As we suggested in last week’s note, The State of the Other Mandate: What the Labor Market Is Telling Us, the labor market shocked investors with a surprisingly strong payrolls report with the U.S. economy adding 172,000 jobs in May while the unemployment rate stayed steady at 4.3%. This was nearly double the consensus call for 88,000 jobs.

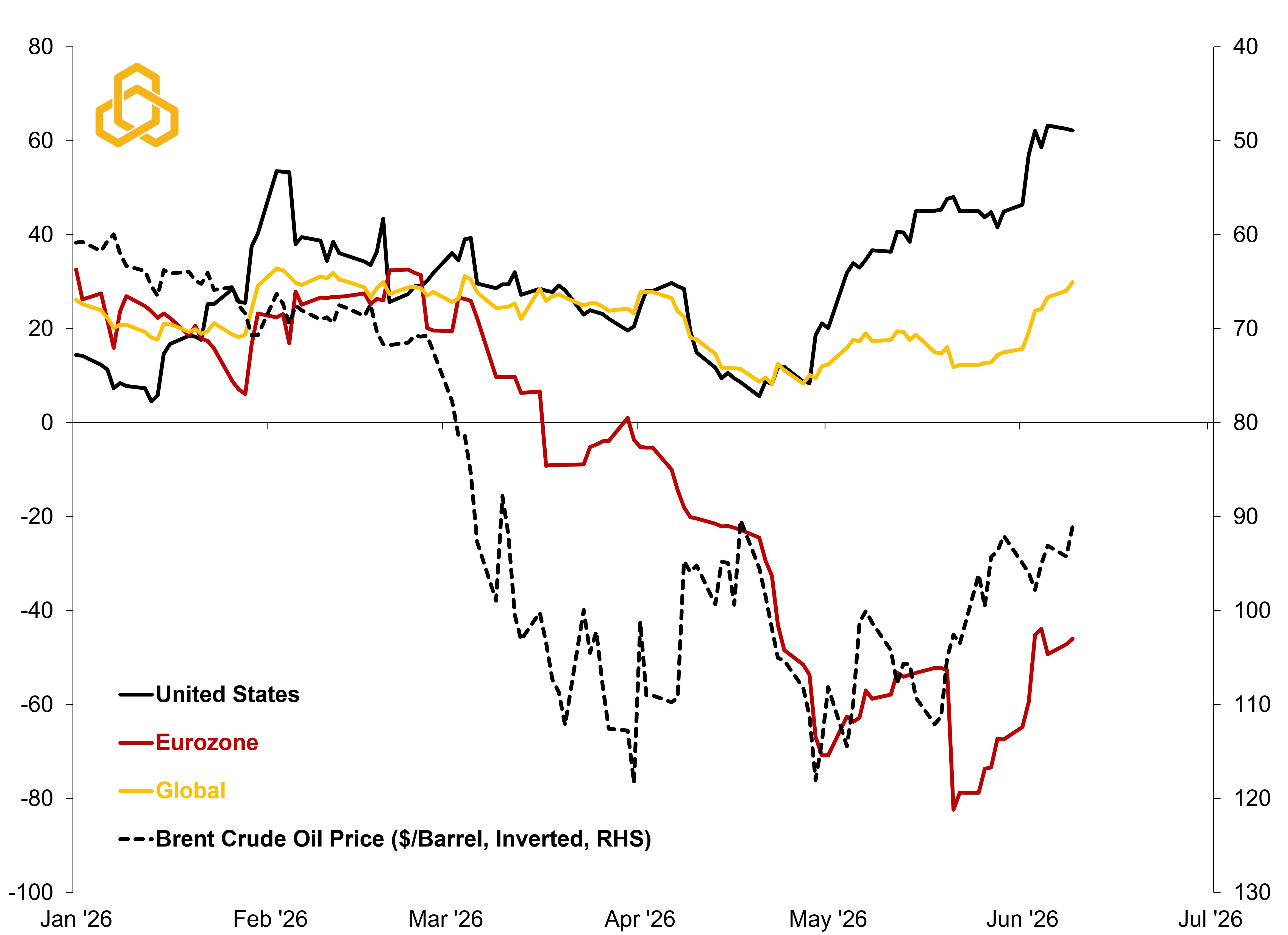

With the release, Citi’s U.S. Economic Surprise Index, which measures whether economic data are beating or missing expectations, now stands at its highest level since 2023 and significantly better than the energy-dependent Eurozone (see figure 1).

Figure 1. Citi Economic Surprise Indices vs. the Price of Brent Crude Oil

Sources: Citigroup Global Markets, Inc., Bloomberg, and Potomac. Data as of June 8, 2026. Note: A reading above zero implies that economic data are on average beating consensus. Below zero means that data are surprising to the downside.

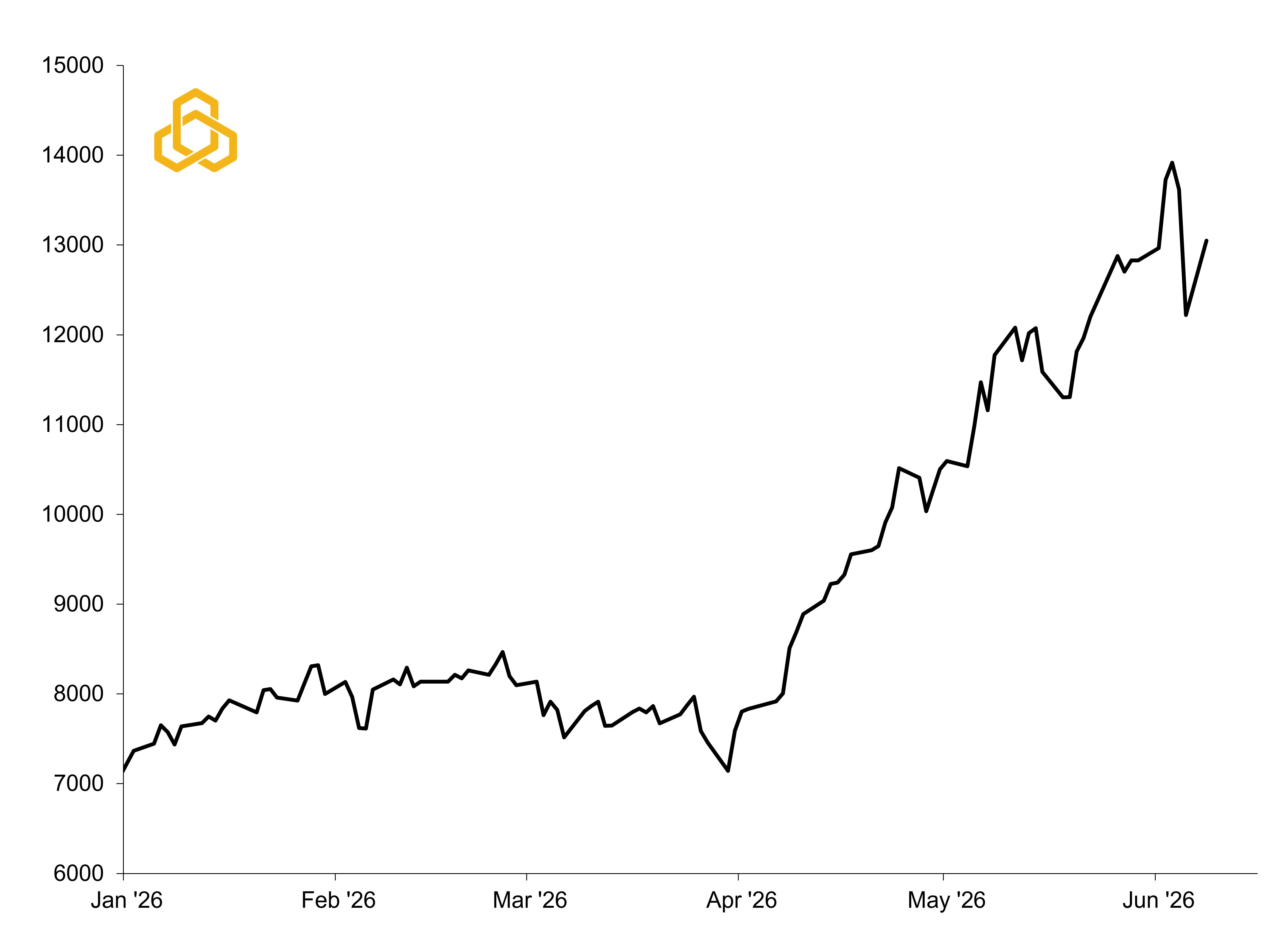

Although this sounds like uniformly good news for investors, the S&P 500 and NASDAQ suffered their worst days of the year, falling 2.64% and 4.18%, respectively. Some of this shakeout should not be surprising given the strong run stocks have enjoyed this year, with semiconductor stocks still up 72.5% despite the recent selloff (see figure 2). More importantly, however, the recent strength in economic data raises a larger question: Can the Federal Reserve remain on hold indefinitely, or will policymakers ultimately be forced to raise rates in response to building inflationary pressures?

Figure 2. Philadelphia Semiconductor Index (SOX) Year-to-Date

Sources: NASDAQ, Bloomberg L.P., and Potomac. Data as of June 8, 2026.

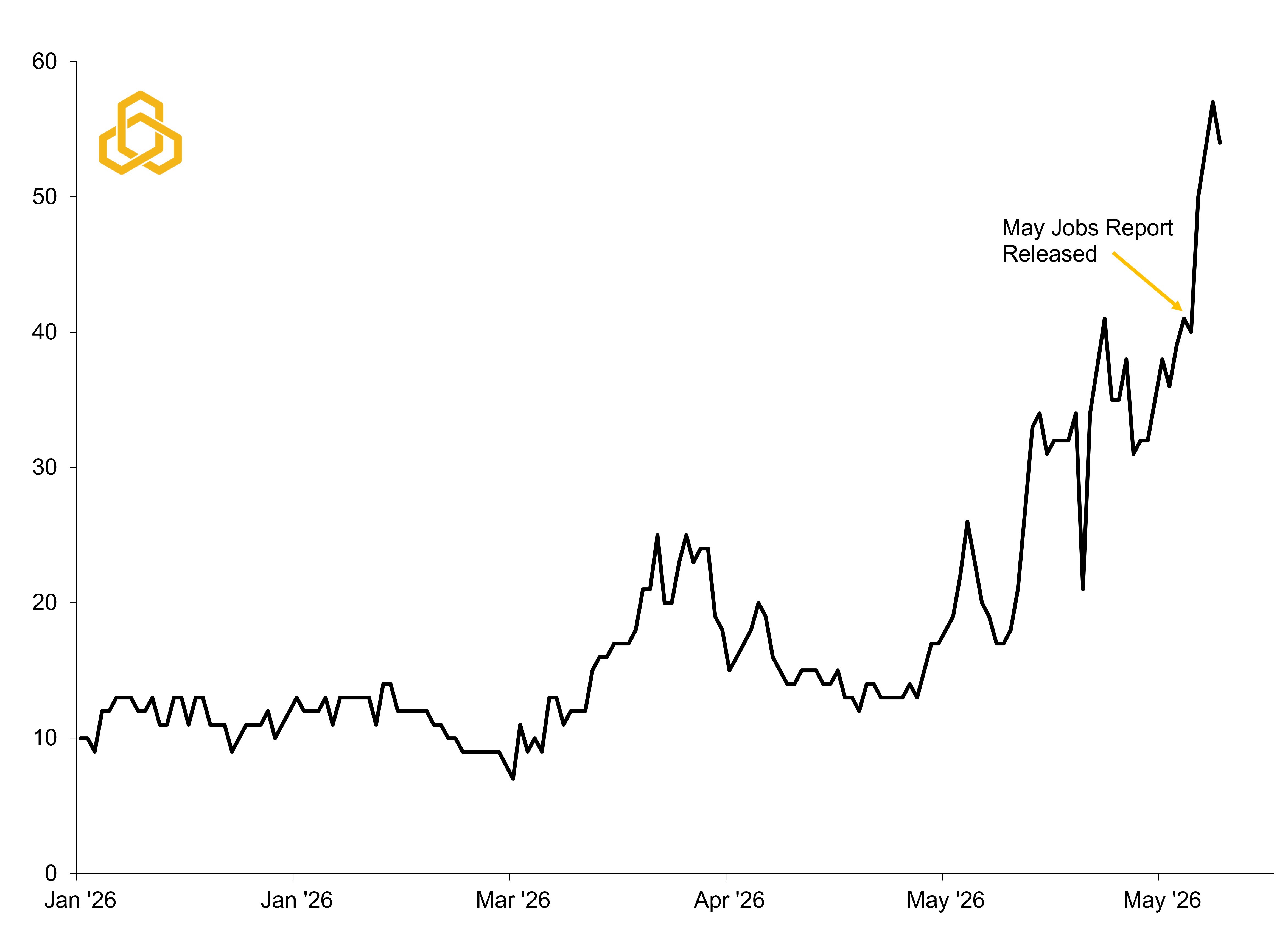

Following the May employment report, the market pulled forward its expectations for a Fed rate hike from March 2027 to December 2026. Betting markets, such as Polymarket, are now assigning roughly 55% odds of a rate hike in 2026 (see figure 3).

Figure 3. Polymarket Odds of a Rate Hike in 2026 (%)

Sources: Bloomberg L.P., and Potomac. Data as of June 8, 2026.

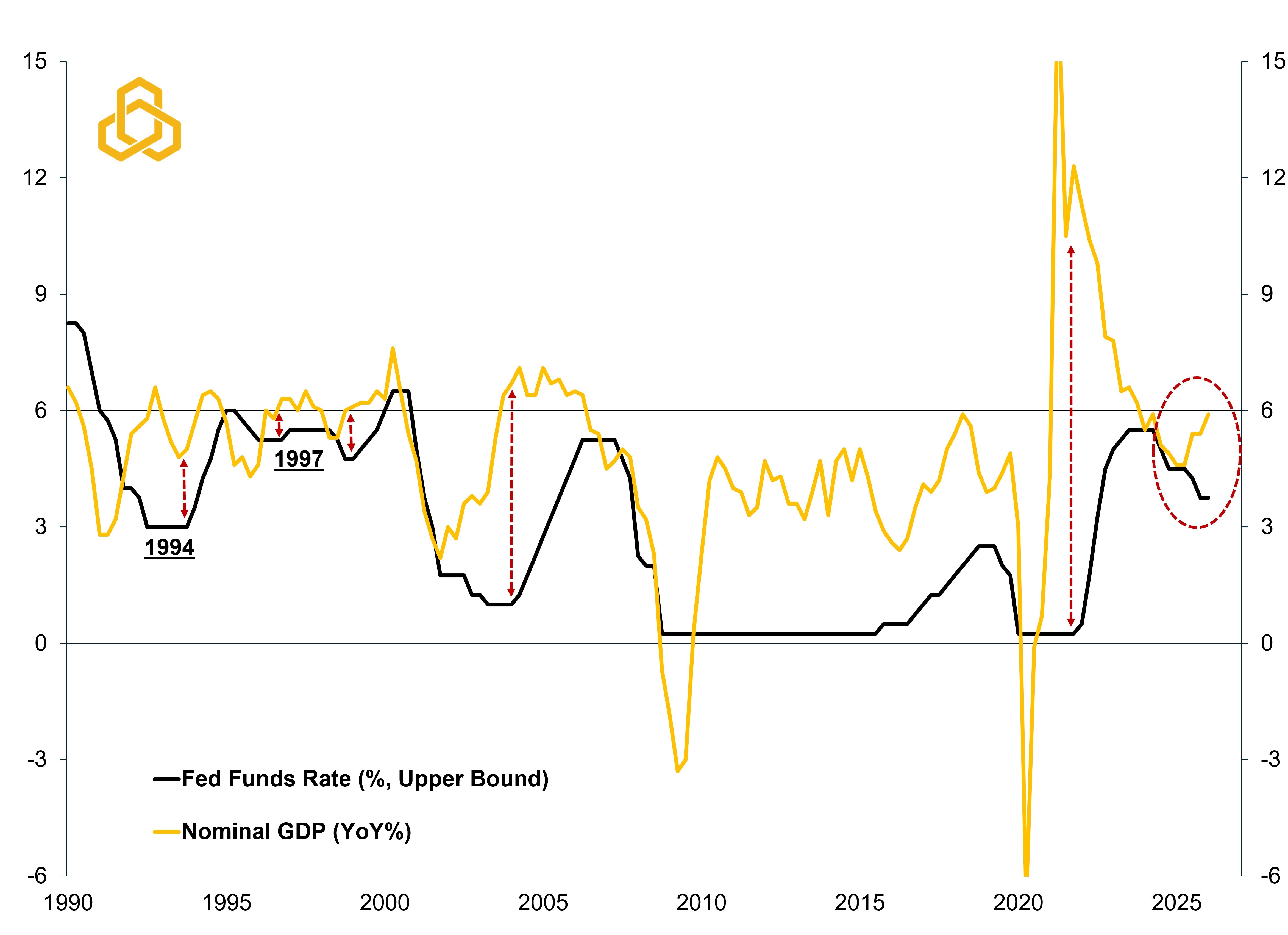

As we have discussed for some time, including in our Thirty Years Later: Another Fork in the Road for the Fed, this debate aligns with previous periods when nominal gross domestic product (GDP), which includes inflation, starts to push north of 6%. While that level is not some magical threshold, it has historically coincided with the beginning of Federal Reserve tightening cycles (see figure 4). The reason is that it tends to signal that demand is running too hot, inflation pressures are building, or both.

Figure 4. Nominal Gross Domestic Product vs. the Federal Funds Rate

Sources: Bureau of Economic Analysis, Federal Reserve Board of Governors, Bloomberg L.P., and Potomac. Data as of 1Q 2026. Note: Nominal GDP includes inflation as measured by the PCE price deflator.

In our view, the monetary backdrop looks most like 1994 and 1997, when the U.S. economy experienced a surge in technology investment as companies spent heavily to connect to the internet and prepare for Y2K. Interestingly, nominal growth was about the same at the time, but inflation was lower. Unemployment was higher, but still within the range of what most economists would consider full employment. Equity valuations, however, are now 40% higher than in 1994 and 50% above 1997 (see figure 5).

Figure 5. Monetary Policy Backdrop in 1994, 1997, and Current

Sources: Bureau of Economic Analysis, Bureau of Labor Statistics, Standard & Poor’s, Bloomberg L.P., and Potomac. Data as of June 8, 2026.

While forward-looking earnings remain strong, lofty valuations could add to market volatility should the Fed embark on a new, but likely short, tightening cycle. While no historical comparison is perfect, these episodes may provide a useful guide for how markets could respond if the Fed ultimately decides to raise rates (see figure 6).

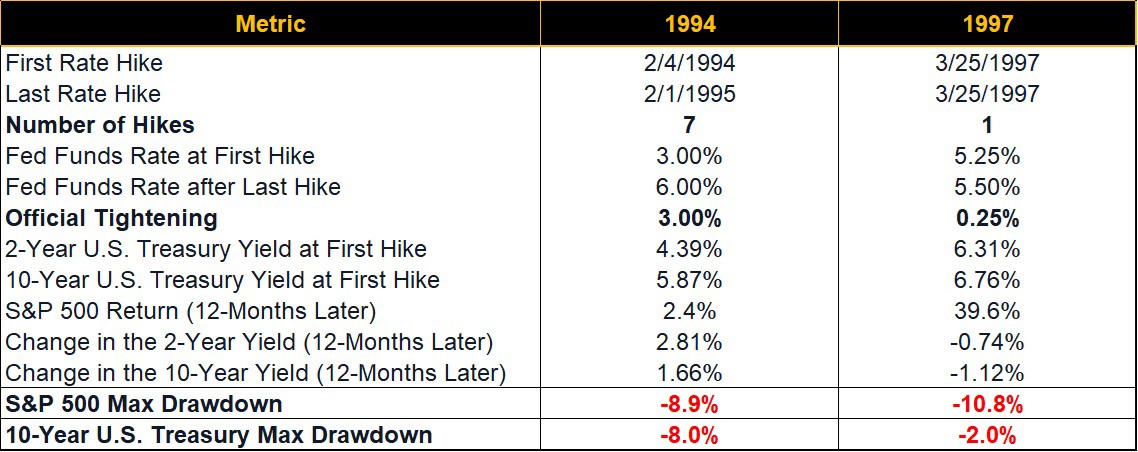

Figure 6. 1994’s “Great Bond Massacre” vs. 1997’s “One and Done”

Sources: Bureau of Economic Analysis, Bureau of Labor Statistics, Standard & Poor’s, Bloomberg L.P., and Potomac. Data as of June 8, 2026.

In our view, the key difference between the two periods was the bond market's response to Fed policy. In 1994, investors were caught off guard by the speed and magnitude of tightening, causing Treasury yields to surge and producing one of the worst drawdowns on record for intermediate-term government bonds. Stocks fared somewhat better, but the S&P 500 still went essentially nowhere in the year following the Fed's first hike.

The experience in 1997 was very different. The Fed raised rates just once before stepping aside, and Treasury yields moved lower over the following year as inflation fell by 1.4 percentage points. Lower energy prices, falling import costs, and a stronger U.S. dollar all helped ease inflation pressures, while equities continued to benefit from strong earnings growth and improving productivity. The result was a nearly 40% gain for the S&P 500 in the year following the hike.

While today's growth backdrop shares similarities with both 1994 and 1997, the ultimate market outcome may depend less on economic growth and more on whether inflation follows the path of 1994 or 1997. The good news is that nominal GDP growth today looks remarkably similar to both periods, suggesting the economy may be stronger than many investors appreciate. The challenge is that inflation remains significantly higher than it was during either episode, while equity valuations are substantially richer.

If inflation proves sticky and the Federal Reserve is forced to resume tightening, investors could experience a period of heightened volatility similar to 1994, particularly in interest-rate-sensitive assets. One of the key lessons from that period is that diversification does not always come from owning bonds. During the so-called "Great Bond Massacre," stocks experienced only a modest correction, while bonds suffered one of their worst drawdowns on record. As a result, investors may want to think more broadly about diversification and ensure portfolios are not overly dependent on bonds to offset equity risk.

If, however, inflation follows the path it did in 1997 and begins to ease despite solid economic growth, the Fed may only need to make modest policy adjustments, allowing equities to continue benefiting from strong earnings growth and rising productivity.

For now, the battle between the Fed's two mandates appears far from settled. The labor market is showing signs of renewed strength, while inflation risks remain elevated. As a result, investors may soon discover that the employment mandate, while largely forgotten in recent years, has a habit of finding its way back into focus.