Buy-and-hold investment outcomes are largely dictated by timing, especially in the 20 years leading up to retirement when the most capital is allocated. Market conditions during this window, which are determined by an investor’s birth date, can lead to vastly different financial outcomes.

The historical S&P 500 Index data shows that over rolling 20-year periods some investors experienced over 1,400% market growth, while others saw only a fraction of that, often enduring prolonged bear markets and deep drawdowns.

Traditional market narratives cite long-term returns but overlook the psychological and financial strain of steep losses, which often cause investors to abandon their strategies before realizing full gains.

This article highlights the critical role of risk management in long-term investing and why a tactical approach can improve the likelihood of achieving cited long-term returns.

The Most Important 15-20 Years

Investors’ market experiences vary significantly depending on when they begin investing.

This is especially true for passive index investors, who are at the mercy of market conditions during their investing lifetime. The reality is that there is a limited time window for which investors can build the wealth they need for retirement.

More specifically, the 20 years leading up to retirement are a significant determinant of final wealth.

A T. Rowe Price analysis suggests that 45-year-olds should have three times their current income set aside for retirement. This savings benchmark rises to five times current income at age 50 and seven times current income at age 55. This represents a substantial increase and is the largest amount of new money allocated to investments vs. any other period within an individual’s lifetime.

The problem is that during this critical period, results are left to chance, which leads to the concept of sequence risk.

Born at the Right (or Wrong) Time?

Anyone familiar with sequence risk knows how important timing is to overall investment success. A strong 20 years leading into retirement can yield a significant lump sum, while a mediocre period may leave the investor with far less than their financial plan anticipated.

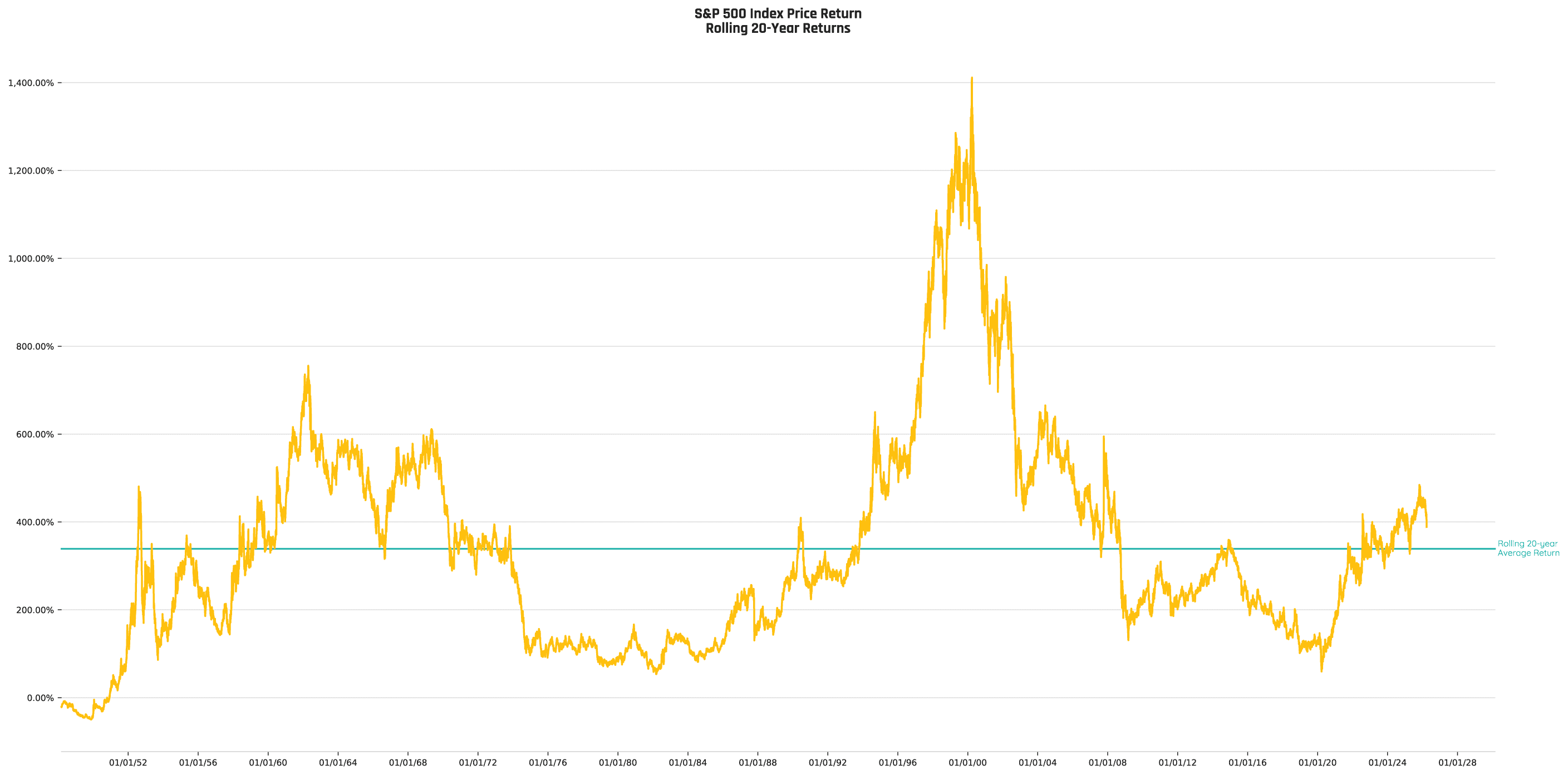

The graphic below illustrates the wide range of outcomes possible in the S&P 500 Index Price Return (S&P) over a 20-year period.

Source: Norgate Data | Daily data of the S&P 500 index price return

The rolling 20-year return of the S&P demonstrates the gains a buy-and-hold investor could have achieved during their most critical wealth-building period.

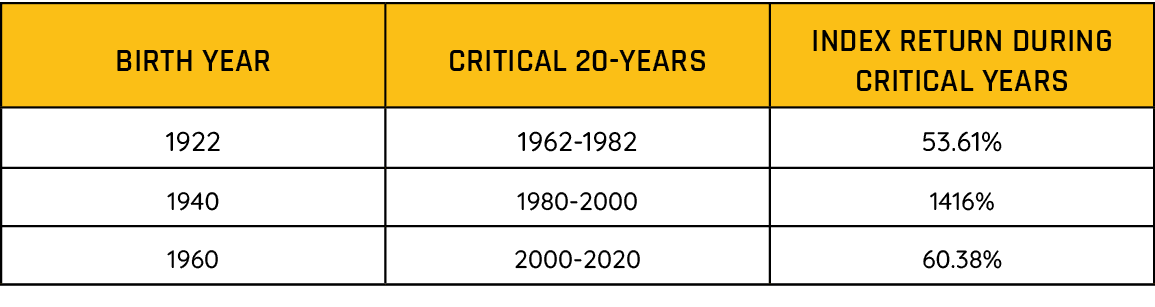

The table below summarizes the most extreme time periods, using daily prices of the S&P 500 index price return, highlighting how dramatic outcomes can differ based on birth date alone. Each birth date chosen is the most extreme example and only the year in which that happened is listed for simplicity.

Source: Norgate | Assumes 60yr Old Retirement Date | Daily data of the S&P 500 index price return | Exact ending dates are 3/27/2000, 3/8/1982, 3/23/2020.

For example, someone born at the best time in 1940 experienced a strong two decades leading into retirement when the S&P 500 index rose more than 1,400%, whereas for people born at the worst time in 1922 or 1960, the S&P rose by a tiny fraction of that amount.

For the luckiest person, the index experienced a 14.56% compound annual return during the critical years, while someone born eighteen years earlier in 1922 saw just 2.16% per year.

This significant difference would have a profound impact on a financial plan. In the case of those born in 1922, they could have far less wealth at retirement than anticipated.

The Illusion of Total Return

While citing long-term returns provides some insight, it often overlooks the fact that achieving those returns requires enduring significant losses along the way.

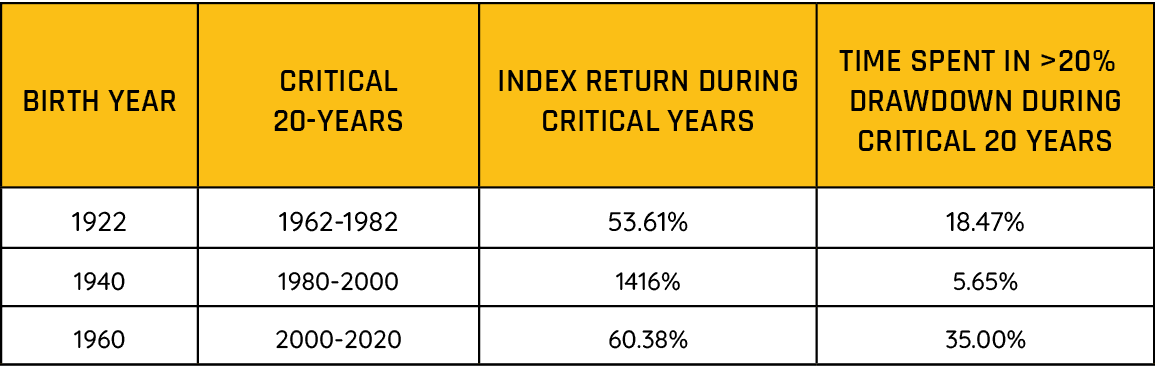

Using the same data, we added a column (highlighted in grey) showing how long the S&P 500 spent in a drawdown greater than 20% during the critical 20-year period leading up to retirement.

In other words, how long would each investor have had to endure a bear market to achieve the long-term total return?

Source: Norgate | Daily data of the S&P 500 index price return | Exact ending dates are 3/27/2000, 3/8/1982, 3/23/2020.

As expected, those born at the worst times in 1922 and 1960 would have spent far longer in a bear market than the investor born in 1940 simply because of their different birth dates.

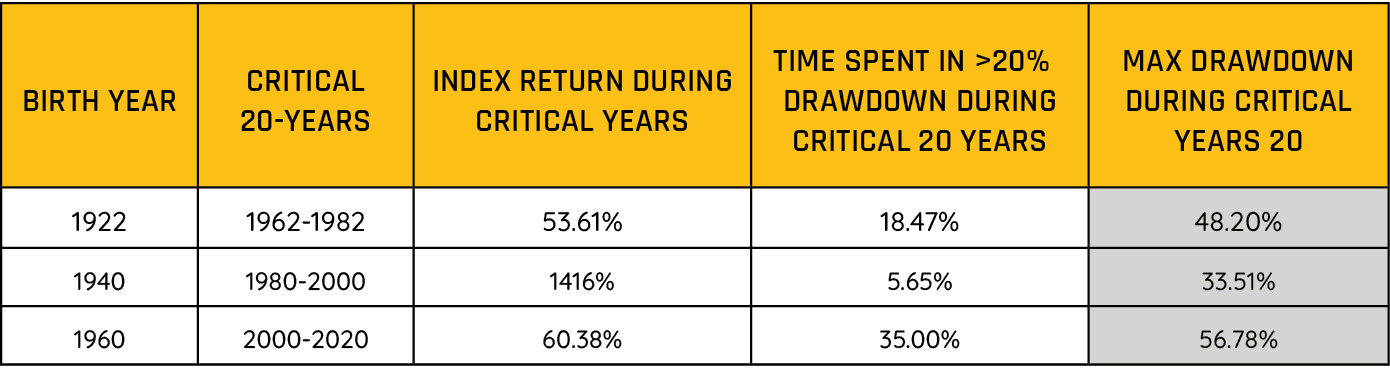

More important than time spent in a bear market - what would the maximum drawdown be for each investor?

Source: Norgate | Daily data of the S&P 500 index price return | Exact ending dates are 3/27/2000, 3/8/1982, 3/23/2020.

To achieve an impressive return of 1,416%, the lucky investor would have still needed to endure a 33.51% drawdown.

Even more challenging were the experiences of those born in 1922 and 1960, who would’ve had to endure drawdowns of -48.20% and -56.78% respectively.

While holding through a drawdown is possible, watching hard-earned money disappear is often too painful. Many will “tap out” during a drawdown and fail to achieve the long-term return.

We think this is a major flaw of commonly held beliefs about markets – that long-term returns are cited without considering the pain someone would have needed to endure to get there.

A Less Painful Way

As demonstrated, we believe that maximum drawdown is the key risk statistic driving investors to tap out before achieving long-term returns. Any long-term total return cited in the media is likely an illusion, as it disregards the challenges of enduring the losses along the way.

The data shows that some spent almost no time in bear markets while others experienced multiple 50% corrections. Birth date determines the investment environment for each person, which is completely left to chance.

As an unconstrained tactical investment manager, we position our strategies to offer some degree of protection from catastrophic investment losses.

We believe in managing risk, so that the value of investment assets doesn’t decline to a point where someone’s financial future, their security and comfort, would be in jeopardy.

If the risk is managed, long-term total returns can be achieved with greater certainty because the likelihood an investor would tap out is decreased.

A Final Word

Our analysis demonstrates that there is a 20-year window during which investing is critical, leading up to retirement. This window is determined entirely by an investor’s birth date.

Media sources often cite the long-term total returns of popular indexes like the S&P 500 but fail to account for the risks involved. This creates an illusion of returns, misleading anyone that plugs these figures into their financial plan without considering whether they could have realistically achieved them.

As a tactical manager, we believe that managing risk provides a more tolerable investment journey. By reducing both the time spent in major drawdowns and the severity of those drawdowns, investors are more likely to stick with the strategy and achieve cited long-term returns.

For a more in-depth look at how Potomac’s flagship strategy, Bull Bear, has managed risk and provided a more tolerable path to long-term returns, we invite you to learn more here.