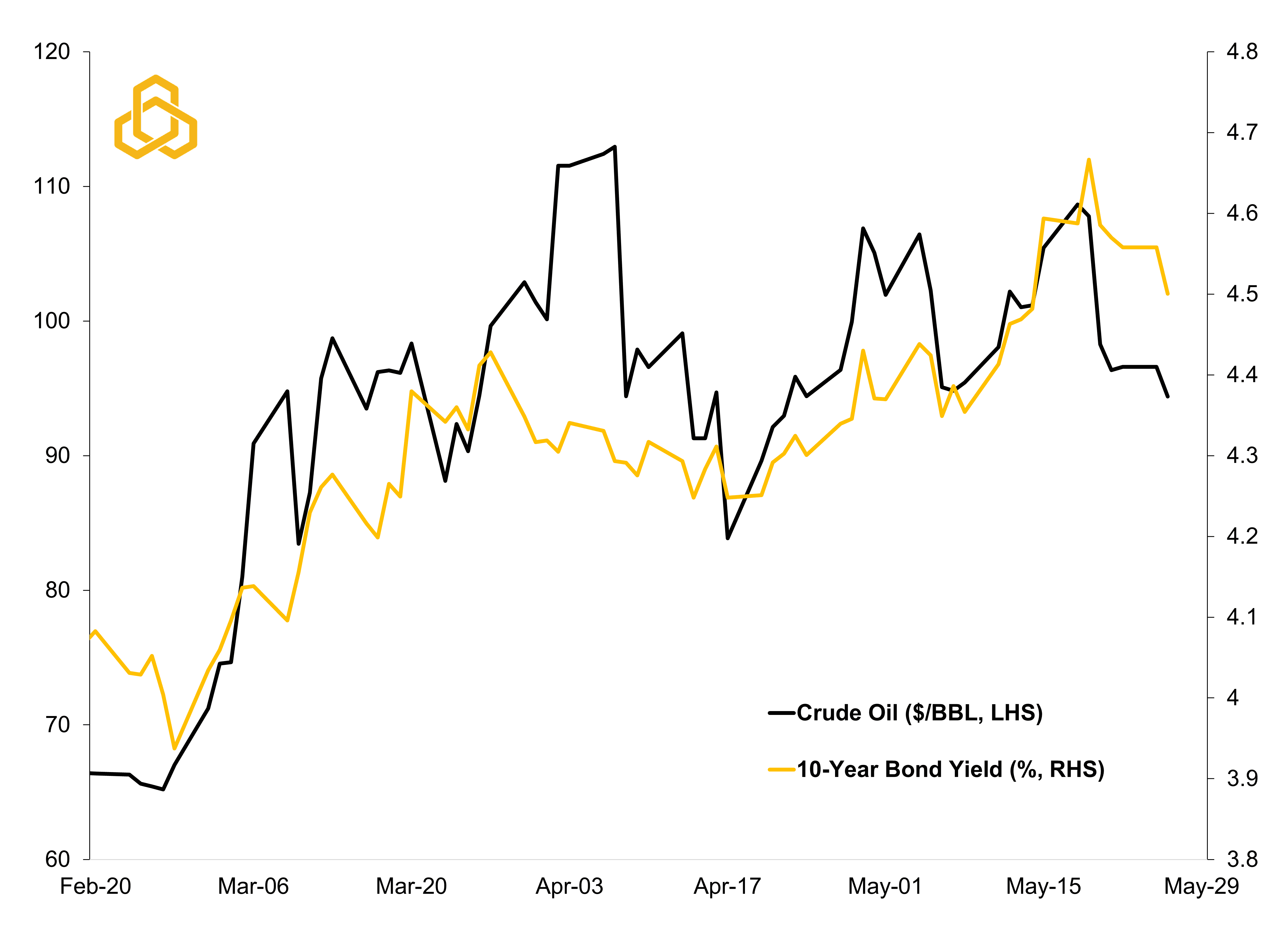

These negotiations are far from simple and there will likely be “two steps forward and one step back” at times, but further de-escalation with Iran would be a welcome development for markets increasingly focused on inflation, oil prices, and the path of monetary policy. With inflation expectations and bond yields both moving higher, Chair Warsh may find his new seat somewhat uncomfortable as long as the conflict persists, and the Strait remains closed (see figure 1).

Figure 1. Oil Prices vs. the 10-Year U.S. Bond Yield Since the Start of the Conflict

Sources: Department of Energy, U.S. Treasury, Bloomberg L.P., and Potomac. Data as of May 26, 2026. Note: Oil prices are West Texas Intermediate.

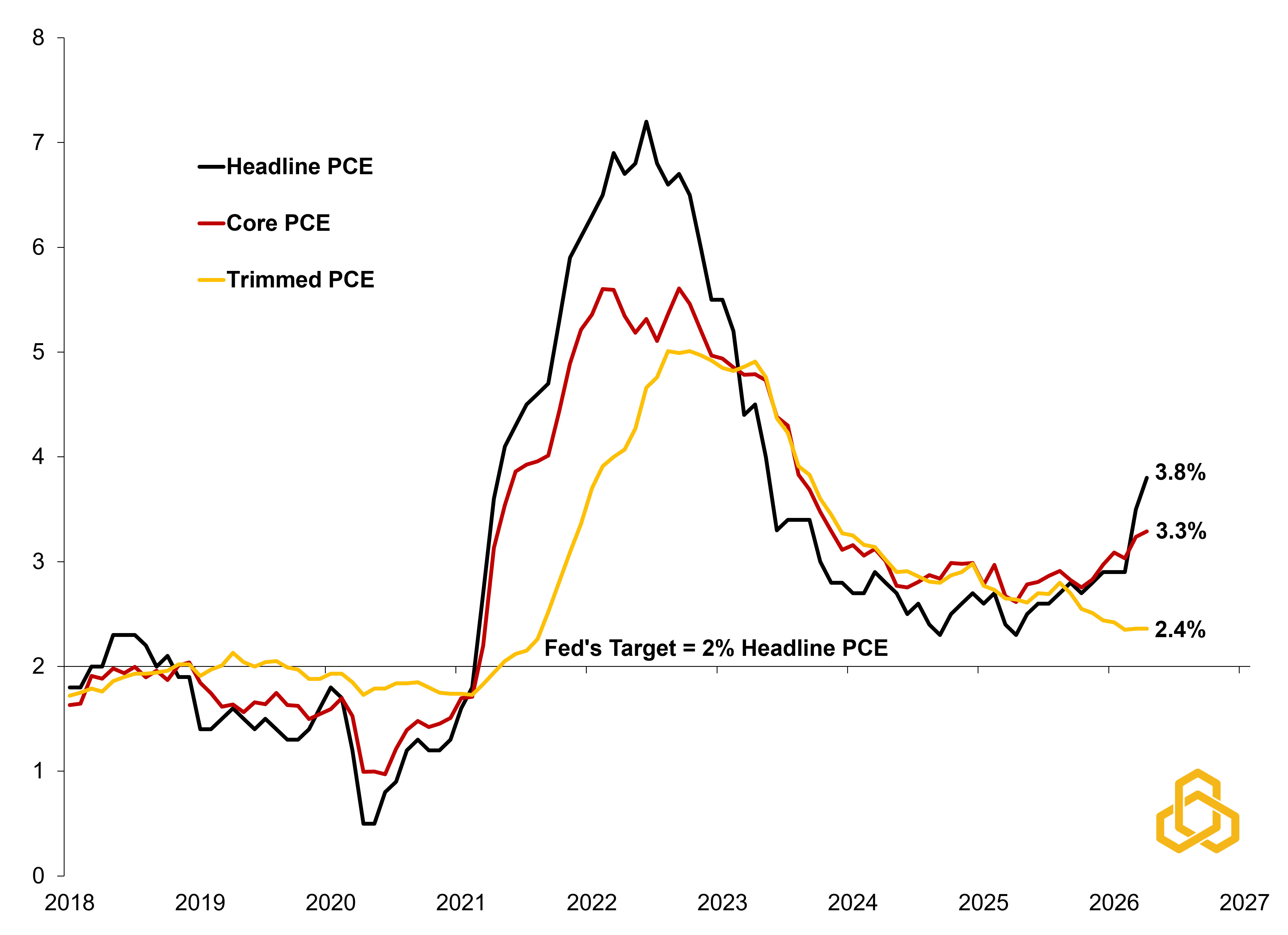

As it stands now, inflation remains well above the Fed’s target of 2.0%. The headline personal consumption expenditures (PCE) price index sits at 3.8% year-on-year, and the core measure, which excludes food and energy, lies at 3.3% year-on-year. Even Chair Warsh’s preferred metric of trimmed PCE inflation, which understated inflation by roughly 2.5% during the peak in 2022, remains above target (see figure 2).

Figure 2. PCE Inflation Metrics Since 2018 (Year-on-Year Percent Change)

Sources: Bureau of Economic Analysis, Bloomberg L.P., and Potomac. Data as of April 2026.

In fact, each of these inflation metrics has remained above the Fed’s target for more than five years. This marks the longest continuous overshoot since the Fed formally adopted the 2% inflation target in 2012.

And yet, the Fed continues to debate whether it should remove the easing bias from its language. Governor Christopher Waller acknowledged this at a recent speech in Germany, stating that, “I have become more concerned that higher energy prices may have a lasting effect on inflation…I would support removing the easing bias language in our policy statement to make it clear that a rate cut is no more likely in the future than a rate increase…my current policy position is to hold rates steady for the near term.”

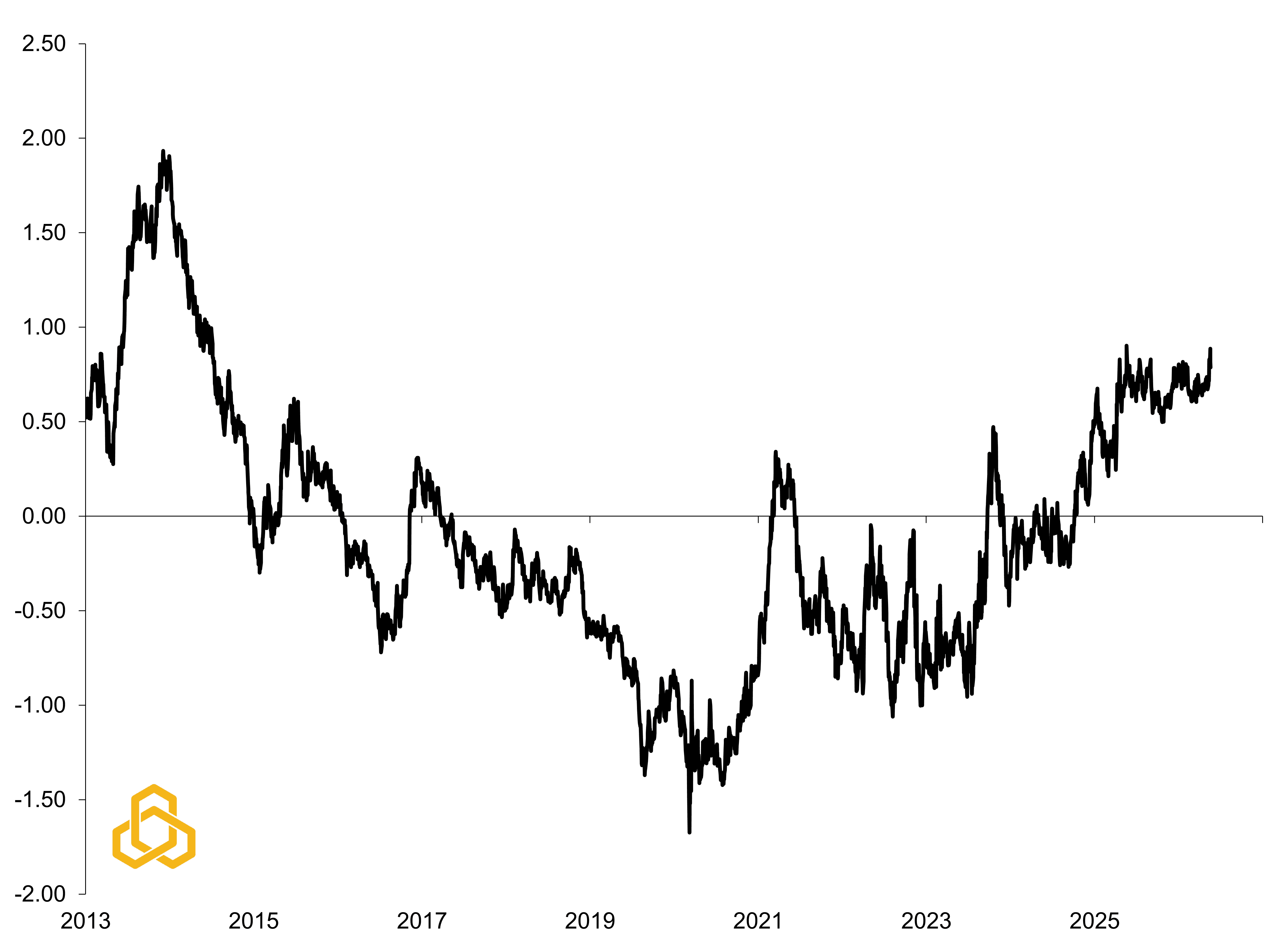

We suspect Governor Waller’s stance may become more widespread as the Fed attempts to maintain its credibility and prevent a further rise in the 10-year Treasury term premium, now at its highest level since 2013 (see figure 3).

Figure 3. ACM 10-Year U.S. Treasury Term Premium (%)

Sources: Federal Reserve Bank of New York, Bloomberg L.P., and Potomac. Data as of May 26, 2026. Note: “ACM” is Tobias Adrian, Richard Crump, and Emanuel Moench.

In fact, it is not unusual for presidents to prefer easier monetary policy only to face a more hawkish Fed Chair after they are appointed. This famously happened with Arthur Burns, but also Paul Volcker, Alan Greenspan, and Jerome Powell. Fed Chairs have often shifted from thinking like an appointee to acting more like a guardian of central bank credibility. If the President truly wants to avoid tighter monetary policy, it may be in his best interest to pursue a peace deal with Iran in a timely fashion.

Particularly, as it may still take substantial time to fully restore traffic through the Strait of Hormuz. According to Sultan Al Jaber, CEO of Abu Dhabi National Oil Company (ADNOC), “Even if this conflict ends tomorrow, it will take at least four months to get back to 80% of pre-conflict flows, and full flows will not return before the first or even second quarter of 2027.” Similar concerns have been echoed by Saudi Aramco CEO Amin Nasser.

The broader risk for markets is that a Fed perceived as tolerating a higher inflation regime could push term premium and long-term bond yields even higher at a time when U.S. net interest costs are already risings steadily. Such an outcome could also further weaken the diversification benefits of the traditional 60/40 portfolio, particularly if stocks and bonds respond negatively to higher inflation expectations simultaneously. Please see our “Bear Market in Diversification” piece for additional insights into how structurally higher inflation and rising term premium could reshape traditional portfolio construction.

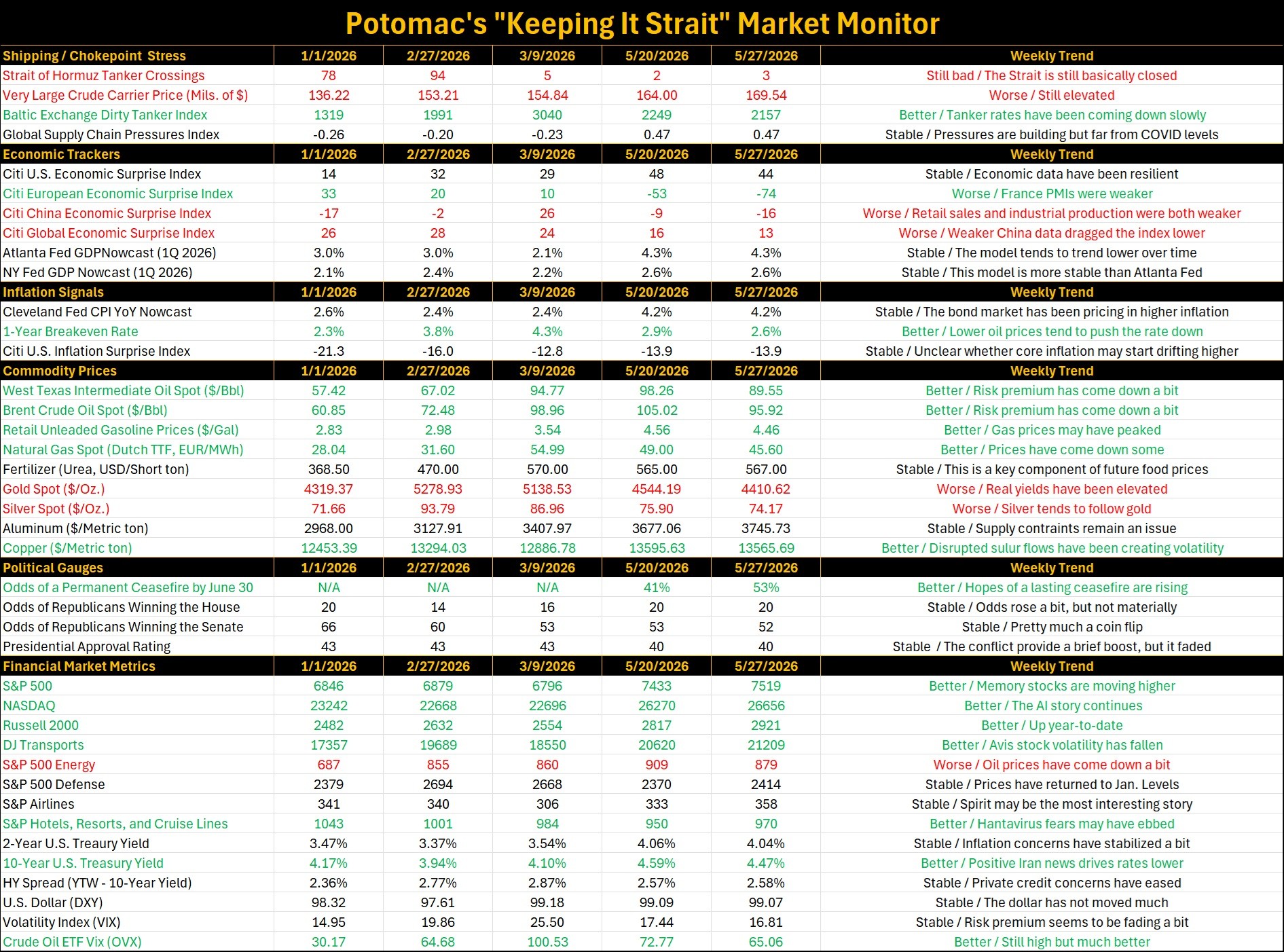

Weekly “Keeping it Strait” Highlights:

The Strait of Hormuz remains closed. However, according to Polymarket the odds of a permanent ceasefire by June 30 have jumped to 53%.

As a result, oil prices have come down alongside 1-year breakeven inflation rates and 10-year Treasury yields. The lingering question is how long it will take for traffic flows to resume if the Strait is eventually reopened. Several CEOs of major oil companies have suggested full traffic may not resume until 2027.

Equity markets were driven higher in the U.S. on the back of earnings and a surge in memory chip stocks like Micron technology. With the producer price index for semiconductors roughly 25% higher year-on-year, expectations are rising that corporate revenues will surge as well.

Source: Bloomberg L.P. and Potomac. Data as of May 27, 2026. Note 1: The dates selected are 2/27/2026 (start of the conflict), 3/9/2026 (initial oil surge/peak as the Strait closed), and the latest week and previous week to compare the weekly trend. Note 2: Economic and inflation surprise index readings about zero imply that data are beating the consensus on average, below zero means that data are missing expectations. Note 3: In commodity prices, we ranked higher oil, natural gas, retail gas, fertilizer, and aluminum prices as bad for the economy because it weighs on growth, we ranked rising gold and silver prices are good due to the investor perspective. Note 4: Political betting market odds are forecasts. All forecasts are expressions of opinions and are subject to change without notice and are not intended to be a guarantee.